Dec CPI Preview: Don’t Trust This CPI Bounce

Key Takeaways:

- December CPI is expected to rebound, but the increase is largely driven by technical and statistical factors.

- Data distortions related to government shutdowns and abnormal sampling likely suppressed prior inflation readings.

- December inflation may temporarily overstate price pressures due to catch-up effects.

- While the Fed is unlikely to react to a single data point, officials’ post-CPI commentary will be critical.

- Inflation stickiness remains a medium-term risk as companies plan to pass tariff-related costs to consumers.

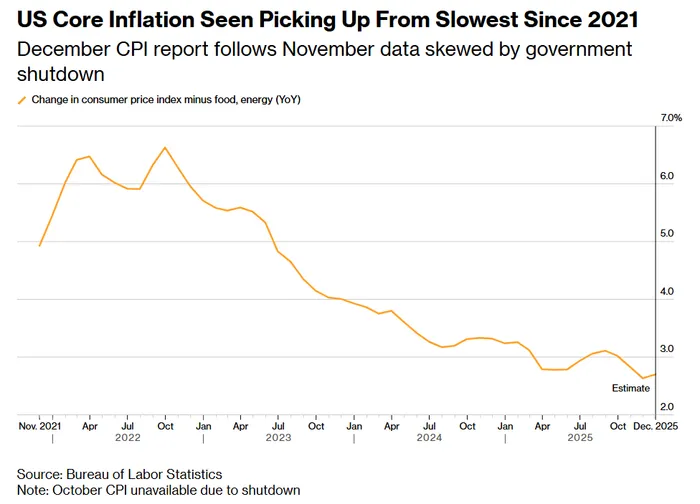

The BLS will release its December CPI data. Market expectations point to a year-over-year increase of 2.7% for both headline CPI and core CPI, with month-over-month gains of 0.3% for each, signaling a rebound in inflation compared with November.

It is important to note that the December CPI rebound does not indicate the onset of a second wave of inflation. Rather, it is largely driven by technical factors. Due to the government shutdown in October and November, the Bureau of Labor Statistics (BLS) was forced to adopt unconventional methods in certain subcomponents, such as “carrying forward prior values” and “forward rolling imputation.” These approaches assume that prices remain unchanged in the short term. When inflation is still in positive territory, such methods mechanically depress current inflation readings.

Moreover, the November price collection period coincided heavily with Black Friday discount events, leading to a systematic underestimation of inflation. As sampling normalized in December, previously suppressed categories may experience a temporary catch-up, pushing the overall inflation reading higher.

Another contributing factor is the catch-up effect created by the BLS’s bi-monthly sampling mechanism. With October data missing, August prices were directly carried forward into both October and November. As a result, December CPI effectively reflects cumulative price changes from August through December — a four-month span — rather than the usual two-month comparison. This mechanism causes affected categories, such as certain apparel and recreational goods, to show a temporary upward bias in December.

Federal Reserve officials are well aware of these data distortions and are unlikely to base policy decisions on a single month’s reading. However, with the January FOMC meeting approaching, several Fed officials are expected to speak shortly after the CPI release. Close attention should be paid to how they interpret the inflation data.

Inflation Stickiness Is the Key Risk

While December’s inflation rebound is partly technical, the risk of inflation stickiness cannot be fully dismissed. Many companies have disclosed during earnings calls that they plan to pass on tariff-related cost increases to consumers beginning in early 2026. Economists at Santander have warned that this could trigger a renewed rise in prices. Going forward, markets will closely monitor signals from Federal Reserve officials.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet