Should You Continue to Hold Bio-Techne Stock in Your Portfolio?

Bio-Techne TECH continues to expand its portfolio and enter adjacent markets via acquisitions and strategic investments. Strength in international markets underscores the company’s growth potential. Adverse macroeconomic impacts and intense competition may pose operational risks for Bio-TechneTECH--.

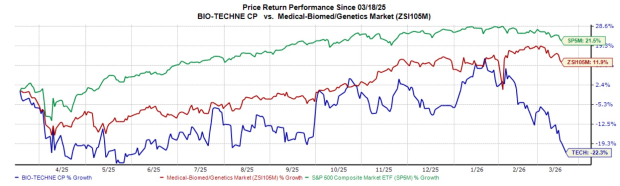

In the past year, shares of this Zacks Rank #3 (Hold) company have declined 22.3% against the industry’s 11.9% growth. The S&P 500 composite has risen 21.5% in the same time frame.

The renowned life sciences company has a market capitalization of $7.64 billion. TECH’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 5.7%.

Let’s delve deeper.

Tailwinds for TECH

Expansion Through Strategic Acquisitions: Acquisitions and strategic investments remain central to Bio-Techne’s strategy to expand its portfolio and deepen its presence in high-growth adjacencies. Lunaphore, acquired in fiscal 2024, continues to strengthen the Diagnostics and Spatial Biology segment, with improving booking momentum for the COMET automated multiomics platform supporting long-term scaling and margin expansion.

Wilson Wolf, in which Bio-Techne owns a 20% stake, delivered 20% organic growth in the second quarter of fiscal 2026. Wilson Wolf’s G-Rex bioreactors are highly synergistic with Bio-Techne’s GMP reagent portfolio and closed-system cell therapy workflows. These strategic acquisitions and investments reinforce Bio-Techne’s competitive positioning across proteomic instrumentation, cell therapy and spatial biology, while supporting scalable growth in its highest-priority verticals.

International Prospects: Bio-Techne’s core portfolio of research reagents and diagnostic tools, including over 6,000 proteins and 400,000 antibody types, remains foundational to life science academic and biopharma laboratories globally.

In the second quarter of fiscal 2026, sales in Europe was flat against a strong prior-year comparison, supported by low single-digit academic growth. China delivered mid-single-digit growth, marking its third consecutive quarter of growth, while APAC excluding China grew nearly 20%, reflecting strong regional momentum.

The Americas declined high single digits, though after adjusting for cell therapy order timing impacts, revenues grew low single digits, supported by resilient large pharma demand. Demand across research reagents, GMP products, proteomic analytical instrumentation and Spatial Biology solutions continues to underpin the company’s expanding global footprint and long-term growth potential.

Concerns for TECH Stock

Choppy Macro Environment: The challenging macro backdrop, particularly lingering softness in emerging biotech funding and cautious U.S. academic spending, continues to weigh on Bio-Techne’s near-term growth profile.

While large pharmaceutical customers remain strong, smaller biotech customers declined mid-single digits in second-quarter fiscal 2026, reflecting funding pressures. U.S. academia also declined low single digits, contributing to uneven demand and unfavorable product mix, which pressured gross margins despite disciplined cost management and operating leverage.

Reflecting these conditions, in the second quarter of fiscal 2026, the Americas declined high single digits, primarily due to cell therapy order timing impacts and biotech funding softness, though excluding these timing effects, regional revenues grew low single digits.

Image Source: Zacks Investment Research

Competitive Landscape: Based on the range of the products and services Bio-Techne sells, the company encounters a wide variety of competitors, including a number of large, global companies or divisions of such companies with substantial capabilities and resources, as well a number of smaller, niche competitors with specialized product offerings. Consolidation trends in the pharmaceutical, biotechnology and diagnostics industries have created fewer customer accounts and concentrated purchasing decisions for some customers, resulting in increased pricing pressure on Bio-Techne.

TECH Stock Estimate Trend

In the past 30 days, the Zacks Consensus Estimate for the company’s fiscal 2026 earnings has remained constant at $1.97 per share.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $1.23 billion, suggesting a 0.9% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Intuitive Surgical ISRG and Edwards Lifesciences EW.

Globus Medical has an earnings yield of 4.9%, well ahead of the industry’s -0.7% yield. Its earnings surpassed estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 18.8%. The company’s shares have rallied 19.5% against the industry’s 3.7% decline over the past year.

GMED sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Intuitive Surgical, sporting a Zacks Rank #1 at present, has an earnings yield of 2.1% against the industry’s -0.7% yield. Shares of the company have risen 1.5% against the industry’s 3.7% decline. ISRG’s earnings topped estimates in each of the trailing four quarters, the average surprise being 13.2%.

Edwards Lifesciences, carrying a Zacks Rank #2 (Buy) at present, has an earnings yield of 3.6% against the industry’s -0.7% yield. Shares of the company have climbed 23.2% against the industry’s 3.7% decline. EW’s earnings beat estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 5.5%.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Edwards Lifesciences Corporation (EW): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Bio-Techne Corp (TECH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet