CoreWeave's AI Bet Pays Off Amid Supply Crunch, But Delays Cloud the Outlook

In the volatile world of AI infrastructure, CoreWeaveCRWV-- Inc. has emerged as a pivotal player, renting out NvidiaNVDA-- Corp.'s coveted graphics processing units to tech giants hungry for computing power. Fresh off its third-quarter earnings report, the cloud-computing firm delivered a performance that underscored the relentless demand for AI capabilities—yet it also highlighted the precarious tightrope of rapid expansion, supply bottlenecks, and mounting capital demands. With shares dipping in after-hours trading despite beating expectations, CoreWeave's results offer a microcosm of the broader AI boom: explosive growth tempered by execution risks.

The Earnings Beat: Revenue Surge and Narrowed Losses

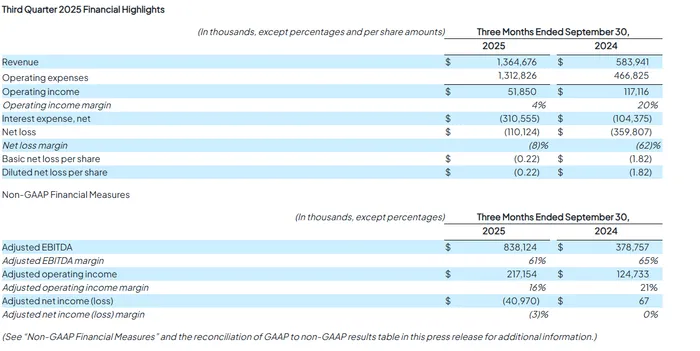

CoreWeave's third-quarter numbers painted a picture of robust momentum. Revenue climbed 134% year-over-year to $1.36 billion, eclipsing Wall Street's consensus estimate of $1.29 billion. This surge, driven by multibillion-dollar deals with hyperscalers like Microsoft Corp., Alphabet Inc.'s Google, and Meta Platforms Inc., helped narrow the net loss to $110 million from $360 million a year earlier. On an adjusted basis, excluding items like stock compensation, the loss per share came in at 22 cents—far better than the anticipated 40-cent deficit.

CEO Michael Intrator attributed the strength to "disciplined execution" across the business, emphasizing CoreWeave's role as the "essential cloud for AI." The company's backlog swelled to $55.6 billion by quarter's end, with power under contract rising to 2.9 gigawatts from 2.2 gigawatts just three months prior. Analysts at Jefferies, led by Brent Thill, had projected recurring purchasing orders to double to $60 billion, a mark the actual figures approached closely, signaling sustained client commitment.

This performance arrives against a backdrop of investor skepticism. Last week's market selloff hammered AI-related stocks, with CoreWeave's shares plunging 22% amid broader concerns over excessive spending by clients like Meta and Microsoft. The S&P 500 notched its first weekly loss in a month, amplifying scrutiny on the "circularity" of AI deals, many orbiting OpenAI. Yet CoreWeave's results affirm that demand for AI infrastructure remains insatiable, outstripping supply and justifying the company's aggressive buildout.

Strategic Deals Fuel the Fire

The quarter brought a flurry of high-profile partnerships that solidified CoreWeave's position as the go-to "neocloud" provider. A $6.5 billion expansion with OpenAI Group PBC stands out, alongside a six-year pact with Meta potentially worth $14.2 billion. An additional contract with an undisclosed leading hyperscaler further diversified the revenue stream, though Meta, Microsoft, and Alphabet still account for the bulk of sales.

Bloomberg Intelligence analyst Anurag Rana notes that this demand mitigates risks from customer concentration. "Even if a top customer were to leave, another client would likely rush in," he observed, pointing to the supply-constrained environment. Intrator echoed this on the earnings call, describing the market as one where CoreWeave's powered-shell data centers—prepped facilities ready for rapid deployment—are in hot demand.

However, the company's dependence on a handful of giants isn't without peril. Questions linger about debt loads and the sustainability of these arrangements, especially as AI hype faces headwinds. Taiwan Semiconductor Manufacturing Co.'s recent report of slowing revenue growth adds to the uncertainty, even as Nvidia chases more chip orders.

Market Reaction: Gains Erased by Guidance Miss

Despite the earnings triumph, CoreWeave's stock tumbled nearly 6% in late trading, erasing much of the 6.1% intraday gain ahead of the report. The culprit? A full-year revenue forecast of $5.05 billion to $5.15 billion, falling short of the $5.29 billion analysts expected. This tepid outlook stems from construction delays at a third-party data center, one of 32 in the portfolio.

Intrator downplayed the issue, assuring that the affected customer's contract value remains intact, with delivery schedules adjusted accordingly. "The delay won't impact our backlog," he stressed. Still, the setback underscores the challenges of scaling infrastructure amid a frenzied AI race. Chief Financial Officer Nitin Agrawal revealed that 2026 capital expenditures will exceed double the current year's $12 billion to $14 billion projection, with roughly two-thirds of this year's spend—about $14 billion—slated for the fourth quarter.

This capex escalation reflects the need to meet surging demand, but it also pressures margins. Operating margins are expected to dip to 14.3% from over 21% a year ago, a trend that began eroding after the second-quarter report in August, when shares sank 21% on a wider-than-expected loss and disappointing guidance.

From IPO Turbulence to Outperformance

CoreWeave's journey since its March initial public offering has been a rollercoaster. Priced at $40 per share with Nvidia's backing to push it over the line, the stock has soared more than 160% overall, closing at $105.61 before the after-hours dip—vastly outperforming the Nasdaq's 32% gain in the same period. Yet volatility persists: down 30% since the August report, the shares reflect investor whiplash between AI euphoria and fiscal caution.

A recent setback came when Core Scientific Inc. shareholders rejected CoreWeave's $9 billion takeover bid on October 30, deeming it undervalued. Intrator affirmed the ongoing partnership, noting shared growth opportunities in data center capacity for AI providers. "Our vision and strategy remain unchanged," the company stated, opting not to sweeten the offer.

Looking Ahead: Scaling Profitably in a Supply-Constrained World

As CoreWeave navigates this landscape, the focus shifts to profitable scaling. Dave Mazza, CEO of Roundhill Financial, captures the investor mindset: "Doubling revenue is great, but if capex is climbing even faster, that math doesn’t work forever." With earnings reports from top clients like Meta and Microsoft showing unwavering AI commitments, CoreWeave's revenue should accelerate into 2026 as new capacity comes online.

Rana anticipates sales growth quickening next year, driven by this year's deferred capex. Thill at Jefferies expects upside to consensus estimates from recurring order growth, though guidance for fiscal 2026 remains elusive—potentially arriving next quarter.

The broader AI narrative adds intrigue. Hyperscalers insist on funding infrastructure amid outstripped supply, but mounting concerns over spending sustainability loom. CoreWeave's ability to generate positive cash flow in the next year or two could be the litmus test. "If they show a path to that, the market will give them credit," Mazza said.

In essence, CoreWeave's earnings reveal a company at the epicenter of AI's transformative wave—profiting handsomely from scarcity while grappling with the costs of abundance. As Intrator steers toward innovation and growth, investors will weigh whether this neocloud pioneer can convert its backlog into enduring profitability, or if delays and debt will dim its shine. With the AI trade under scrutiny, CoreWeave's next moves could redefine the sector's trajectory.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet