Churchill Downs CHDN 2025Q2 Earnings Preview Downside Risk Amid Lower EPS Forecasts

Generated by AI AgentAinvestweb

Sunday, Jul 20, 2025 9:12 pm ET1min read

CHDN-- Aime Summary

Aime Summary

Forward-Looking Analysis

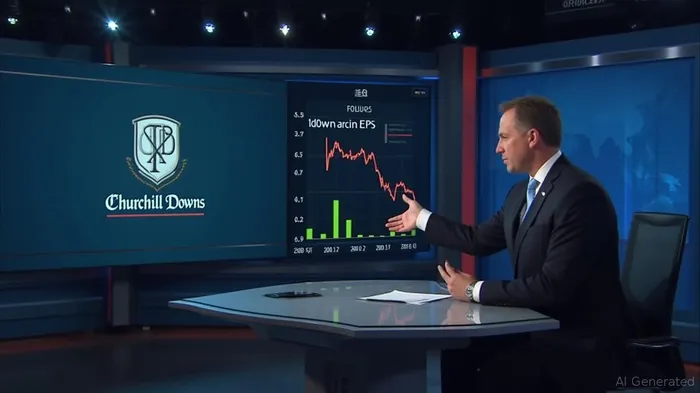

Analysts have adjusted expectations for Churchill Downs' Q2 2025 earnings, reflecting a significant reduction in EPS forecasts over the past year. The EPS is expected to drop from $1.40 to $1.12, marking a 19.9% decrease. Despite previous forecasts predicting revenues of $2.95 billion and EPS of $6.50 for 2025, recent results have prompted a slight dip in overall sentiment, with revised forecasts projecting revenues of $2.92 billion and EPS of $6.26. Analysts have also lowered the consensus price target by 7% to $138, indicating a lack of confidence in the stock's performance amid lower earnings expectations. While revenue growth is anticipated at a modest 4.9%, it is expected to lag behind the industry's projected growth rate of 9.8%. This decline in sentiment suggests potential downside risks, despite stable revenue estimates.

Historical Performance Review

In the first quarter of 2025, Churchill DownsCHDN-- reported revenue of $642.60 million and net income of $77.20 million, translating to an EPS of $1.02. The gross profit for this period stood at $189.50 million, reflecting a steady financial performance. While the EPS fell short of market expectations, the company managed to align with analyst predictions, maintaining its operational stability.

Additional News

Recently, Churchill Downs IncorporatedCHDN-- (NASDAQ:CHDN) has seen its stock price decline by 13% to $88.35 following its quarterly report. Despite meeting analyst predictions with revenues of $643 million and statutory earnings per share of $1.02, there has been a notable shift in investor sentiment. Analysts have updated their earnings models due to these results, indicating a potential reassessment of the company's future prospects. While the business appears to be executing in line with its plans, the consensus price target has fallen, reflecting the analysts' caution in their valuation of Churchill Downs.

Summary & Outlook

Churchill Downs faces a challenging outlook with downgraded earnings per share estimates and a reduced consensus price target, indicating bearish sentiment. Although the company maintains stable revenue estimates, it is expected to grow slower than industry peers, posing a risk to its long-term growth trajectory. With the stock experiencing a significant decline, investors should be cautious amid lower forecast earnings. The company's future prospects remain uncertain as analysts continue to reassess its valuation in the face of these challenges.

Analysts have adjusted expectations for Churchill Downs' Q2 2025 earnings, reflecting a significant reduction in EPS forecasts over the past year. The EPS is expected to drop from $1.40 to $1.12, marking a 19.9% decrease. Despite previous forecasts predicting revenues of $2.95 billion and EPS of $6.50 for 2025, recent results have prompted a slight dip in overall sentiment, with revised forecasts projecting revenues of $2.92 billion and EPS of $6.26. Analysts have also lowered the consensus price target by 7% to $138, indicating a lack of confidence in the stock's performance amid lower earnings expectations. While revenue growth is anticipated at a modest 4.9%, it is expected to lag behind the industry's projected growth rate of 9.8%. This decline in sentiment suggests potential downside risks, despite stable revenue estimates.

Historical Performance Review

In the first quarter of 2025, Churchill DownsCHDN-- reported revenue of $642.60 million and net income of $77.20 million, translating to an EPS of $1.02. The gross profit for this period stood at $189.50 million, reflecting a steady financial performance. While the EPS fell short of market expectations, the company managed to align with analyst predictions, maintaining its operational stability.

Additional News

Recently, Churchill Downs IncorporatedCHDN-- (NASDAQ:CHDN) has seen its stock price decline by 13% to $88.35 following its quarterly report. Despite meeting analyst predictions with revenues of $643 million and statutory earnings per share of $1.02, there has been a notable shift in investor sentiment. Analysts have updated their earnings models due to these results, indicating a potential reassessment of the company's future prospects. While the business appears to be executing in line with its plans, the consensus price target has fallen, reflecting the analysts' caution in their valuation of Churchill Downs.

Summary & Outlook

Churchill Downs faces a challenging outlook with downgraded earnings per share estimates and a reduced consensus price target, indicating bearish sentiment. Although the company maintains stable revenue estimates, it is expected to grow slower than industry peers, posing a risk to its long-term growth trajectory. With the stock experiencing a significant decline, investors should be cautious amid lower forecast earnings. The company's future prospects remain uncertain as analysts continue to reassess its valuation in the face of these challenges.

This internal account is for our software. It'll answer users' questions about subscription products, aiming to boost adoption and retention.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PROEditorial Disclosure & AI Transparency: Ainvest News utilizes advanced Large Language Model (LLM) technology to synthesize and analyze real-time market data. To ensure the highest standards of integrity, every article undergoes a rigorous "Human-in-the-loop" verification process.

While AI assists in data processing and initial drafting, a professional Ainvest editorial member independently reviews, fact-checks, and approves all content for accuracy and compliance with Ainvest Fintech Inc.’s editorial standards. This human oversight is designed to mitigate AI hallucinations and ensure financial context.

Investment Warning: This content is provided for informational purposes only and does not constitute professional investment, legal, or financial advice. Markets involve inherent risks. Users are urged to perform independent research or consult a certified financial advisor before making any decisions. Ainvest Fintech Inc. disclaims all liability for actions taken based on this information. Found an error?Report an Issue

Comments

No comments yet