Ciena Surges 73% in 3 Months: Should Investors Still Buy the Stock?

Ciena Corporation CIEN stock has surged 72.7% in the past three months, outperforming the Zacks Communication - Components industry’s growth of 53.3%. The S&P 500 composite and Zacks Computer & Technology sector have declined 1.8% and 2.8%%, respectively, over the same time frame.

CIEN has also outpaced its peers, Cisco Systems, Inc. CSCO, Nokia NOK and Arista Networks, Inc. ANET. CSCOCSCO--, NOKNOK-- and ANETANET-- have climbed 3.1%, 36% and 8.6%, respectively, in the past three months.

Image Source: Zacks Investment Research

Ciena shares have climbed 17.1% in the past month, supported by robust first-quarter fiscal 2026 results, wherein both top and bottom lines beat Zacks Consensus Estimate and grew year over year. Ciena’s fiscal first-quarter reflected a year-over-year 33% top-line gain, 111% EPS growth and a record $7 million order backlog, driven by accelerating AI-led demand from cloud and service provider customers. It continues to capitalize on WAN connectivity needs across subsea, long-haul, metro networks and DCI. CIENCIEN-- is currently trading at $363.88 and has a 52-week high of $567.45.

Following a strong rally, investors may wonder whether CIEN still has upside or if expectations have outpaced fundamentals. Let’s break down to see what’s driving the rally, the bull and bear cases, and a practical approach to managing risk and position size.

CIEN’s Tailwinds

Ciena’s growth is being driven by exceptionally strong and sustained demand, supported by robust order activity and long-term customer planning. In the last earnings call, the company highlighted that this demand visibility, combined with strong execution, provides confidence in continued growth through 2026, 2027 and beyond. The increasing need for high-speed connectivity solutions, particularly to support scaling AI workloads, positions the company to benefit from durable, multi-year demand trends.

A key growth driver is the rising investment in AI-driven connectivity. Customers are significantly increasing spending to support AI training and inference workloads, and CienaCIEN-- is gaining share in this expanding market due to its technology leadership and strong customer relationships. Large-scale AI data center deployments require high-performance optical interconnects, and this is creating substantial opportunities for the company across both wide area networks and data center environments.

The company is also benefiting from structural demand in its core WAN business, fueled by continued cloud adoption and the need to interconnect geographically distributed data centers. Additionally, service providers are increasing investments in optical transport infrastructure and automation capabilities to handle surging data traffic and improve efficiency. The growing adoption of managed optical fiber networks, particularly in regions like India, is further contributing to demand and is expected to remain an important growth contributor.

Another significant growth factor is the expansion of opportunities in and around data centers. Hyperscalers are ramping capital expenditures to build AI infrastructure at scale, creating demand for solutions that enable scale across, scale out and scale up architectures. As compute workloads are distributed across multiple locations due to power and space constraints, the need for high-speed optical connectivity between sites is increasing, opening new avenues for Ciena’s interconnect solutions.

Moreover, innovation and product development are supporting growth by addressing evolving network requirements. New solutions such as advanced optical engines, pluggable optics and data center management platforms are designed to meet rising bandwidth, power and efficiency demands.

Image Source: Zacks Investment Research

Combined with increasing adoption of optical technologies within data centers and ongoing collaboration with hyperscalers and service providers, these innovations are expected to drive continued momentum and long-term expansion. Ciena expects revenues between $5.9 billion and $6.3 billion for fiscal 2026. It projects adjusted gross margins of 43.5-44.5%. For the second quarter of fiscal 2026, Ciena expects revenues of $1.5 billion (+/-$50 million). Adjusted gross margin is projected in the range of 43.5-44.5%.

However, CIEN is grappling with multiple headwinds that could weigh on its near-term performance, including potential disruptions from new tariffs and retaliatory trade actions, which may increase input costs, strain supply chains and dampen global demand, thereby pressuring margins and slowing international expansion. The company is also facing elevated expense levels driven by ongoing strategic investments in business expansion and technology enhancements, with fiscal first-quarter adjusted operating expenses rising 10.3% year over year to $383.2 million, primarily due to higher incentive payouts linked to strong orders and financial performance. Near-term challenges such as new product introduction ramp issues, rising input costs and supply constraints amid strong demand are adding pressure. Moreover, high customer concentration remains a concern.

CIEN’s Valuation

CIEN trades at a forward 12-month price-to-earnings (P/E) of 65.59X, above the industry’s 43.34X. CSCO, NOK and ANET trade at a forward 12-month P/E ratio of 21.99X, 22.75X and 41.31X, respectively.

Image Source: Zacks Investment Research

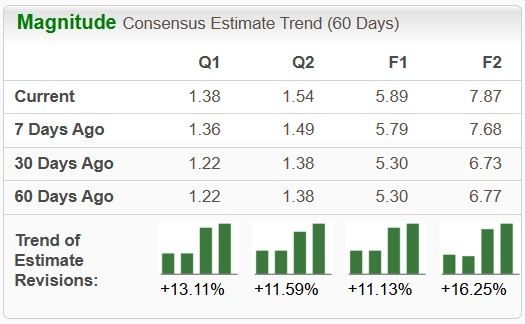

CIEN’s Upward Estimates

The Zacks Consensus Estimate for CIEN’s earnings for fiscal 2026 has been revised upward over the past 30 days.

Image Source: Zacks Investment Research

What Should You Do With CIEN Stock Now?

Ciena continues to benefit from increased network traffic, demand for bandwidth and the adoption of cloud architecture.

Sporting a Zacks Rank #1 (Strong Buy) at present and a Growth Score of B, CIEN seems to be a good bet now. Existing investors may consider holding their positions, while new investors could view the stock as an attractive buying opportunity. You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Nokia Corporation (NOK): Free Stock Analysis Report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Ciena Corporation (CIEN): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet