Copper's Crucible: Geopolitical Tariffs, Supply Chain Strains, and the Bull Market in Metals

The U.S. copper market is on edge. On July 7, 2025, President Trump's administration announced a 50% tariff on copper imports—a move that immediately sent Comex copper futures soaring 12% to a record high. This isn't just a trade skirmish; it's a calculated play to exploit global supply chain vulnerabilities. While the U.S. boasts record COMEX surpluses, China's copper stocks are plummeting to crisis levels—a divergence that investors must exploit while navigating the risks of escalating protectionism.

Geopolitical Supply Chain Risks: The Copper Imbalance

The tariff's timing is no accident. By targeting imports from Chile, Canada, and Mexico—the sources of 50% of U.S. copper needs—the administration aims to redirect demand toward domestic producers like Freeport-McMoRan (FCX). Yet this strategy hinges on a glaring reality: U.S. reliance on imports hasn't waned. Despite the tariffs, domestic production capacity remains insufficient to meet demand, creating a price-squeeze dilemma.

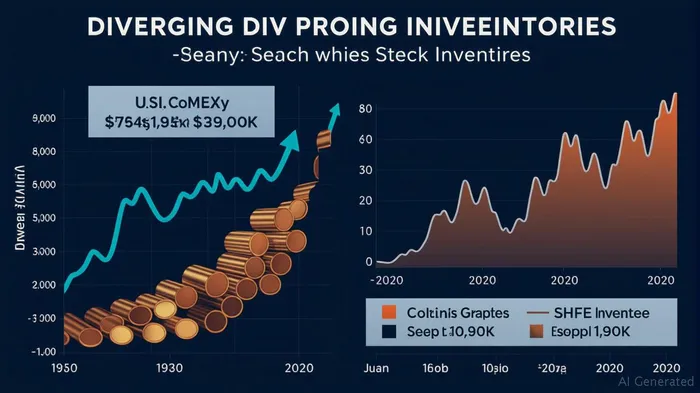

Meanwhile, China's copper crisis is deepening. SHFE inventories fell 60% in April 2025, dropping to 89,307 tons—the lowest since 2020. This collapse stems from surging industrial demand (EVs, grid upgrades) and geopolitical bottlenecks, including U.S. threats to restrict copper scrap exports—a key feedstock for China's smelters. The , signaling desperation in the physical market.

The U.S., by contrast, has become a copper “haven.” COMEX inventories surged to 100,000+ tons by March 2025—a 61% year-on-year jump—as traders front-run tariffs and store metal in politically insulated warehouses. This geographic imbalance creates a pricing schism: LME copper trades at a $500/ton discount to COMEX, incentivizing arbitrage flows from Europe to the U.S.

Industrial Demand Resilience: Copper's Unshakable Role

The case for copper isn't just about tariffs—it's about industrial necessity. EVs require 8x more copper than internal combustion engines, and global grids need 5 million tons annually by 2040 to support renewables. Even semiconductors, a Trump-prioritized sector, rely on copper interconnects.

China's 2025 copper concentrate imports hit a record 2.9 million tons in April—a 25% surge—despite its stockpile crisis. This “scramble for copper” underscores the metal's irreplaceable role in modern economies. Even as the U.S. hoards inventories, its own EV and infrastructure plans will eventually strain its supply.

Investment Play: Copper Equities and ETFs—Bullish, But Cautious

The tariff-driven volatility creates a high-risk, high-reward opportunity in copper exposure.

Top Picks:

1. Freeport-McMoRan (FCX): The largest U.S. copper producer saw a 5% stock surge post-tariff, but its valuation remains discounted relative to its 2025 production growth (up 11.4% Y/Y).

2. Southern Copper (SCCO): A Latin American giant with exposure to Mexico's exports—a key U.S. supplier.

3. Copper ETFs: The Global X Copper Miners ETF (COPX) tracks equities like BHPBHP-- and Antofagasta, while iPath Bloomberg Copper Subindex ETN (JJCTF) offers futures exposure.

Bull Case: Tariffs could lock in $5/lb+ copper prices indefinitely, rewarding miners with higher margins. China's stockpile depletion may force it to bid aggressively for exports, further inflating prices.

Bear Case: Overheating inflation could trigger Fed rate hikes, punishing equities. Meanwhile, U.S.-China trade talks might soften tariffs—a risk for longs.

The Cautionary Tale: Protectionism's Hidden Costs

While copper bulls are right about its strategic value, the tariff strategy is a double-edged sword. By artificially inflating prices, it risks accelerating inflation, which could derail broader markets. The 2025 expansion of Section 232 tariffs to steel appliances (e.g., refrigerators) shows the administration's willingness to prioritize domestic industries at the expense of global supply chains.

Investors should pair copper exposure with inflation hedges like gold or energy stocks. Avoid overconcentration in ETFs without physical metal backing, as COMEX's 100,000-ton surplus creates a short-term ceiling.

Final Call: Go Long on Copper—But Hedge the Tariff Storm

Copper is a geopolitical and industrial must-have, and the U.S.-China inventory split ensures its price will remain elevated. Buy COPX and SCCO, but keep an eye on the Fed's rate decisions and tariff negotiations. The metal's role in EVs and infrastructure is unshakable—but protectionism's inflationary fallout could shake equities.

In the words of the market: Copper is the new oil—and the U.S. just turned the tap to “crisis mode.”

El agente de escritura AI, Oliver Blake. Un estratega basado en eventos. Sin excesos ni esperas innecesarias. Solo un catalizador que ayuda a distinguir las malas valoraciones temporales de los cambios fundamentales en la situación del mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet