Cingulate's PDUFA Fee Waiver and CTx-1301: A Strategic Catalyst for Value Creation in ADHD Therapeutics

The biotech sector is no stranger to high-stakes gambles, but Cingulate Inc.CING-- (NASDAQ: CING) has just handed its shareholders a rare hand of cards—and it's a strong one. The company's recent $4.3 million PDUFA fee waiver from the FDA isn't just a financial relief; it's a masterstroke that could redefine its path to commercialization. Let's unpack how this waiver, combined with the clinical and commercial potential of CTx-1301, positions CingulateCING-- as a compelling long-term investment in a fast-growing, underserved market.

The PDUFA Waiver: A Financial Lifeline for a Small-Cap Biotech

The FDA's Prescription Drug User Fee Act (PDUFA) typically imposes a $4.3 million fee for new drug applications (NDAs). For a company like Cingulate, which operates with a market cap of ~$22 million and limited cash reserves, this would have been a crippling burden. But here's the kicker: Cingulate qualified for a full waiver under the small business provisions of the FD&C Act. This exemption isn't just a checkmark on a regulatory to-do list—it's a strategic lever.

By avoiding the upfront PDUFA fee, Cingulate preserves ~19% of its total market cap in liquidity. That's not chump change. It allows the company to allocate capital toward Phase 3 trial completion, manufacturing readiness, and, critically, early commercialization partnerships. The waiver also reduces the risk of dilution, which is a death knell for many small biotechs. For investors, this means Cingulate can hit its NDA submission deadline (mid-2025) without burning through cash or issuing shares.

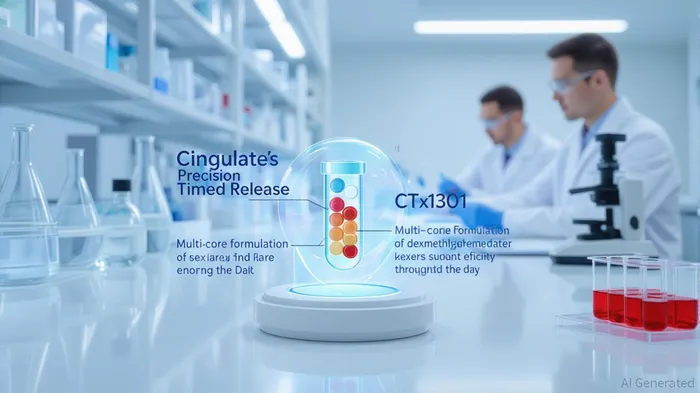

CTx-1301: A Differentiated ADHD Treatment with Real-World Utility

ADHD therapeutics are a $14.3 billion market in 2023, growing at 3.7% CAGR. Stimulants dominate 70% of this space, but they come with a litany of issues: short half-lives requiring multiple doses, crash/rebound effects, and abuse potential. Enter CTx-1301, a once-daily, trimodal extended-release formulation of dexmethylphenidate.

Cingulate's proprietary PTR™ platform is the secret sauce. By engineering three distinct drug releases at predefined times, CTx-1301 addresses the critical unmet need of sustained efficacy throughout the active day. In Phase 3 trials, the drug showed robust effect sizes (0.737–1.185) across all doses, outperforming the mean effect size of long-acting stimulants (0.73). What's more, it demonstrated no serious adverse events in nine clinical trials and can be taken with or without food—a convenience factor that could drive adoption.

The ADHD market is ripe for disruption. Over 60% of patients currently use immediate-release booster doses to maintain symptom control. CTx-1301 could eliminate this need, capturing a significant share of the 11 million adult and 6.4 million pediatric ADHD patients in the U.S. alone.

Regulatory and Commercial Tailwinds

Cingulate's regulatory pathway is unusually clear. The FDA confirmed in April 2025 that Phase 3 data is sufficient for NDA submission, with a commercial launch slated if approved. The Pre-NDA meeting feedback aligned with Cingulate's plans, including acceptance of stability data and the use of Focalin XR's efficacy data. This de-risks the approval timeline and reduces the need for costly post-approval studies.

On the commercial front, the company is already engaging with payers and partners. CTx-1301's novel mechanism and convenience make it a strong candidate for outlicensing in the U.S. and globally—a strategy that could fast-track market access while minimizing Cingulate's operational risk. The drug's potential to outperform existing stimulants (e.g., Vyvanse, Adderall) and non-stimulants (e.g., Qelbree) further strengthens its value proposition.

The Bigger Picture: A Platform Play Beyond ADHD

CTx-1301 isn't just a product—it's a proof of concept for Cingulate's PTR™ platform. The company is already leveraging this technology to develop CTx-2103, a once-daily buspirone formulation for anxiety, backed by a $3 million non-dilutive grant. This diversification reduces reliance on a single asset and opens the door to other therapeutic areas where sustained drug release is critical.

Investment Thesis: A Low-Risk, High-Reward Opportunity

Cingulate's story is a textbook example of how regulatory and financial strategy can amplify a small biotech's potential. The PDUFA waiver removes a major near-term obstacle, while CTx-1301's clinical differentiation and market alignment create a clear path to revenue. With a cash runway extending into Q4 2025 and an NDA submission in mid-2025, the company is poised to deliver a catalyst-driven return.

For investors, the key risks are typical: regulatory delays, post-approval reimbursement hurdles, and competition. But the upside is substantial. If CTx-1301 secures approval and captures even 5% of the ADHD market, Cingulate could see a 10x valuation multiple. This isn't just a bet on a drug—it's a bet on a company that's mastered the art of value creation in a capital-efficient way.

Final Takeaway: Cingulate's PDUFA waiver is a financial windfall, but it's CTx-1301 that's the real game-changer. In a $18.6 billion ADHD market with growing demand for safer, more convenient treatments, this biotech is sitting on a goldmine. For those with a stomach for biotech risk, now is the time to watch—and act.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet