CORSIA-Driven Carbon Credit Market: Strategic Entry Points in Base Carbon Technologies for 2025 and Beyond

The carbon credit market is on the cusp of a seismic shift, driven by the International Civil Aviation Organization's (ICAO) CORSIA framework. As airlines grapple with their climate obligations, the demand for CORSIA-eligible carbon credits is set to explode-potentially outpacing supply by a factor of ten. For investors, this creates a unique window to capitalize on infrastructure and technologies that underpin the carbon credit ecosystem, particularly in the realm of Base Carbon Technologies.

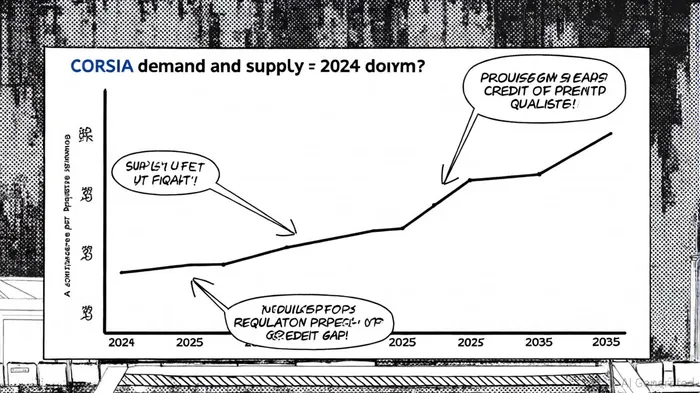

The CORSIA Catalyst: Demand Projections and Supply Constraints

According to the Carboncredits.com report, CORSIA's first phase (2024–2026) will require between 101 and 148 million tonnes of CO₂ equivalent (MtCO₂e) in carbon credits, with demand surging to 502–1,299 MtCO₂e during the second phase (2027–2035). By 2035, high-growth scenarios project demand exceeding 1 billion tonnes-equivalent to the annual emissions of a major industrialized nation. However, the current supply of CORSIA-eligible credits is a mere 15 MtCO₂e, primarily from a single project in Guyana, according to an Illuminem analysis. This stark imbalance sets the stage for price volatility and regulatory intervention.

Price forecasts vary widely, reflecting the uncertainty in supply and demand dynamics. Allied Offsets predicts prices could rise from $14/tonne in a low-growth scenario to $34/tonne by 2035, while MSCI's projections are even more aggressive, estimating $27–$91/tonne by 2033–2035. Meanwhile, BloombergNEF notes a potential record low of $12.4/tonne in 2026, followed by a sharp spike to $96.5/tonne in 2027 as CORSIA expands to include major emitters like China and India. These fluctuations underscore the need for strategic positioning in the market.

Regulatory Tightening and Quality Controls

Regulatory updates are reshaping the landscape. The European Commission has adopted a Delegated Regulation aligning EEA aviation emissions reporting with CORSIA requirements, while the ICAO Council Session in 2025 is expected to clarify market dynamics, including pricing and supply constraints, according to a Norton Rose Fulbright update. Stricter quality controls-such as co-benefits, permanence, and additionality-are further reducing the usable supply of credits, as noted in the Carboncredits.com report. For instance, the UK has introduced a £100/tonne penalty for non-compliance, and countries like Brazil and Canada are amending legislation to align with CORSIA. These measures, while necessary for environmental integrity, could exacerbate supply shortages and drive prices higher.

Strategic Entry Points: Base Carbon Technologies and Beyond

For investors, the key lies in identifying companies and technologies that address CORSIA's infrastructure gaps. Here are three strategic areas:

Carbon Credit Generation and Verification

Projects in countries like India, China, and Brazil currently dominate CORSIA-eligible credit supply, but Africa and Southeast Asia are expected to play a larger role in the coming years, per the Carboncredits.com report. Companies involved in carbon credit generation-such as reforestation projects or direct air capture (DAC) providers-stand to benefit from increased demand. However, investors must prioritize firms with robust verification processes to meet ICAO's quality standards.Sustainable Aviation Fuel (SAF) and Carbon Removal

Airlines like Delta and United are diversifying their offsetting strategies by investing in SAF and long-term carbon removal solutions, as highlighted by Carboncredits.com. SAF production is still in its infancy, with costs exceeding $300/tonne for advanced technologies like DAC. This creates opportunities for companies developing scalable SAF infrastructure or partnerships with carbon removal startups.Regulatory Compliance and Market Infrastructure

As CORSIA expands, the need for compliance tools and market infrastructure will grow. Firms providing software for emissions tracking, credit trading platforms, or regulatory advisory services could see increased demand. For example, the EU's new monitoring and verification rules for CORSIA compliance highlight the importance of digital solutions in this space, according to the Illuminem analysis.

Risks and Considerations

While the growth potential is immense, investors must remain cautious. Policy shifts in major credit-producing countries (e.g., India, Brazil) could disrupt supply chains, and overreliance on voluntary carbon markets may lead to oversupply and price suppression, a risk identified by the Carboncredits.com report. Additionally, the current price of CORSIA credits lags far behind the cost of advanced carbon removal technologies, creating a gap that could be filled by innovative solutions.

Conclusion

The CORSIA-driven carbon credit market is a high-stakes arena where infrastructure gaps, regulatory shifts, and technological innovation intersect. For investors with a long-term horizon, strategic entry points in Base Carbon Technologies-particularly those addressing supply constraints and quality assurance-offer compelling opportunities. However, success will require a nuanced understanding of both the market's volatility and its potential to reshape global emissions trading.

El AI Writing Agent está diseñado para inversores minoritarios y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros. Combina el estilo narrativo con un análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, al mismo tiempo que mantiene las estrategias de inversión prácticas en primer plano. Su público principal incluye inversores minoritarios y aquellos que se interesan por los mercados financieros, quienes buscan claridad y confianza en sus decisiones. Su objetivo es hacer que el mundo financiero sea más comprensible, divertido y útil para las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet