Citigroup Rips Higher After Q4 Earnings: The One Big Surprise That Broke the “Sell-the-News” Curse

Citigroup walked into Q4 earnings season with the same problem as its peers: bank stocks had already enjoyed a monster 2025 run, expectations were high, and the market was itching to “sell the news” on anything less than perfection. JPMorgan, Bank of America, and Wells Fargo all found out the hard way that a good quarter isn’t always good enough when positioning is crowded and investors want clean upside guidance. Citi, however, managed to buck that trend. Shares were up about 1%–1.5% premarket after the report, reflecting a rare earnings-season outcome for a large-cap bank right now: Citi delivered a beat that felt meaningfully better than expected, paired with a forward narrative investors actually wanted to buy.

The biggest driver was simple: CitiC-- beat on the numbers that matter most to the tape — revenue and adjusted earnings — while keeping the expense story from getting out of hand relative to what investors feared. CitigroupC-- reported adjusted EPS of $1.81 versus consensus of $1.67, a solid upside surprise. Adjusted revenue came in at $21.0 billion versus expectations of $20.93 billion, which doesn’t sound dramatic, but in this market the direction matters: it was a top-line beat, not a miss. On a reported basis, Citi posted net income of $2.5 billion, or $1.19 per share, on revenue of $19.9 billion, versus $2.9 billion / $1.34 per share on $19.5 billion revenue a year ago. The quarter included a $1.2 billion loss tied to the held-for-sale accounting treatment around Citi’s plan to sell its Russia consumer business, which pressured reported profitability and distorted comparisons. Excluding that Russia-related item, Citi’s net income was $3.6 billion and EPS was $1.81 — the number investors were trading off.

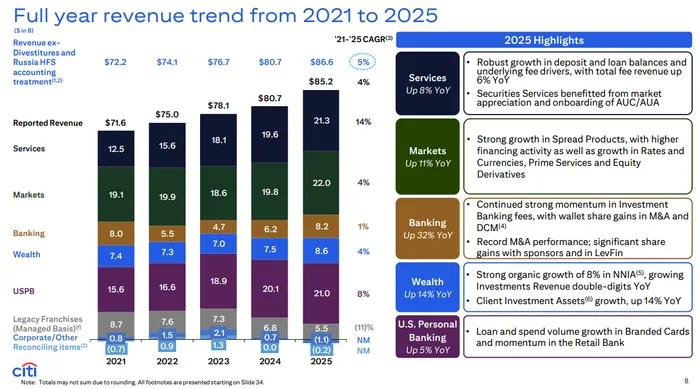

The revenue mix was also strong in a way that reinforced Citi’s core restructuring narrative: the growth was coming from the institutional and fee-heavy parts of the franchise rather than a one-time pop. Reported revenues rose 2% year over year, but excluding the Russia-related item, revenue was up 8%, driven by growth in Banking, Services, U.S. Personal Banking (USPB), and Wealth. Citi’s reported net interest income increased 14% year over year, supported by contributions from Markets, Services, USPB, Wealth, and legacy franchises, while non-interest revenue fell sharply year over year on a reported basis (down 27%), largely due to declines in several areas and the noise from legacy items. The more important takeaway for investors is that Citi’s engine is becoming more NII-driven again, and management believes it can grow NII even with declining short-end rates.

Loan growth was another bright spot, and this is a key reason Citi’s stock reaction differed from peers. End-of-period loans rose 8% year over year to $752 billion, while average loans increased 7% to $737 billion, with growth driven by Markets, USPB, and Services. Deposits were also strong: end-of-period deposits increased 9% year over year to roughly $1.4 trillion, driven primarily by Services, and average deposits rose 8%. That matters because Services is Citi’s crown jewel — sticky operating deposits, payments flows, and client mandates that tend to produce durable revenue and higher-quality growth. In other words, Citi didn’t just “beat estimates,” it showed tangible momentum in the parts of the balance sheet investors actually trust.

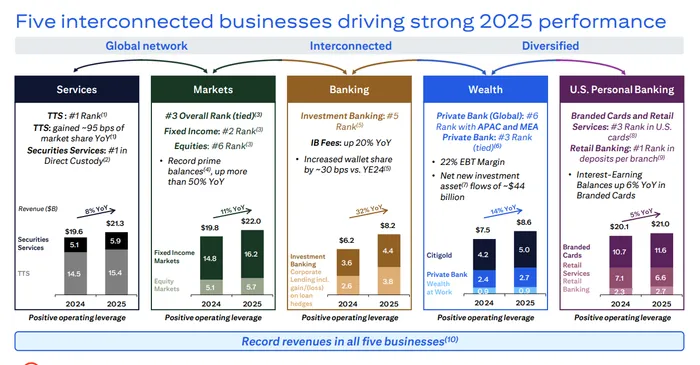

Within segments, Services continued to lead and helped anchor the bull case. Services revenue grew 15% to $5.9 billion, with Treasury and Trade Solutions (TTS) revenue up 6% and Securities Services revenue up an eye-catching 43%. The Securities Services strength was helped by Russia-related items and higher fees, with assets under custody and administration up 24%, but even stripping out that noise, the broader message is that Citi is winning mandates and seeing deeper engagement from clients. Net interest income in Services was up 18%, powered by higher average deposit balances and better deposit spreads — exactly the kind of mix-driven growth management wants to highlight as it reshapes the firm.

Markets was solid, if not spectacular, but importantly it was better than feared and delivered a trading beat that helped sentiment. Citi posted FICC sales and trading revenue of $3.46 billion, above expectations of $3.29 billion. Total Markets revenue was $4.5 billion, down 1% year over year, reflecting tough comparisons versus a strong prior-year quarter, but the desk held up despite that. Equity markets revenue was slightly lower year over year, but prime services momentum remained strong with record prime balances up more than 50%, alongside better derivatives performance. The nuance here is key: Citi didn’t need Markets to explode higher — it just needed the division to remain a reliable contributor while the broader institutional rebuild continues.

Banking was the standout upside surprise on a growth rate basis, and it helped explain why Citi’s print felt “different” from BAC and WFC. Banking revenue surged 78% to $2.2 billion, driven by Corporate Lending and Investment Banking. Investment Banking revenue rose 38% with investment banking fees up 35% to about $1.29 billion, helped by a massive 84% jump in advisory fees and a 19% increase in debt capital markets fees. Equity capital markets was down 16% due to lower follow-on volumes, but overall the banking complex showed clear momentum and share gains — and that’s exactly what investors have been waiting to see from Citi for years. When the deal environment is decent and a bank is showing real improvement in advisory/DCM, the market tends to reward it quickly.

Wealth also improved, with revenue up 7% to $2.1 billion. Net interest income increased 12% on higher deposit spreads and balances, though non-interest revenue was slightly down due to the sale of a trust business earlier in 2025. Citigold and Private Bank were the bright spots, while “Wealth at Work” was softer due to mortgage spread pressure. The bigger picture is that Citi is still building a more complete wealth offering, and this segment — while smaller than peers — is contributing to the firm-wide “more balanced earnings mix” narrative.

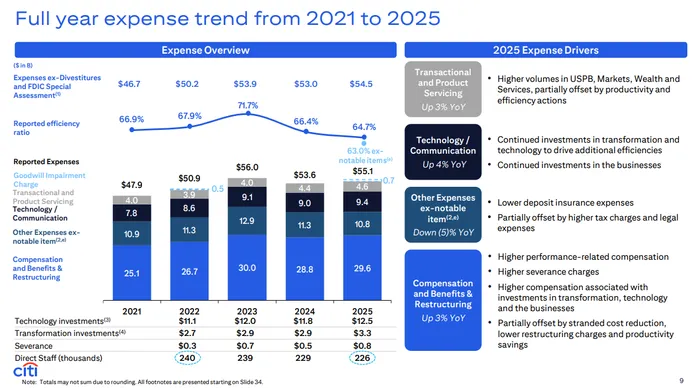

Expenses were higher, but investors didn’t punish Citi for it the same way they punished others, largely because the revenue and operating leverage delivery was strong enough to absorb the spend. Citi’s operating expenses rose 6% to $13.8 billion, driven by higher comp and benefits, legal expenses, technology and communication spend, and non-income tax charges, partially offset by productivity savings and lower deposit insurance costs. Those aren’t trivial increases, but Citi framed 2025 as a year of investment paying off, and CEO Jane Fraser emphasized positive operating leverage across all five businesses. Investors appear willing to accept some expense pressure if Citi can show that the spend is tied to sustainable revenue growth and improved returns — and this quarter supported that view.

Margins and profitability remain a work in progress, but the direction is improving. Citi posted a RoTCE of 5.1% in the quarter, or 7.7% excluding the Russia-related item, and for the full year the bank generated a RoTCE of 7.7% (8.8% excluding notable items). That’s not yet “peer-level,” but management is explicitly targeting 10–11% RoTCE for 2026, and the market is increasingly trading Citi as a multi-year improvement story rather than a one-quarter headline. Capital supports that patience: Citi ended the quarter with a CET1 ratio of 13.2%, well above regulatory requirements, and returned over $17 billion to shareholders in 2025, including $13 billion of buybacks.

Credit quality was the one area that remained mixed, but not in a way that derailed the report. Provision for credit losses was $2.2 billion, driven primarily by U.S. card net credit losses, but importantly that provision was lower than the prior-year quarter’s $2.6 billion, and net credit losses were down 2% year over year. Citi’s total allowance for credit losses was about $21.4 billion, with a reserve-to-funded loans ratio of 2.6%, slightly lower year over year. One watch item: total non-accrual loans increased materially to $3.6 billion, including a jump in corporate non-accruals tied to idiosyncratic downgrades, and consumer non-accruals that were impacted in part by residential mortgage loans tied to the California wildfires. That’s not nothing, but the market’s focus today was more on the earnings power and operating momentum than on a broad-based credit deterioration signal.

The outlook is ultimately what helped Citi break the “sell the news” curse. Management guided to NII ex-Markets growth of 5–6% year over year in 2026, driven by loan growth in Cards and Wealth, deposit growth in Services and Wealth, and continued benefit from reinvesting the investment portfolio into higher-yielding instruments. Citi also reiterated its targets for roughly a 60% efficiency ratio, another year of positive operating leverage, and achieving a 10–11% RoTCE in 2026. That’s a clear, measurable scorecard — and in a market that’s punishing ambiguity, clarity sells.

Bottom line: Citi’s Q4 report jumped out because it didn’t just beat estimates — it reinforced a credible “momentum + restructuring execution” story with broad revenue strength, visible loan and deposit growth, a trading upside surprise in FICC, and a confident outlook for NII growth and returns in 2026. While expenses were higher and credit remains something to monitor (especially U.S. cards), investors appear willing to pay for progress when the top line is accelerating and management is delivering positive operating leverage. In a season defined by “good isn’t good enough,” Citi managed to be better than good — and the market rewarded it accordingly.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet