Cisco Just Quietly Turned Into an AI Powerhouse — And the Stock Is Exploding

Cisco Systems just reminded the market that “boring old networking” is suddenly one of the more exciting places in tech. The company kicked off fiscal 2026 with an 8% revenue increase to $14.9 billion, a 10% non-GAAP EPS gain to $1.00, and guidance that points to its “strongest year yet,” in CEO Chuck Robbins’ words. The stock is responding in kind, up about 7% in pre-market trading and pushing to its best level in roughly 25 years, as investors lean into a story built on AI infrastructure demand, a multi-year campus refresh cycle, and still-reasonable valuation versus the rest of AI-adjacent tech.

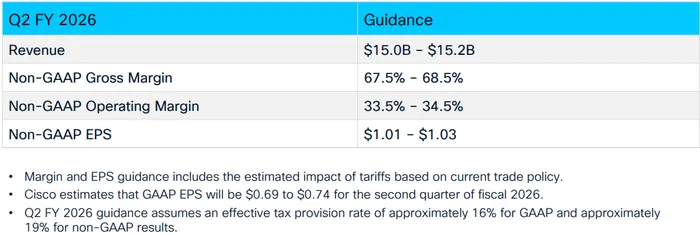

Against expectations, this was a clean beat-and-raise quarter. Revenue of $14.9 billion came in modestly ahead of the $14.76 billion consensus, while adjusted EPS of $1.00 topped the $0.98 estimate. The company also raised both Q2 and full-year guidance: Q2 revenue is now expected at $15.0–$15.2 billion versus the Street’s $14.63 billion, with non-GAAP EPS of $1.01–$1.03 versus $0.99. For FY26, CiscoCSCO-- guided revenue to $60.2–$61.0 billion (roughly 7% growth year over year) compared with consensus near $59.7 billion, and non-GAAP EPS to $4.08–$4.14 versus expectations around $4.04. For a company that has already beaten estimates for more than a dozen quarters in a row, the pattern of under-promising and over-delivering remains well intact.

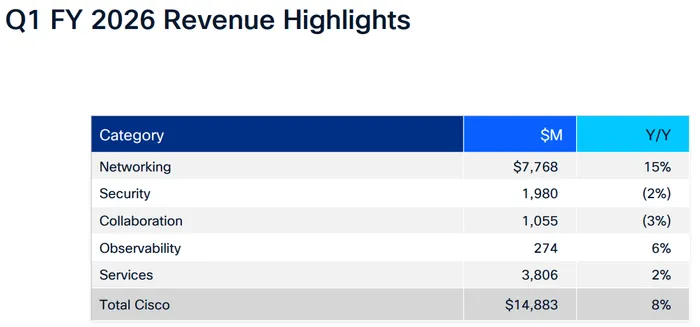

Under the hood, the quarter looked exactly like a networking- and AI-driven story. Product revenue grew 10% to $11.1 billion, outpacing services at 2% growth. Within that, Networking revenue rose 15%, continuing a strong run as customers upgrade infrastructure for AI workloads and modern campus environments. Observability grew 6%, while Security declined 2% and Collaboration fell 3%, underscoring that this is not a broad-based Cisco renaissance so much as a powerful cycle in the core networking franchise. Geographically, the Americas led with 9% growth, while EMEA and APJC each grew around 5%, reflecting where data center building and AI investment are most intense.

The most important datapoint for the market was the AI order and revenue trajectory. Cisco booked $1.3 billion of AI infrastructure orders from hyperscalers in the quarter, split roughly 50/50 between systems and optics, plus more than $200 million from neocloud, sovereign, and enterprise customers. Management now expects to recognize approximately $3 billion of AI infrastructure revenue from hyperscalers in FY26, up from about $1 billion in FY25, with AI-related orders guided to double to $4 billion. On top of that, Robbins highlighted a pipeline in excess of $2 billion for high-performance networking products across sovereign, neocloud, and enterprise customers for the rest of the year. Analysts keyed in on this during Q&A, with multiple questions probing the durability of webscale demand and the pace at which enterprise AI networking follows the hyperscalers’ lead.

The other structural driver is the campus networking refresh. Cisco is staring at roughly $10 billion of older campus products reaching end-of-service in FY26, which is helping drive what management calls a multi-year, multi-billion-dollar upgrade cycle. In Q1, all major campus technologies—switching, routing, wireless, and IoT—saw accelerated order growth, while new product families like next-gen smart switches, secure routers, and Wi-Fi 7 solutions are ramping faster than prior launches. This is exactly the kind of high-visibility, infrastructure-heavy cycle the Street tends to reward, particularly when paired with AI-driven spend in data centers.

Margins and profitability round out the quality of the print. Non-GAAP gross margin came in at 68.1%, with product gross margin at 67.2% and services at 70.7%. While gross margin is slightly below year-ago levels, Cisco more than offset that via operating leverage: non-GAAP operating margin was a robust 34.4%, with operating expenses up just 3% on 8% revenue growth. GAAP operating income jumped 43%, with the GAAP operating margin at 22.6%. Non-GAAP net income grew 9%, and EPS rose 10%, helped modestly by share repurchases. Operating cash flow of $3.2 billion dipped 12% year on year but remained solid, and Cisco returned $3.6 billion to shareholders via dividends and buybacks, maintaining its profile as a cash-return machine rather than a speculative AI bet.

On the outlook, management’s tone was notably confident. Robbins said Cisco is “on track to deliver our strongest year yet,” citing AI infrastructure and campus networking as the key pillars. CFO Mark Patterson emphasized that the company raised revenue and EPS guidance while absorbing cost pressures, including higher memory prices and existing tariff assumptions; the only change in their macro framework was a reduction in the China fentanyl-related tariff from 20% to 10%. The FY26 guide implies high-single-digit revenue growth and similar or slightly higher EPS growth, with additional upside possible if Cisco’s historical pattern of conservative guidance holds.

Security remains the main blemish—and the Street isn’t ignoring it, but it’s not enough to derail the thesis. Security revenue fell 2% year over year despite platform launches and firewall refreshes, in part due to mix shifts including Splunk’s move toward cloud subscriptions. Management framed this as a timing issue and a transition rather than demand destruction, but several analysts pressed for clarity on when growth returns and how quickly next-gen offerings can offset declines in legacy platforms. For now, investors are giving Cisco the benefit of the doubt because the networking and AI cycles are more than compensating.

Analyst reaction to the print and guide was broadly constructive to outright bullish. KeyBanc raised its price target to $87 from $77 and reiterated Overweight, arguing that weakness in Security is “far outweighed” by strength in Networking, with 13% order growth and high-teens networking order growth underpinning a multi-year cycle. Bank of America took its target to $95 from $85 and reiterated Buy, highlighting very strong AI networking orders, the $3 billion FY26 AI revenue goal, and upgraded 2026 revenue growth guidance to 7% versus the Street’s 5.3%. BofA also noted that Cisco still trades at roughly a 17x forward EV/FCF multiple—hardly nosebleed territory for an AI-levered name. Barclays was more restrained, maintaining Equal Weight and a $76 target, acknowledging the strong AI orders and lifted revenue guide while flagging ongoing Security weakness and noting that non-AI growth is closer to 4%. Citi stayed in the bull camp, keeping its Buy rating, bumping its target to $85, and raising FY26/27 EPS estimates by 3–5%, calling this a classic “beat and raise” quarter that confirms a durable networking upgrade cycle driven by agentic AI inference demand.

Put it together, and this is exactly the kind of AI story the market wants right now: tangible orders, infrastructure-heavy, tied to real capex cycles rather than just promises—and still trading at something resembling a normal multiple. Security is a work in progress and execution risk around supply, tariffs, and competitive dynamics remains, but for now, the Street’s message is clear: the networking cycle has legs, and Cisco is finally getting paid for it.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet