Credit Scoring's Regulatory Crossroads: Is FICO's Decline a Buying Opportunity or a Structural Shift?

The credit scoring industry is at a pivotal juncture. Regulatory approvals for AI-driven models and shifts in consumer data usage are upending the dominance of legacy firms like FICOFICO--. For investors, this raises a critical question: Is the recent volatility in FICO's stock a fleeting opportunity to buy dips, or does it signal an irreversible shift toward agile competitors like VantageScore and Upstart?

The Regulatory Tipping Point

The Federal Housing Finance Agency's (FHFA) 2025 decision to mandate VantageScore 4.0 for government-backed mortgages was a seismic moment. FICO's stock plummeted 17% overnight as its near-monopoly in mortgage scoring crumbled. This move was not just about competition—it was a regulatory rebuke of FICO's aggressive pricing, which had surged 400% since 2022.

The EU's AI Act adds another layer of pressure. By 2026, credit scoring models must comply with strict transparency and bias-mitigation rules, favoring AI platforms like ZestFinance (which already integrates “explainable AI”) over FICO's proprietary, opaque algorithms. Meanwhile, the U.S. Senate's proposed OBBB Act—a federal moratorium on state AI regulations—could strip FICO of its leverage to push price hikes, as states like Colorado and California have already mandated model transparency.

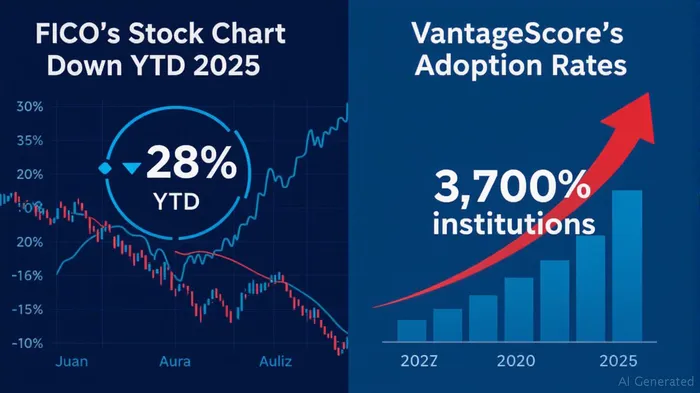

FICO's Vulnerabilities: Pricing Power vs. Regulatory Risk

FICO's revenue growth (14.7% in 2023) was fueled by its dominance in mortgage scoring. But its stock has cratered 28% over six months in 2025 due to:

- Regulatory Backlash: The CFPB's focus on fair lending has targeted FICO's legacy models, which critics argue perpetuate racial disparities.

- Competitor Inroads: VantageScore's tri-bureau data integration and inclusion of alternative metrics (e.g., rent payments) now scores 33 million more consumers than FICO, including marginalized groups.

- Overvaluation: FICO's P/E ratio of 75x in 2025 vs. Equifax's 15x suggests investors are pricing in existential risks.

The data is stark: VantageScore's usage has grown 55% since 2022, while FICO's market share in mortgages has dropped from 85% to 60%.

The Case for Agile Competitors

AI-driven upstarts are not just nipping at FICO's heels—they're rewriting the rules.

- Upstart: Uses AI to analyze 3,000+ data points (beyond traditional credit files), reducing APRs for underbanked borrowers by 12%. Its stock rose 40% in 2024 as it secured partnerships with regional banks.

- Zest AI: Focuses on compliance-first AI, offering lenders tools to audit bias in real time—a direct answer to the CFPB's demands.

- Global Reach: The EU's AI Act will favor firms like these, which already have transparency frameworks in place.

Investment Implications: Structural Shift or Buying Opportunity?

Bear Case for FICO:

- Its reliance on mortgage scoring is eroding. By 2026, lenders must submit both FICO and VantageScore for GSE loans, diluting FICO's pricing power.

- Software segment growth (slowed to 20% ARR in 2025) may not offset core declines.

Bull Case for FICO:

- Its Falcon Fraud Detection and analytics platforms still hold value. If FICO pivots to a “platform-as-a-service” model, it could stabilize.

Actionable Takeaways:

1. Avoid FICO's stock unless it slashes prices and diversifies beyond mortgages. Its valuation assumes no structural shift, which looks risky.

2. Allocate to AI-first firms: UpstartUPST-- and Zest AI offer exposure to regulatory tailwinds and inclusive data trends.

3. Monitor the OBBB Act: If it passes, it could freeze state-level reforms, giving FICO temporary respite—but long-term, transparency is inevitable.

Conclusion: The Writing Is on the Wall

The era of FICO's monopoly is ending. While its legacy systems still underpin much of the credit infrastructure, regulatory pressure, rising competition, and the AI revolution are structural forces favoring agile, transparent alternatives. For investors, this is less a “buy the dip” scenario and more a call to reallocate capital toward companies that can thrive in a post-FICO world.

The chart tells the story: FICO's decline isn't a blip. It's a new reality.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet