Citigroup Tops Q1 Estimates with Strong Trading, Wealth Gains; Reaffirms 2025 Outlook

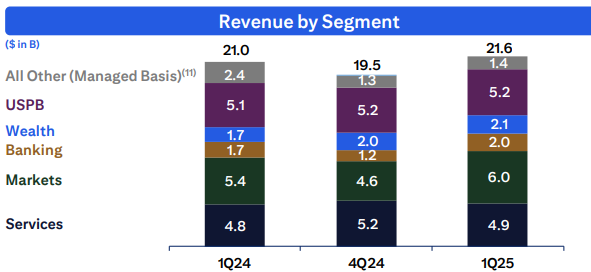

Citigroup kicked off 2025 with a strong first-quarter performance, beating analyst expectations and showcasing resilience across its core businesses. Net income rose to $4.1 billion, or $1.96 per share, up from $3.4 billion, or $1.58, a year ago, and well ahead of the $1.85 consensus. Revenue came in at $21.6 billion, a 3% increase year-over-year, boosted by higher net interest income and strength in its trading and investment banking units. CEO Jane Fraser emphasized momentum across all five business lines, particularly noting the best Q1 Services performance in a decade and surging Wealth revenue. She reiterated the bank’s commitment to its diversified strategy and long-term confidence in the U.S. economy and dollar.

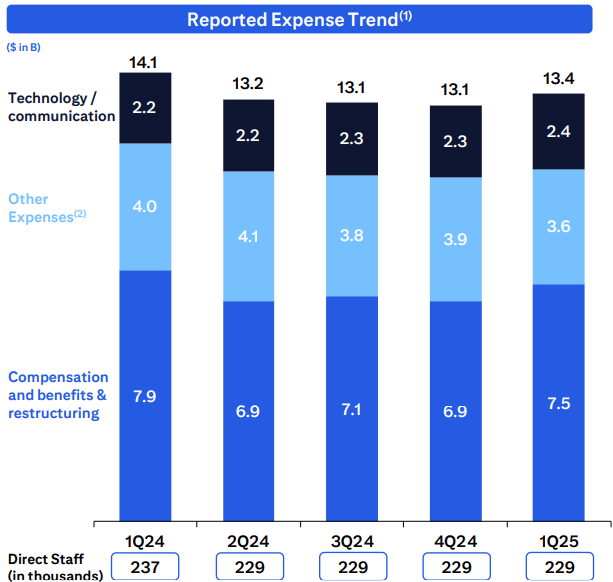

Net interest income rose 4% to $14.01 billion, above the $13.68 billion estimate, supported by strength in U.S. Personal Banking, Wealth, Services, and Markets. Operating expenses fell 5% to $13.43 billion, aided by a lighter FDIC charge, cost-cutting initiatives, and FX benefits. The bank delivered positive operating leverage and posted an 8% return on average equity and 9.1% return on tangible common equity, both ahead of expectations. CitiCTRN-- returned $2.8 billion to shareholders in the quarter, including $1.75 billion in buybacks as part of its $20 billion repurchase plan.

By segment, U.S. Personal Banking (USPB) revenue rose 2% to $5.23 billion, driven by Branded Cards. Wealth revenue surged 24% to $2.1 billion, with Citigold, Private Bank, and Wealth at Work all contributing to growth. Investment fee revenues were strong, and deposit spreads improved even as balances declined slightly due to a shift toward higher-yielding investments. The Private Bank saw a 16% revenue increase, and Wealth at Work posted 48% revenue growth.

Markets revenues increased 12% to $6.0 billion, with Fixed Income up 8% to $4.5 billion and Equities up 23% to $1.5 billion. Equities benefitted from strong performance in derivatives and rising client activity, while FICC was buoyed by spread products and robust trading in rates and currencies. Investment banking revenue rose 12% to $1.04 billion, topping expectations, with advisory fees up 84% year-over-year. M&A activity saw a strong rebound, while ECM and DCMDCOM-- saw moderate pullbacks.

Services revenue totaled $4.89 billion, slightly below the $5.01 billion consensus, but still marked the best first quarter in a decade. Deposits in Services were up, though softness in other segments slightly offset gains. Corporate Lending was modestly lower excluding hedges, but Banking revenue still climbed 12% to $1.95 billion. CEO Jane Fraser highlighted that the investment banking pipeline remains strong, with particular strength in advisory engagements.

Credit costs increased meaningfully, with total cost of credit rising 15% to $2.7 billion, driven by a higher allowance for credit losses (ACL) due to a more cautious macroeconomic outlook. Net charge-offs totaled $2.46 billion, in line with the seasonal uptick in card losses. The allowance for credit losses now stands at $22.8 billion, including $18.7 billion on loans, down slightly as a percentage of funded loans to 2.70%. Nonperforming loans were down 2% to $2.7 billion, with corporate NPLs down 8%, and consumer NPLs up 4%.

Citi's balance sheet remained solid, with loans up 4% year-over-year to $702.1 billion and deposits increasing 1% to $1.32 trillion. The CET1 ratio was 13.4%, slightly below the prior quarter's 13.6%, due to share repurchases, dividend payments, and higher risk-weighted assets. Book value per share rose 5% to $103.90, and tangible book value climbed 6% to $91.52.

Looking ahead, Citigroup maintained its 2025 guidance. It expects full-year revenue of $83.1 to $84.1 billion, with net interest income (ex-Markets) up 2-3% and expenses slightly below $53.4 billion. The firm anticipates card net credit losses near the top of 2024 levels, particularly in the first half, and continues to adjust reserves based on macro conditions. Another $1.75 billion in share repurchases is targeted for Q2.

From a technical standpoint, CitigroupC-- shares remain rangebound, and while the recent results may provide a catalyst, sustained breakout likely hinges on improved macro clarity. With its diversified business mix, growing advisory pipeline, and a strong capital return strategy, Citi remains well-positioned despite ongoing economic headwinds.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet