The Clock is Ticking: How Young Workers Can Outsmart Social Security's 2034 Crisis with Smart Investment Moves

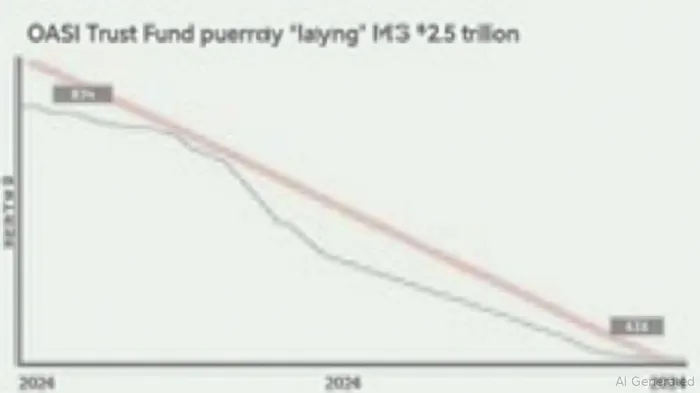

The Social Security Administration's 2025 report paints a stark picture: the Old-Age and Survivors Insurance (OASI) Trust Fund, which funds retirement benefits, will run dry by 2034, reducing scheduled benefits to 81% of current levels. For young workers today—those in their 20s and 30s—this means their retirement nest egg could shrink by nearly a fifth unless they take proactive steps. This isn't just a policy debate; it's a personal financial crisis demanding immediate action. Let's dissect the risks and craft a strategy to safeguard your future.

The Depletion Timeline: Why 2034 is a Hard Deadline

The OASI Trust Fund's reserves are projected to vanish by 2034, after which benefits will rely solely on payroll tax revenue. By 2099, this income will cover only 69% of promised benefits. The Disability Insurance (DI) Fund, while stable through 2099, offers little solace—its success hinges on a workforce that's shrinking due to low fertility and aging boomers.

Why Procrastination is Financial Suicide

Compound interest is a double-edged sword. Delaying retirement savings means missing out on decades of growth. For a 30-year-old earning $50,000 annually, contributing an extra $500/month to a 401(k) could add $1.2 million by age 67 (assuming a 7% annual return). Conversely, relying solely on Social Security's diminished payouts could slash their post-2034 retirement income by thousands yearly.

Action Plan A: Maximize 401(k) Contributions

2025's IRS limits offer a clear roadmap:

- Employee contributions: $23,500/year ($31,000 for those 50+).

- Employer matches: Don't leave free money on the table—contribute at least enough to capture your company's match.

- Tax advantages: Pre-tax contributions reduce taxable income now, while Roth 401(k)s offer tax-free withdrawals in retirement.

Why this matters: A 30-year-old who saves $20,000 annually in a 401(k) could accumulate $1.4 million by 2060, even with modest returns. Pair this with an employer match, and you're already ahead of the game.

Action Plan B: Roth IRAs for Tax Efficiency

Roth IRAs are a stealth weapon for young workers. With lower current income than their future selves, they benefit from paying taxes now on contributions rather than later on withdrawals.

2025's rules:

- Contribution limit: $7,000/year ($8,000 for those 50+).

- Income phase-outs: Single filers with MAGIMAGY-- below $150,000 can contribute fully.

The kicker: Earnings grow tax-free, and withdrawals in retirement are penalty-free. Even if Congress eventually raises taxes on retirement accounts, Roth holders are shielded.

Action Plan C: Diversify with Inflation Hedges

Social Security's post-2034 benefit cuts will hit hardest if inflation resurges. Protect your portfolio with assets that thrive in rising prices:

1. Treasury Inflation-Protected Securities (TIPS)

- How they work: Their principal adjusts with the Consumer Price Index (CPI), ensuring purchasing power.

- Risks: Avoid long-term TIPS (e.g., 30-year maturities) unless you're certain of holding them to maturity. Short-term TIPS (5–10 years) offer stability.

2. Real Estate: A Cash Flow Machine

- Direct ownership: Rent out apartments or duplexes—rents can be hiked annually, outpacing inflation.

- Securitized options: REITs (e.g., VNQ, which tracks the MSCI US REIT Index) offer liquidity and diversification.

Why now? U.S. housing shortages (projected to grow to 3 million homes by 2030) will drive demand for multifamily and senior housing. A 2023 study found real estate delivered 8–10% annualized returns over 10–15 years, even during crises.

Balancing Risk and Liquidity: A Pragmatic Approach

No strategy is perfect. Pair aggressive growth assets (stocks, real estate) with stable income streams (TIPS, dividend stocks). For example:

- 60% stocks (diversified via ETFs like VTI or SPY).

- 25% real estate (VNQ or direct property).

- 15% TIPS and short-term bonds (e.g., BIL for liquidity).

Avoid overexposure to real estate without a long-term horizon—illiquidity can bite during downturns.

The Bottom Line: Act Now or Pay Later

Social Security's 2034 crunch isn't a distant worry—it's a ticking clock. By boosting 401(k) contributions, leveraging Roth IRAs, and diversifying into inflation-resistant assets, young workers can build a portfolio that outpaces government cuts. The math is clear: $1 invested now yields $5 by 2060 at 7% returns. Don't let inertia turn this into a retirement crisis. The time to act is now.

Your future self will thank you.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet