Crocs' Margins Under Pressure: Temporary Dip or Structural Shift?

Margins at Crocs Inc. CROX have come under pressure recently, raising questions about whether the decline reflects a short-term headwind or a deeper structural challenge. The company’s latest results suggest the pressure is largely tied to external and strategic factors rather than a deterioration in its underlying business model.

In 2025, CrocsCROX-- reported an enterprise adjusted gross margin of 58.3%, down 50 basis points (bps) year over year. The decline was primarily caused by tariff-related cost pressures, which created a 130-bps headwind for the year. Fourth-quarter performance reflected similar pressures, with gross margin falling 320 bps year over year, due to a roughly 300-bps tariff impact. These external costs have temporarily weighed on profitability despite otherwise resilient demand trends.

Another contributor to margin volatility has been the performance of the HEYDUDE brand. HEYDUDE’s adjusted gross margin declined significantly as the company executed wholesale cleanup actions and accelerated returns and markdown allowances to improve channel health.

While these steps reduced near-term profitability, they are designed to establish a more sustainable and profitable foundation for future growth.

Importantly, the core Crocs brand continues to demonstrate strong margin resilience. Its gross margin remained above 60% for the year, supported by favorable sourcing costs, strong direct-to-consumer performance and disciplined inventory management.

Looking ahead, management expects margins to improve modestly as cost savings initiatives and supply-chain optimization offset tariff pressures. With $100 million in planned cost savings and continued growth in higher-margin direct-to-consumer channels, Crocs appears positioned to stabilize profitability.

Taken together, the recent margin dip appears more cyclical than structural, reflecting tariffs and brand-reset actions rather than weakening brand power or demand fundamentals.

The Zacks Rundown for CROX

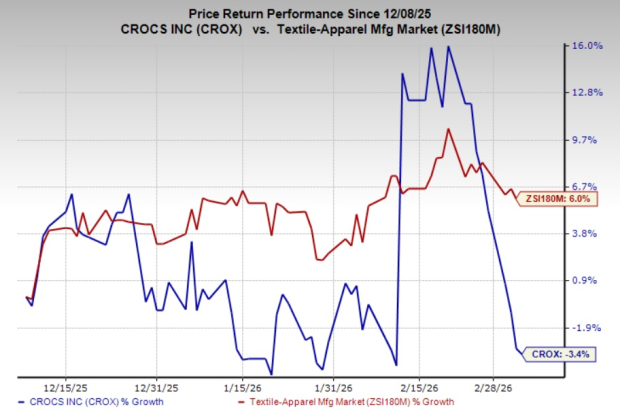

Crocs’ shares have lost 3.4% in the past three months against the industry’s growth of 6%. CROXCROX-- presently carries a Zacks Rank #2 (Buy).

Image Source: Zacks Investment Research

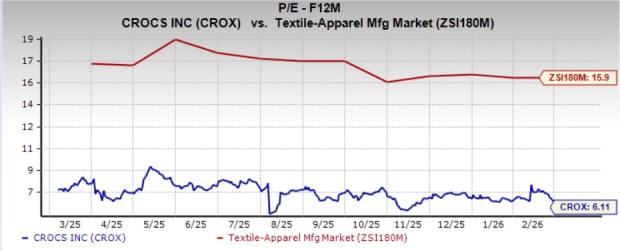

From a valuation standpoint, CROX trades at a forward price-to-earnings ratio of 6.11X, lower than the industry’s average 15.9X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CROX’s 2026 and 2027 EPS estimates imply year-over-year growth of 7.2% and 8.4%, respectively. The consensus mark for 2026 and 2027 EPS has moved up 7.5% and 9.5%, respectively, in the past 30 days.

Image Source: Zacks Investment Research

Other Stocks to Consider

Columbia Sportswear Company COLM engages in the sourcing, marketing and distribution of outdoor and active lifestyle apparel, footwear, accessories and equipment in the United States and internationally. At present, the company flaunts a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for COLM’s 2026 sales implies growth of 2% from the year-ago figure, while EPS indicates a decline of 6.2%. Columbia Sportswear has delivered a trailing four-quarter earnings surprise of 25.2%, on average.

Vince Holding VNCE offers a broad range of women's and men's ready-to-wear, including its signature cashmere sweaters, leather jackets, luxe leggings, dresses, silk and woven tops, denim and footwear. At present, the company sports a Zacks Rank #1.

The Zacks Consensus Estimate for Vince Holding’s fiscal 2025 sales and earnings implies growth of 2.1% and 26.3%, respectively, from the year-ago figures. VNCE has delivered a trailing four-quarter negative earnings surprise of 229.6%, on average.

Ralph Lauren Corporation RL is a major designer, marketer and distributor of premium lifestyle products in North America, Europe, Asia and internationally. At present, the company holds a Zacks Rank of 2.

The Zacks Consensus Estimate for Ralph Lauren’s fiscal 2026 sales and earnings implies growth of 12.4% and 31.8%, respectively, from the year-ago figures. RL has delivered a trailing four-quarter earnings surprise of 9.7%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Columbia Sportswear Company (COLM): Free Stock Analysis Report

Ralph Lauren Corporation (RL): Free Stock Analysis Report

Crocs, Inc. (CROX): Free Stock Analysis Report

Vince Holding Corp. (VNCE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet