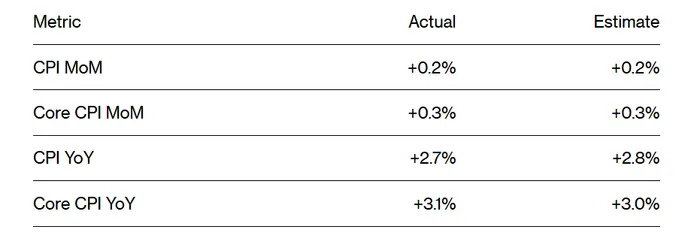

CPI Mild at 2.7%, Sep. Rate Cut Odds Jump to 95%

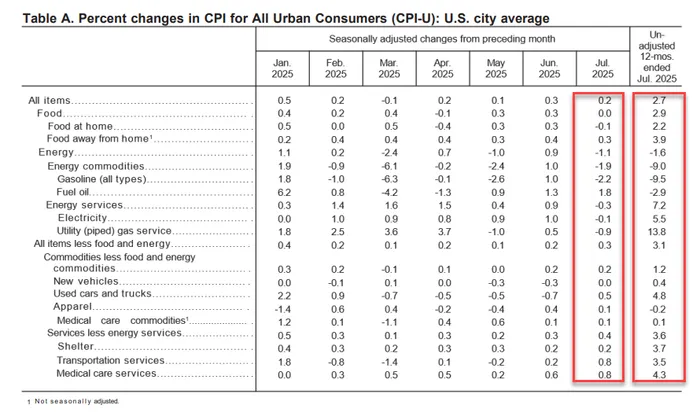

The U.S. July CPI revealed mild inflation. Specifically, CPI rose 2.7% YoY, below the expected 2.8%, and 0.2% MoM, in line with forecasts.

Excluding volatile food and energy prices, core CPI rose 3.1% YoY, slightly above the expected 3.0%, while the monthly increase was 0.3%, matching expectations.

Following the release, markets priced in a 95% probability of a Federal Reserve rate cut in September, up from 88% previously.

U.S. stocks opened higher, with the S&P 500 up 0.4%.

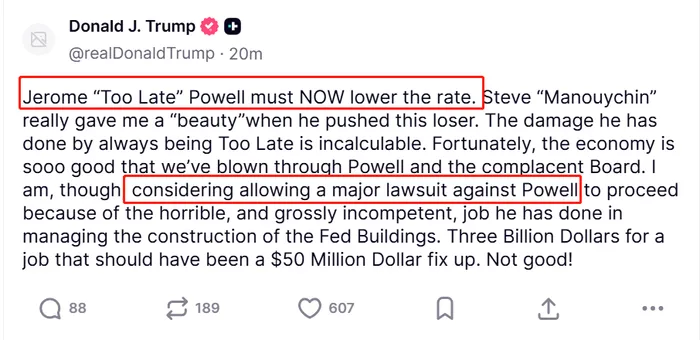

President Donald Trump criticized Fed Chair Jerome Powell on social media for moving too slowly, insisting rates should be cut immediately. He also threatened to file a major lawsuit over the Fed’s luxury renovations.

Energy Prices Drive Mild CPI

The biggest factor behind the modest July CPI rise was lower energy prices.

For goods heavily affected by tariffs, inflation remained limited. Clothing prices fell year-on-year and rose only 0.1% month-on-month. Furniture and household goods rose 2.4% year-on-year and 0.7% month-on-month, while audio-visual products climbed 0.8% month-on-month. Tariffs have not triggered a significant surge in the cost of essential goods.

Michelle Meyer, Chief Economist at MastercardMA--, noted that inflation is concentrated in products such as large appliances and car tires—items consumers rarely purchase. Furniture is rising in price, but it is not an essential purchase.

Services Inflation, Not Tariffs, Drives Price Gains

In sectors less affected by tariffs, services were the biggest CPI driver. Airfares jumped 4.0% month-on-month—the largest increase in three years—after a 0.1% drop in June. Auto insurance rose 5.3%. The healthcare index increased 0.8% month-on-month, with dental services seeing particularly sharp gains.

The surge in services prices is unrelated to tariffs. UBSUBS-- Chief Global Economist Alan Detmeister attributed the increases to President Trump’s strict crackdown on illegal immigration, which has sharply raised prices in labor-intensive industries such as landscaping, laundry, and personal care services.

Analysts View September Cut as Certain

Following the data, analysts broadly agreed that a September Fed rate cut is “a done deal,” with debate focused on whether it will be 25 or 50 basis points.

Nick Timiraos, often dubbed the “Fed Whisperer,” said the July CPI report further boosted the likelihood of a cut, noting that controlled inflation and a weakening labor market removed a key obstacle to easing.

Bloomberg’s Chief U.S. Rates Strategist Ira Jersey said the mild CPI suggests the upcoming Personal Consumption Expenditures (PCE) index will return close to the Fed’s 2% target, making a September cut likely and supporting further stock gains.

PIMCO economist Tiffany Wilding said tariffs have had little impact on goods inflation, leaving price pressures well-contained—a positive sign for the Fed.

CreditSights’ Head of Macro Strategy Zachary Griffiths said that while the report was neutral overall, weakening employment prospects make a 50 basis point cut in September more likely, as the labor market has become the Fed’s main concern.

Some Warn of Future Tariff Risks

However, some analysts warned the Fed’s inflation fight is not over.

Principal Asset Management’s Chief Global Strategist Seema Shah said that as goods inventories shrink, the inflationary impact of tariffs could intensify in the coming months. While a September cut is almost certain, decisions for October, December, and beyond will be more complex.

Katherine Judge of the Canadian Imperial Bank of Commerce reiterated her view that while automakers have so far absorbed tariffs, they may pass on costs to consumers through price hikes once new models hit the market.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet