CoreWeave Slides Below $100 as Supply Snags Test AI Cloud Darling’s Debt-Fueled Expansion

CoreWeave (CRWV), one of the fastest-growing players in the emerging “neocloud” infrastructure space, delivered a third-quarter report that underscored both the promise and the growing pains of building out AI-era compute capacity at breakneck speed. The company — which powers workloads for customers like Meta, OpenAI, and multiple hyperscalers — posted triple-digit revenue growth and an enormous backlog expansion, but investors are fixating on guidance cuts, supply chain delays, and mounting balance-sheet strain. Shares were down roughly 9% in premarket trading Tuesday, slipping below the key $100 level and potentially eyeing support in the $85–$90 zone that held in early September.

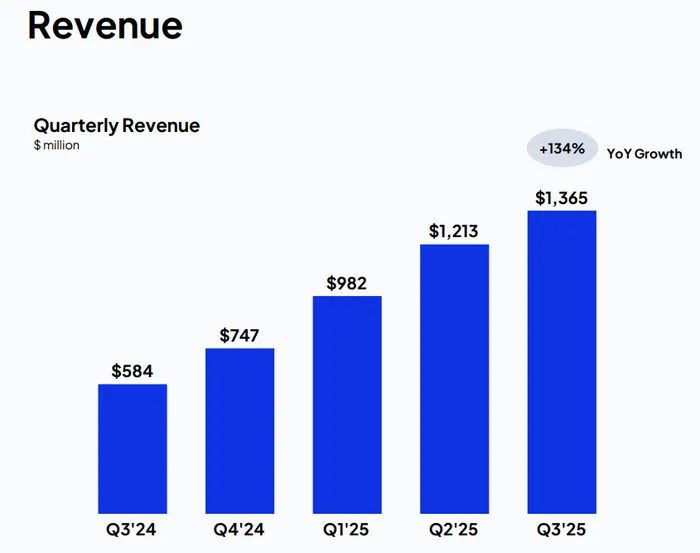

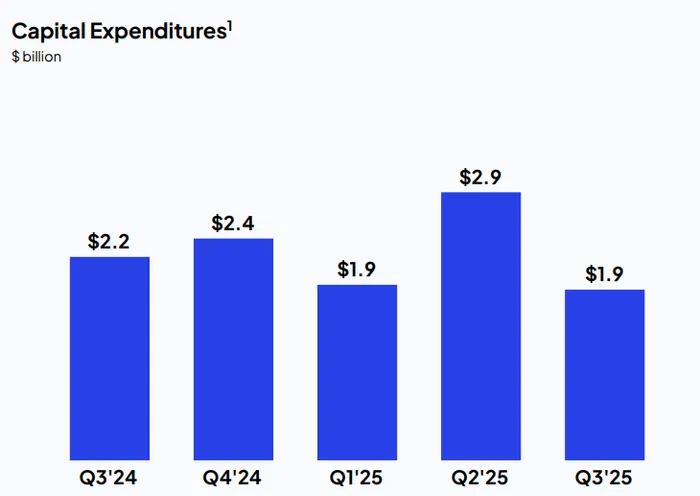

In the third quarter, CoreWeave reported revenue of $1.36 billion, a 134% year-over-year surge that handily beat consensus estimates of $1.28 billion. Adjusted EBITDA climbed to $838 million with a 61% margin, while adjusted operating income totaled $217 million, reflecting solid execution in scaling operations. Despite the revenue beat, profitability remained elusive, with a net loss of $110 million and an adjusted net loss of $41 million. Interest expense ballooned to $311 million, highlighting the growing cost of servicing the company’s expanding debt pile. Capital expenditures for the quarter reached $1.9 billion, below prior expectations due to construction delays at one of its major data center partners — an issue management characterized as temporary. Construction in progress rose to $6.9 billion, reflecting heavy investment in facilities awaiting power delivery and final fit-out.

On the balance sheet, CoreWeaveCRWV-- continues to tap multiple funding channels to finance its growth. The company raised $1.75 billion in senior unsecured notes due 2031 at a 9% coupon and closed a $2.6 billion delayed-draw term loan facility (DDTL 3.0) at SOFR +4%. It also amended its DDTL 2.0 facility, adding a $3.0 billion tranche at slightly higher rates, while satisfying preferred equity obligations that boosted shareholders’ equity by $1.2 billion. Liquidity remains solid, with $3 billion in cash and equivalents, but leverage is now firmly in focus. JPMorgan, which downgraded the stock to Neutral with a $110 price target, cited “mounting supply-chain pressures” and execution risk, even as it maintained long-term optimism around CoreWeave’s AI exposure.

The biggest sticking point for investors this quarter was CoreWeave’s revised outlook for FY2025, which now calls for revenue of $5.05–$5.15 billion, down from $5.15–$5.35 billion and below Wall Street’s $5.29 billion consensus. The company also reduced its CapEx outlook to $12–$14 billion from a prior range of $20–$23 billion, citing project delays and a shift of spending into next year. Management said much of the deferred investment will roll into the first quarter of 2026, with construction in progress absorbing the gap. CFO Nitin Agrawal guided for adjusted operating income of $690–$720 million and noted that interest expense will remain heavy, estimated at $1.21–$1.25 billion next year. Importantly, he suggested 2026 CapEx could more than double 2025 levels as capacity expansion resumes in earnest.

The delay stems from power delivery constraints at a single data center provider, widely speculated to be Core Scientific (CORZ). CEO Michael Intrator emphasized that while this would push some near-term deployments, the affected customer has already agreed to an adjusted schedule that preserves the full contract value. In total, CoreWeave now boasts a $55.6 billion revenue backlog, up nearly 100% sequentially and over 270% year-over-year, reflecting large new multi-year deals: a $14.2 billion partnership with Meta, an expanded $6.5 billion agreement with OpenAI, and a $6.3 billion collaboration with Nvidia to scale GPU infrastructure. Active power capacity reached 590 megawatts, with 2.9 gigawatts contracted and plans to exceed 850 MW by year-end. The company also launched CoreWeave Ventures to invest in emerging AI infrastructure startups and introduced CoreWeave Federal, with NASA already onboarded as a client.

Still, rapid scaling has come with trade-offs. Operating margin has fallen sharply amid soaring infrastructure and technology costs, and interest expenses now absorb a growing share of operating cash flow. The company’s strategy — build capacity at full throttle even as short-term profitability declines — mirrors early hyperscaler expansion phases but carries greater risk given its smaller scale and reliance on external data center partners. JPMorgan and other analysts expressed concern about execution risk and capital intensity, noting that while demand remains “insatiable,” forecasting the timing of deliveries and power availability is increasingly complex.

During the earnings call, Intrator and Agrawal sought to reassure investors that the worst of the supply chain headwinds would be resolved by Q1 2026. They highlighted steps to diversify data center providers, expand self-build initiatives, and increase operational control through new facilities in the U.S. and Europe, including a $6 billion project in Lancaster, Pennsylvania and a £2.5 billion investment in the U.K.. Intrator downplayed concerns about overcapacity, arguing that the company’s infrastructure is highly fungible and can be reallocated across clients if needed. He also noted that the company’s powered shell challenges were isolated rather than systemic: “It’s not a challenge for power — really, the challenge is the powered shell.”

Investor sentiment remains divided. Bulls see CoreWeave as a pure-play on the AI cloud buildout, with unmatched backlog momentum and strategic partnerships positioning it as a key enabler of the next compute cycle. Bears, meanwhile, point to the deteriorating balance sheet, steep capital intensity, and the company’s exposure to a still-nascent market that could see volatility if AI spending normalizes. The downgrade from JPMorgan underscores the near-term execution risks, though analysts largely continue to view the company as a long-term beneficiary of AI infrastructure demand.

Technically, the stock’s 9% premarket slide has it breaking below the $100 psychological threshold. The next key support lies in the $85–$90 range, which held in early September. While the near-term narrative is dominated by supply bottlenecks and funding costs, the broader trend remains one of aggressive infrastructure expansion in response to unprecedented AI demand. If CoreWeave can navigate its supply-chain bottlenecks and resume full deployment early next year, investors may view this quarter as a pause in a much larger growth story. But for now, the balance of risk is shifting toward execution — not demand.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet