Core PCE Inflation Holds Steady: Strategic Implications for Capital Markets and Food Products

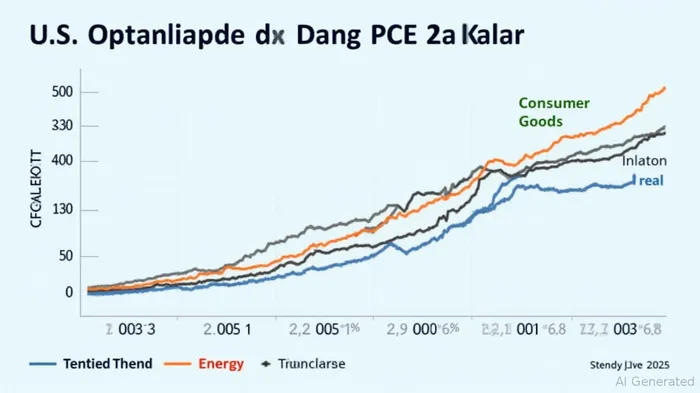

The July 2025 U.S. Core PCE Price Index, released on August 29, 2025, confirmed a year-over-year increase of 2.8%, matching market expectations and underscoring a stabilization in inflationary pressures. This data point, while not a surprise, reveals critical divergences in sector-specific inflation dynamics that investors must dissect to navigate the evolving economic landscape. With the Federal Reserve maintaining a cautious stance and internal policy debates intensifying, the Core PCE's stability masks underlying shifts in capital markets and food products industries that demand strategic reallocation.

Capital Markets: Financial Services as Inflation Winners

The Core PCE's stability belies a surge in portfolio management fees, a key component of the services category. As equity markets rebound, asset managers like BlackRock (BLK) and Vanguard (VGT) are seeing revenue growth driven by rising assets under management. This trend positions financial services as an inflation-resistant sector, with fee-based income insulating these firms from broader macroeconomic volatility. Investors should monitor BLK's quarterly fee revenue as a barometer for this tailwind, particularly as demand for managed investments remains elevated.

However, the sector is not without risks. The Federal Reserve's “higher for longer” interest rate environment pressures liquidity in high-yield sectors, favoring cash-generative industries like industrials over speculative tech plays. For defensive positioning, Treasury Inflation-Protected Securities (TIPS) remain a viable hedge against persistent inflation. Investors in financial services should prioritize firms with robust cost controls and diversified revenue streams to mitigate labor market tightening and operational cost pressures.

Food Products Industry: Tariffs and Supply Chain Pressures

The food products sector faces a dual challenge: stable food-at-home prices and rising food-away-from-home costs. While the Core PCE excludes food and energy, the broader PCE data for July 2025 highlights a 0.4% increase in dining-out costs, driven by labor and input expenses. Tariff policies, particularly the 50% copper tariff and potential hikes on pharmaceuticals and electronics, are exacerbating supply chain bottlenecks.

Procter & Gamble (PG), a bellwether for consumer goods, has announced price hikes to offset imported material costs, illustrating the sector's squeeze between rising input prices and consumer resistance. Furniture and recreation goods, which saw 1.3% and 0.9% price increases, respectively, are particularly vulnerable. Conversely, domestic manufacturing in industrial metals and logistics offers upside potential.

Investors should adopt a nuanced approach: shorting discretionary food-away-from-home stocks while overweighting domestic producers. ETFs like the iShares U.S. Home Construction ETF (ITB) may benefit from inflation-linked demand for housing and related goods. For hedging, the Citi Inflation Surprise Index—which has shown recent volatility—can signal unexpected shifts in consumer spending patterns.

The Fed's Dilemma and Sector Rotation Strategies

The Federal Reserve's decision to keep rates unchanged in July 2025, despite two dissenting votes, reflects internal divisions over inflation's trajectory. While the 2.8% core PCE aligns with the 2% target in the medium term, the Fed's focus on transitory pressures may delay rate cuts until 2026. This environment favors cash-generative sectors (e.g., industrials) over high-yield real estate or consumer discretionary.

For capital markets, a strategic shift toward financial services and domestic manufacturing is warranted. In food products, sector rotation should prioritize defensive producers with pricing power while avoiding discretionary sub-sectors. The key to outperforming lies in precision: leveraging sector-specific ETFs and hedging tools to capitalize on divergent inflationary dynamics.

Conclusion: Navigating a Polarized Inflationary Landscape

The July 2025 Core PCE data signals a departure from one-size-fits-all inflation narratives. For capital markets, financial services are well-positioned to benefit from rising asset management fees and equity market rebounds. For food products, the impact of tariffs and supply chain bottlenecks demands a careful balance between cost management and consumer affordability. Investors who adopt data-driven, agile strategies—focusing on inflation-resistant sectors and hedging against energy and discretionary underperformance—will be best poised to thrive in this polarized environment.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet