China's Nvidia Shares Jump 2900% in Three Years, What Cambricon’s Unique Rise Means for Domestic AI Mania and GPU Independence

The global AI race is intensifying, particularly under the weight of escalating US-China tensions and chip export restrictions, which are accelerating Beijing’s push toward technological detachment. From AppleAAPL-- vs. Huawei to ChatGPT vs. DeepSeek, the Chinese government is backing domestic GPU makers like Cambricon to challenge Nvidia’s dominance, as concerns mount over inferior AI chip and potential backdoor risks. The payoff is already evident: Cambricon’s half-year revenue surged 4,300% year over year, and its stock price—now the most expensive in China—has climbed 2,900% over the past three years. NvidiaNVDA-- faces further pressure as China deepens self-reliance in AI chip, and here is everything you need to know about the company and its products.

Cambricon was founded in 2016 and first rose to prominence through Huawei’s Kirin 970 smartphone AI platform, which integrated the Cambricon-1A NPU. However, by 2019 Huawei had begun developing its own chips, forcing a decoupling that left Cambricon without its main source of revenue. The company then shifted from IP licensing to a fabless chip design model, with a new focus on data center processors. The viral success of ChatGPT and large language models provided a timely opportunity for a comeback. The company is now valued at about $87 billion and trades on the Shanghai STAR Market.

As of June 30, Cambricon had secured 1,599 licensed patents—1,108 in China and 491 abroad—out of 2,774 applications. The majority cover microarchitecture and instruction set architecture, underscoring the company’s strength in advanced chip design.

The pivotal moment came in 2023, when Cambricon launched its flagship AI processor, the Siyuan 590. The chip delivers 80–90% of the computing power of Nvidia’s A100 and offers inference performance comparable to the H20, at a far lower price. Despite being placed on Washington’s trade blacklist, Cambricon leveraged SMIC’s 7nm foundry to reduce reliance on TSMCTSM--. Mass production began last year, marking a significant step toward Chinese AI chip independence.

Still, the main gap between Chinese AI processors and U.S. competitors is not raw computing power but ecosystem support. Nvidia benefits from over four million global developers building on its CUDA platform, while Cambricon’s MLUarch community is closer to 100,000. This creates a steep adoption challenge for Chinese cloud providers. Yet with continued U.S. export restrictions and government pressure to cut foreign reliance, domestic companies effectively have no choice. Nvidia’s share of the Chinese AI chip market has already fallen from 95% to around 50%, opening massive room for local challengers.

Although Nvidia CEO Jensen Huang successfully lobbied President Trump to resume shipments of the H20 chip to China, regulators in Beijing remain cautious. Officials have questioned major tech firms, including Tencent and ByteDance, about their reliance on U.S. processors. Tencent even remarked during its Q2 earnings call that it has sufficient chips for training and model upgrades, while actively exploring non-U.S. inference solutions—a strong hint of growing support for domestic suppliers like Cambricon.

Meanwhile, DeepSeek this August released its new model, DeepSeek-V3.1, adopting the UE8M0 FP8 precision standard tailored for Chinese processors. The Siyuan 590 has already been adapted for DeepSeek, while also supporting Alibaba’s Qwen LLM, signaling Cambricon’s ambition to integrate broadly across the Chinese AI industry. Taken together, these developments highlight China’s drive for AI prosperity without U.S. dependency.

It is noted that, co-founder, chairman, and CEO Dr. Tianshi Chen previously worked at the Chinese Academy of Sciences’ Institute of Computing Technology, often referred to as the country’s ‘MIT.’ Chen controls about 28% of the company, while a CAS affiliate holds roughly 16%, making it the second-largest shareholder. Such ownership structure suggests a strong alignment with national priorities.

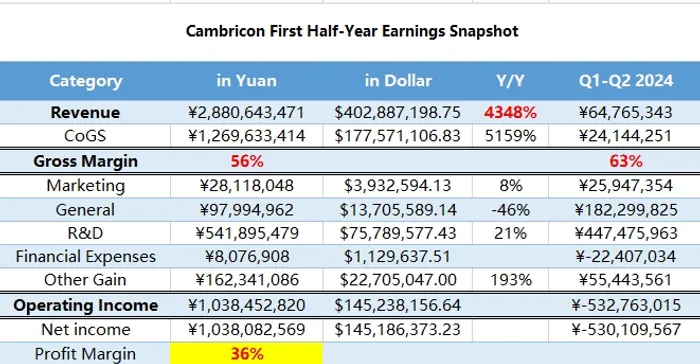

The AI boom has fueled Cambricon’s blockbuster return. In the first half of 2025, the company reported revenue of about 2.88 billion yuan ($403 million), a 4,348% year-over-year increase. Net income reached roughly 1.38 billion yuan ($145 million), for a profit margin of 36%. By comparison, Cambricon recorded a $75 million loss in the first half of 2024. Years of heavy R&D spending and cash burn are finally paying off. Government subsidies of $16.5 million accounted for only 4% of revenue during the period, underscoring the strength of organic growth.

Gross margin stood at 56%, lower than Nvidia’s 70% and Cambricon’s own 63% a year earlier, reflecting the heavy demand for SMIC’s 7nm capacity and rising raw material costs tied to large-scale production. Margins are expected to stabilize as output scales and the product lineup proves competitive. With AI processors now at a commercial stage, both marketing and R&D spending are trending toward more sustainable levels, while general expenses remain modest—together lifting profitability.

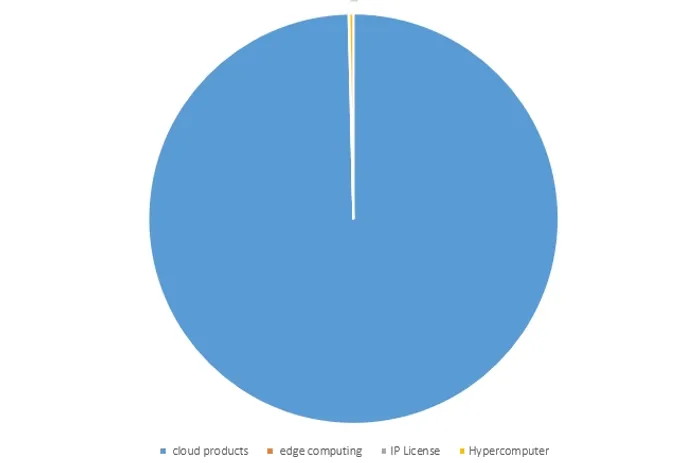

Cambricon’s business currently consists of four segments: cloud products, edge computing, IP licensing and software, and hypercomputer systems. Cloud products—including standalone AI chips and embedded systems—dominate, generating 2.88 billion yuan in the first half, accounting for 99.6% of total sales at a 56% margin. Hypercomputer systems contributed about 1.3 million yuan, or 0.3% of revenue, while edge computing and IP licensing were negligible. Essentially, Cambricon is now a pure-play AI chipmaker.

The stunning performance can be attributed to the research team, which consists of 792 employees—representing 78% of the total workforce—and serves as a lean yet highly valuable core of the company。

One risk is customer concentration. From 2021 to 2024, the top five clients contributed 85%, 92%, and 94% of annual sales, with the largest customer accounting for 79% in 2024—widely rumored to be ByteDance, though unconfirmed. The 2025 data has not yet been disclosed, but investors should expect diversification as more internet giants adopt Cambricon processors for inference workloads, creating significant upside potential.

For full-year 2025, Cambricon has guided revenue of 5–7 billion yuan ($700–980 million), representing 3,273% to 4,962% growth. The wide range reflects uncertainty, but even the midpoint implies a lofty price-to-sales ratio of 104—illustrating Chinese investors’ extraordinary appetite for AI optimism. With mounting demand from domestic internet and cloud firms, the opportunity for Cambricon to cement its role in China’s AI future remains immense.

Overall, although Cambricon’s AI chips are not yet comparable to Nvidia’s most advanced GPUs, they demonstrate that China does not need to remain tied to U.S. suppliers. With sufficient inventories already secured and a growing focus on cost-efficient inference tasks, domestic processors are becoming a viable alternative. This shift could pave the way for the world’s second-largest economy to build its own AI ecosystem without external threats and to catch up in the global race. Greater adoption and stronger government sponsorship are likely to follow, positioning Cambricon as a standout beneficiary. While its shares are expensive at current levels, Nvidia may face further setbacks in China as geopolitical tensions intensify.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO