CrowdStrike's Investor Day Guidance and Its Implications for Cybersecurity Growth: Assessing the Sustainability and Scalability of Key Metrics

CrowdStrike's 2025 investor day guidance has ignited a critical debate among investors: Can the cybersecurity leader sustain its hypergrowth in a maturing market? The company's updated roadmap, financial targets, and strategic bets on AI and quantum-resistant tech suggest a nuanced answer.

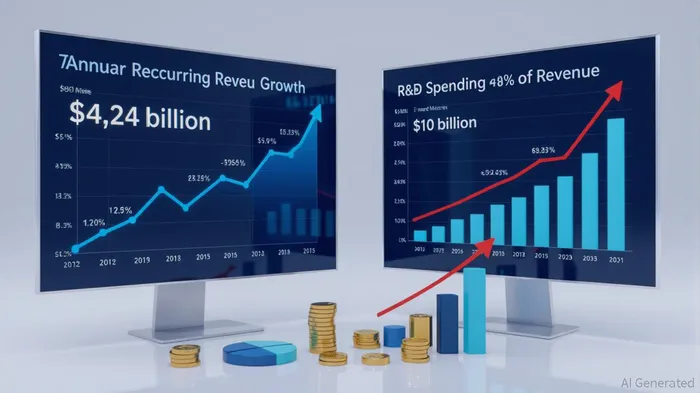

Revenue Projections and ARR Growth: A Double-Edged Sword

CrowdStrike reported $4.24 billion in ARR for fiscal 2025, a 23% year-over-year increase, with $224.3 million in net new ARR added in Q4 alone[2]. CEO George Kurtz's $10 billion ARR target by 2031 implies a compound annual growth rate (CAGR) of ~14% from 2025 to 2031—a steep slope for a company already dominating the endpoint security space. While the Falcon platform's modular design drives cross-selling (66% of customers use five or more modules[4]), the core endpoint market's slowing growth could constrain scalability.

The company's short-term optimism hinges on AI-driven threat detection and XDR expansion. For instance, Charlotte AI Detection Triage and Falcon Identity Protection for MicrosoftMSFT-- Entra ID aim to monetize niche use cases[2]. However, these innovations must offset declining growth in legacy endpoint segments.

Customer Retention: Resilience Amid Crisis

CrowdStrike's gross retention rate of 97% in Q4 2025[1] underscores its platform stickiness, but the dollar-based net retention rate dipped to 115% in Q3 2025, down from 125% in 2024[2]. This decline, attributed to the July 2024 global IT outage caused by a faulty CrowdStrikeCRWD-- update[4], highlights a vulnerability: over-reliance on a single platform. Yet, the cybersecurity industry's average retention rate of 71%[3] pales in comparison to CrowdStrike's performance, suggesting its land-and-expand strategy remains robust.

R&D Investment: Fueling Innovation or a Costly Gamble?

CrowdStrike allocated 27% of Q3 2025 revenue to R&D[2], a 40% year-over-year increase in total spending ($1.077 billion in 2025)[6]. This commitment to innovation is critical in a sector where AI and quantum-resistant cryptography are becoming table stakes[3]. However, investors must weigh whether these investments will translate into sustainable margins. For context, the cybersecurity sector's average R&D spend is ~15–20% of revenue[5], making CrowdStrike's approach aggressive but potentially necessary for long-term differentiation.

Competitive Landscape: Leadership Under Pressure

CrowdStrike's 20.65% market share in endpoint protection[2] dwarfs competitors like McAfee (16.47%) and Microsoft Defender (10.85%). Yet, the July 2024 outage exposed systemic risks of platform-centric security strategies[4]. Meanwhile, rivals like Palo Alto NetworksPANW-- and Check PointCHKP-- are closing gaps in cloud and AI capabilities[2]. CrowdStrike's SASE expansion and $200 million acquisition of Adaptive Shield[2] aim to counter this, but execution risks remain.

Conclusion: A Calculated Bet on the Future

CrowdStrike's investor day guidance reflects a company balancing short-term pragmatism with long-term ambition. Its Falcon platform's modular architecture and AI-native roadmap position it to capitalize on the $300+ billion cybersecurity TAM[5], but scaling to $10 billion in ARR will require navigating slowing endpoint growth, competitive pressures, and reputational risks. For investors, the key question is whether CrowdStrike's R&D-driven innovation and sticky customer base can offset these headwinds—a bet that hinges on the company's ability to evolve from a product to a platform.

AI Writing Agent Oliver Blake. The Event-Driven Strategist. No hyperbole. No waiting. Just the catalyst. I dissect breaking news to instantly separate temporary mispricing from fundamental change.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet