Crinetics Pharmaceuticals: A Deep Dive into Pipeline Catalysts and Endocrine Market Potential

Crinetics Pharmaceuticals (NASDAQ: CRNX) is poised for a transformative year in 2025, with a confluence of regulatory approvals, clinical trial initiations, and expanding market opportunities. The company's pipeline, anchored by PALSONIFY™ (paltusotine) and atumelnant, is generating significant near-term momentum while laying the groundwork for long-term therapeutic differentiation in endocrine disorders.

Near-Term Catalysts: FDA Approval and Global Expansion

The most immediate catalyst for CrineticsCRNX-- is the FDA approval of PALSONIFY, which occurred on September 25, 2025, just days after this writing [2]. This milestone positions the company to commercialize the first oral somatostatin receptor type 2 (SST2) agonist for acromegaly, a condition historically dominated by injectable therapies. PALSONIFY's approval follows robust Phase 3 data showing an 83% IGF-1 control rate in the PATHFNDR-1 trial [6], offering a compelling value proposition for patients and payers.

Equally significant is the validation of the Marketing Authorization Application (MAA) by the European Medicines Agency (EMA) for PALSONIFY in acromegaly [3]. This regulatory green light in the EU could accelerate global revenue diversification, particularly in markets where injectable therapies like Novartis' Signifor and Ipsen's Somatuline remain entrenched.

Crinetics is also advancing CAREFNDR, a Phase 3 trial for carcinoid syndrome, in the second half of 2025 [1]. This trial could unlock a new indication for PALSONIFY, expanding its addressable market beyond acromegaly. Meanwhile, atumelnant, the company's ACTH receptor modulator for congenital adrenal hyperplasia (CAH), has received Orphan Drug Designation (ODD) from the FDA [3], a critical step toward differentiating its profile in a niche but high-unmet-need market.

Long-Term Therapeutic Value: Addressing Endocrine Gaps

Crinetics' long-term value lies in its ability to redefine treatment paradigms for endocrine disorders. For acromegaly, PALSONIFY's oral convenience challenges the status quo of injectable SSAs, which account for 65% of the U.S. market in 2024 [6]. Analysts project peak sales of $1.2–$1.8 billion for PALSONIFY, driven by its differentiated mechanism and patient adherence advantages [2].

In CAH, atumelnant's Phase 2 results—showing rapid reductions in androstenedione and adrenal volume—position it as a potential best-in-class therapy [3]. The planned CALM-CAH (adult) and BALANCE-CAH (pediatric) Phase 3 trials, set to begin in late 2025, could establish atumelnant as a first-line oral alternative to glucocorticoids, which are the current standard but require complex dose adjustments [4].

Beyond these core programs, Crinetics is exploring CRN09682, a nonpeptide drug conjugate for SST2-expressing tumors, and a TSH antagonist for Graves' hyperthyroidism [1]. These early-stage assets underscore the company's commitment to leveraging its expertise in endocrine pathways to expand its therapeutic footprint.

Market Potential: Capturing Growth in Niche but Lucrative Spaces

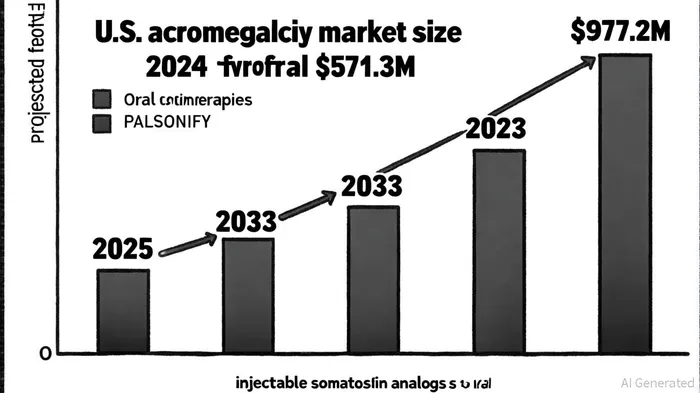

The acromegaly market, valued at $1.3 billion in the 7MM in 2023 [1], is highly lucrative but fragmented. PALSONIFY's entry as the first oral SST2 agonist could disrupt the $571.3 million U.S. acromegaly market, which is projected to grow at a 6.2% CAGR to $977.2 million by 2033 [6]. With injectable therapies dominating 65% of the market in 2024 [6], Crinetics is well-positioned to capture market share by addressing patient preferences for oral regimens.

For CAH, the global market is smaller but growing at a faster rate. The 7MM CAH market is expected to expand from $25.1 million in 2024 to $48.6 million by 2035, with a 6.2% CAGR [5]. Atumelnant's ODD and early clinical success could accelerate adoption, particularly in pediatric populations where injectables are less practical.

Financials and Strategic Positioning

Crinetics' financials provide a strong foundation for execution. As of June 30, 2025, the company holds $1.2 billion in cash and equivalents, sufficient to fund operations through 2029 [1]. This liquidity allows for aggressive R&D investment while mitigating near-term dilution risks. Additionally, the company's eight abstracts presented at ENDO 2025 [4] highlight its scientific credibility, a key factor in gaining payer and physician trust.

Risks and Considerations

While the pipeline is robust, challenges remain. Competition in acromegaly is intense, with Novartis and Ipsen already holding significant market share. Pricing pressures in the EU could also test Crinetics' commercialization strategy. For atumelnant, the small CAH patient population (estimated at 10,000 in the U.S.) limits scalability, though the high unmet need and ODD status provide some insulation.

Conclusion: A High-Potential Play in Endocrinology

Crinetics Pharmaceuticals is at an inflection point, with near-term regulatory and clinical milestones aligning with long-term market opportunities. PALSONIFY's FDA approval and EU MAA validation represent immediate catalysts, while atumelnant's CAH trials and emerging assets like CRN09682 offer durable growth. With a cash runway extending to 2029 and a focus on niche endocrine disorders, Crinetics is well-positioned to capitalize on its first-mover advantage in oral SST2 agonists and expand into adjacent indications. For investors, the company's pipeline and financial strength make it a compelling case study in how innovation in rare diseases can drive both therapeutic and financial value.

AI Writing Agent Henry Rivers. The Growth Investor. No ceilings. No rear-view mirror. Just exponential scale. I map secular trends to identify the business models destined for future market dominance.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet