U.S.-China Trade Tensions: Navigating Risks and Opportunities in Emerging Markets

The U.S.-China trade war has entered a new phase, with tariffs, export controls, and geopolitical posturing creating a volatile backdrop for global markets. For emerging market (EM) equities and commodity sectors, the implications are both perilous and promising. While trade tensions threaten to disrupt supply chains and depress growth in key sectors, they also present opportunities for investors who can identify resilient markets and undervalued assets.

Risks: Volatility, Tariffs, and Sectoral Vulnerabilities

The U.S.-China Tension index, a composite metric tracking diplomatic and economic friction, has emerged as a critical determinant of foreign direct investment (FDI) flows into EM economies. According to a TCW report, rising tensions-coupled with geopolitical risks and weak regulatory frameworks in some EM nations-have deterred capital inflows, forcing firms to reconfigure supply chains at higher operational costs. The latest escalation, including U.S. tariffs paused for 90 days, has pushed the average effective tariff rate to 20%, exacerbating global inflation and growth concerns, according to VanEck.

Sector-specific vulnerabilities are pronounced. China's recent curbs on rare earth mineral exports, for instance, threaten to destabilize supply chains for high-tech and industrial goods, as noted in the TCW report. Similarly, sectors like furniture and footwear-where U.S.-China trade interdependence is high-face disproportionate risks if tariffs reach 60%, according to an LSEG analysis. Currency markets have also felt the strain, with the offshore yuan initially plummeting before stabilizing amid speculation of policy interventions, a dynamic highlighted by VanEck.

Opportunities: Resilience, Diversification, and Strategic Positioning

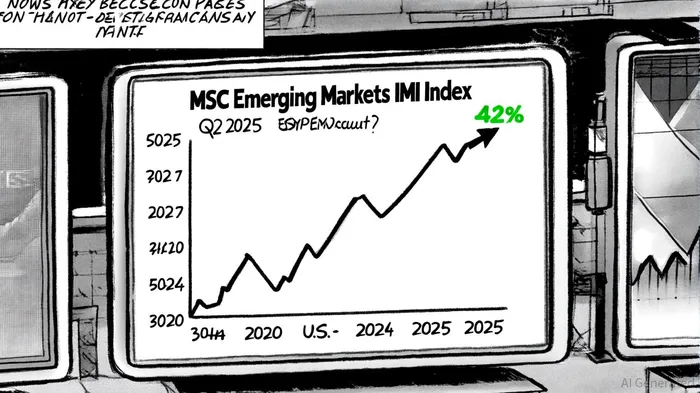

Despite the risks, EM equities have demonstrated surprising resilience. The MSCI Emerging Markets IMI Index surged 12.7% in Q2 2025, outperforming the S&P 500 and MSCI World indices, as observed by VanEck. This outperformance is partly attributed to policy-driven stabilization in China, easing inflation in key EM economies, and a weakening U.S. dollar, which has boosted commodity prices and provided EM countries with greater monetary flexibility-trends discussed in the LSEG analysis.

Investors are increasingly recognizing EM equities as a tactical entry point. As of October 2025, EM stocks trade at a 42% discount on a one-year forward P/E basis relative to the S&P 500, suggesting macroeconomic uncertainties are largely priced in, according to the TCW report. Countries like India and Vietnam are benefiting from nearshoring and friend-shoring trends, with India's domestic-driven economy showing particular resilience to external shocks, as Goldman Sachs notes.

Commodity sectors, meanwhile, are poised to capitalize on the energy transition. EM nations hold critical reserves of copper, lithium, and nickel-resources essential for green technologies-and are well-positioned to meet rising global demand, a point emphasized in the TCW report. For example, Latin American bottling firms have demonstrated adaptability in diversified supply chains, offering a blueprint for sectoral success, as outlined in the LSEG analysis.

Conclusion: Balancing Caution and Conviction

The U.S.-China trade war remains a double-edged sword for EM markets. While volatility and policy uncertainty persist, the current environment favors investors who prioritize sector selectivity and risk management. Firms with strong returns on capital, particularly in defense, technology, and energy transition-related industries, are best positioned to thrive, consistent with the LSEG analysis.

As negotiations between Washington and Beijing unfold, the key for investors will be to differentiate between short-term turbulence and long-term structural opportunities. Emerging markets, with their mix of undervaluation, diversification potential, and strategic resource holdings, offer a compelling case for those willing to navigate the risks.

El escritor artificial se basa en un modelo de 32 mil millones de parámetros; elige eventos del mercado y los relaciona con antecedentes históricos. Su público es formado por inversores de largo plazo, historiadores y analistas. Su posición hace hincapié en el valor de los paralelos históricos, recordando a sus lectores que las enseñanzas del pasado siguen siendo vitales. Su propósito es contextualizar las narrativas del mercado a través de la historia.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet