Concentrix Outperforms Revenue Expectations: A Glimpse into BPO Sector Resilience

In the ever-evolving landscape of business process outsourcing (BPO), ConcentrixCNXC-- (CNXC) has emerged as a case study in resilience. The company's Q3 2025 results, released on September 25, 2025, underscore both the challenges and opportunities facing the sector. With revenue hitting $2.48 billion—a 4.0% year-on-year increase—Concentrix not only exceeded its internal guidance but also signaled its ability to navigate a competitive market[1]. Yet, beneath the surface of this growth lies a complex interplay of margin pressures, strategic reinvention, and sector-wide transformation that demands closer scrutiny for investors.

The Numbers: Growth, Margins, and Strategic Reinvestment

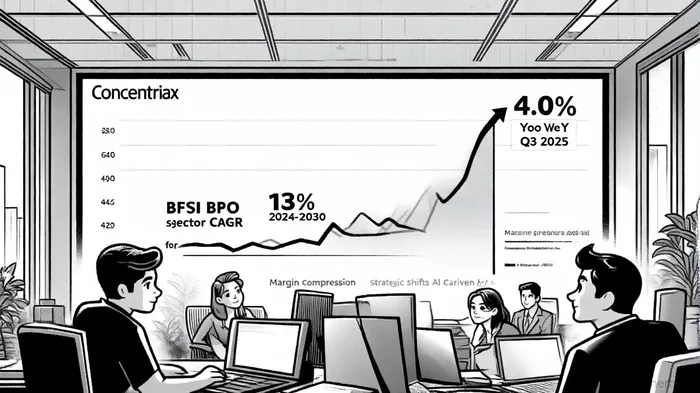

Concentrix's Q3 performance was marked by a 4.0% year-on-year revenue increase, driven by strong demand for integrated solutions combining customer experience (CX), artificial intelligence (AI), and IT services[1]. This growth, however, came at a cost. Non-GAAP operating income fell 7.8% to $305.1 million, while adjusted EBITDA declined 7.4% to $359.2 million, reflecting margin compression amid rising operational costs and competitive pricing pressures[1]. The disconnect between top-line growth and profitability raises questions about the sustainability of Concentrix's current model, particularly as the BPO sector shifts toward outcome-based contracts that prioritize value over volume[2].

Yet, the company's strategic investments in AI and hyper-automation offer a counterbalance. Initiatives like iX Hello—a GenAI self-service layer leveraging large-language models—position Concentrix to capitalize on the BFSI sector's demand for scalable, technology-driven solutions[2]. This aligns with broader industry trends: the BFSI BPO market, valued at $92.4 billion in 2024, is projected to grow at a 13% CAGR through 2030, driven by digital transformation and regulatory complexity[2]. For Concentrix, which derives 15.89% of its revenue from BFSI clients[2], this represents both a tailwind and a test of execution.

Sector Resilience and Competitive Positioning

The BPO sector's resilience in 2025 has been underpinned by its adaptability to macroeconomic headwinds. Geopolitical uncertainties, such as the Russia-Ukraine conflict, have accelerated the shift toward diversified, offshore operations in stable regions like India and the Philippines[1]. Concentrix's geographic footprint and focus on cloud-native delivery models—offering elastic, consumption-linked pricing—position it to benefit from this trend, particularly for small- and medium-sized enterprises (SMEs) seeking cost optimization[2].

However, the company faces stiff competition. Key players like Accenture, Cognizant, and Genpact are similarly leveraging AI and robotics process automation (RPA) to enhance efficiency[1]. Concentrix's differentiator lies in its client retention metrics: while specific figures for Q3 2025 are unavailable, industry data suggests the BFSI sector's average retention rate hovers around 74%[2]. Given Concentrix's long-term relationships—with 7 of the top 10 fintech companies and 8 of the top 10 European banks as clients[2]—its ability to maintain high retention will be critical to sustaining growth.

Investment Implications: Opportunity or Overreach?

For investors, Concentrix's Q3 results present a nuanced picture. On one hand, the company's revenue outperformance and strategic alignment with BFSI's digital transformation make it an attractive play in a high-growth sector. Its 8.2% dividend increase and $42.2 million in share repurchases further underscore management's commitment to shareholder returns[1]. On the other, margin compression and the absence of granular BFSI client retention data highlight risks that cannot be ignored.

The broader BPO market, valued at $164.83 billion in 2023, is forecasted to reach $339.3 billion by 2032—a CAGR of 8.35%[1]. Within this, the BFSI subsector's 9.1% CAGR through 2028[2] suggests Concentrix's focus on this area is well-placed. Yet, the transition from labor arbitrage to technology-enabled solutions requires significant reinvestment, which could strain margins in the short term.

Conclusion: A Calculated Bet in a Transformative Sector

Concentrix's Q3 performance is a testament to the BPO sector's adaptability—and its vulnerabilities. While the company's revenue beat and strategic pivot toward AI-driven solutions position it to capitalize on BFSI's growth, investors must weigh these strengths against margin pressures and competitive dynamics. For those with a long-term horizon, Concentrix offers a compelling case: a firm navigating the crosscurrents of technological disruption and sector consolidation, with the potential to emerge stronger if its reinvention pays off.

In the end, the question is not just whether Concentrix can sustain its growth, but whether it can redefine what growth means in an industry where the rules are being rewritten.

Eli escribe principalmente para inversores, profesionales del sector y personas que estén interesadas en la economía, y su estilo es asertivo y bien investigado, con la intención de desafiar perspectivas comunes. Su análisis adopta una posición crítica, pero equilibrada, en relación con las dinámicas del mercado, con el objetivo de educar, informar y, a veces, interrumpir las narrativas habituales. Mientras mantiene su credibilidad e influencia dentro del periodismo financiero, Eli se centra en la economía, las tendencias del mercado y el análisis de inversiones. Su estilo analítico y directo asegura la claridad, lo que hace que incluso los temas complejos del mercado sean accesibles para un público amplio sin sacrificar el rigor.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet