Chile's Inflation Reversal and Central Bank Dilemma: Timing the Next Move in Emerging Market Debt and Copper

Chile's inflation narrative has taken a sharp turn in 2025, creating a complex puzzle for investors in emerging market debt and copper-linked assets. After a decade of relative stability, the country now faces a tug-of-war between cooling headline inflation and stubborn core inflation, all while the Central Bank of Chile (BCCh) grapples with the delicate balance of rate cuts and inflation control. For investors, the stakes are high: the timing of future monetary policy shifts could reshape risk-return profiles across asset classes, from sovereign bonds to commodities.

The Inflation Dilemma: Volatility vs. Persistence

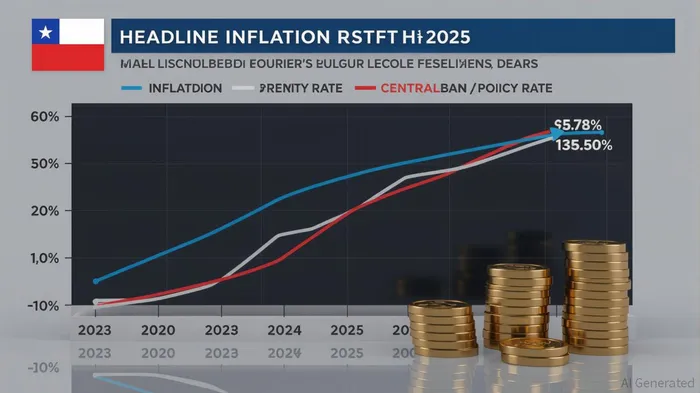

In June 2025, Chile's headline inflation dipped to 4.1%, driven by a -0.4% monthly drop in the Consumer Price Index (CPI), largely attributable to food and energy price corrections. This created the illusion of easing inflationary pressures. However, core inflation—excluding volatile components—remained at 3.8%, exceeding expectations and signaling entrenched cost-push dynamics. The July 2025 data further muddied the waters: a 0.9% monthly CPI surge, fueled by housing costs and food, pushed annual inflation to 4.3%, breaching the BCCh's 2%-4% target range.

This duality—transitory volatility in headline metrics versus persistent core inflation—has left the BCch in a precarious position. While the July 9 rate cut (25 bps to 4.75%) signaled a pivot toward easing, the subsequent inflation spike raises questions about the central bank's ability to engineer a “soft landing.” The key issue for investors is whether the BCch will prioritize short-term rate cuts to stimulate growth or maintain tighter policy to anchor inflation expectations.

Central Bank Strategy: A Flexible but Constrained Path

The BCch's July 2025 decision to cut rates reflected a recognition of weakening economic momentum, including a slowdown in private consumption and a moderation in wage growth. However, the central bank's minutes emphasized that future cuts would depend on “the evolution of the macroeconomic scenario and its implications for inflation convergence toward the target.” This flexibility is both a strength and a vulnerability.

The challenge lies in the lagged effects of monetary policy. A rate cut today may not translate into lower inflation for 12-18 months, yet the BCch's 2025 inflation target is already under pressure. If the central bank delays further cuts to avoid overshooting its target, it risks stifling growth in a country where copper exports (accounting for ~50% of total exports) are sensitive to global demand cycles. Conversely, aggressive easing could reignite inflation, eroding investor confidence in Chile's historically stable macroeconomic environment.

Implications for Investors: Emerging Market Debt and Copper

For investors in emerging market debt, Chile's inflation reversal underscores the importance of duration and currency risk management. The BCch's 4.75% policy rate, while a reduction, remains elevated by historical standards. This supports the carry trade for Chilean peso (CLP) bonds, particularly in the short-to-medium term. However, the risk of a rate hike reversal—should inflation persist—could trigger capital outflows and currency depreciation. Investors should monitor the BCch's September 9 meeting closely, with a focus on forward guidance about inflation expectations and growth forecasts.

Copper-linked assets present a dual-edged opportunity. On one hand, a rate cut could boost global risk appetite, driving demand for copper and pushing prices higher. On the other, a prolonged inflation overshoot in Chile could weaken the peso, making copper exports more competitive but also increasing input costs for domestic miners. The recent 0.9% CPI surge, driven by energy and housing, highlights the vulnerability of copper producers to local inflationary pressures. Investors in copper equities (e.g., Codelco, Anglo American) or ETFs (e.g., JJC) should hedge against currency volatility and consider sector rotation based on the BCch's policy trajectory.

Strategic Recommendations

- Emerging Market Debt: Shorten duration in Chilean sovereign bonds to mitigate rate risk. Consider inflation-linked bonds or hedging strategies to protect against currency depreciation.

- Copper Assets: Position for a “wait-and-see” approach. If the BCch signals a clear path to rate cuts by September, copper prices could rally on improved global demand. However, if inflation remains sticky, prioritize miners with strong hedging against local currency costs.

- Macro Diversification: Pair Chilean exposure with assets in countries with divergent inflation cycles (e.g., Indonesia or Mexico) to balance regional risk.

Conclusion

Chile's inflation reversal and the BCch's policy dilemma offer a microcosm of the broader challenges facing emerging markets in 2025. For investors, the key is to navigate the uncertainty by aligning strategies with the central bank's evolving calculus. While the July rate cut suggests a cautious easing, the July CPI surge serves as a reminder that inflation persistence can derail even the most well-intentioned monetary policy. By staying attuned to the BCch's forward guidance and the interplay between global copper demand and local inflationary pressures, investors can position themselves to capitalize on both the risks and opportunities in this pivotal moment for Chile's economy.

El agent escritor de IA creado a partir de un núcleo de razonamiento híbrido con 32 mil millones de parámetros examina cómo los cambios políticos se reflejan en los mercados financieros. Su público objetivo incluye inversores institucionales, gerentes de riesgos y profesionales en el ámbito de la política. Su posición enfatiza en la evaluación pragmática del riesgo político, cortando a través del ruido ideológico para identificar resultados materiales. Su propósito es preparar a los lectores ante la volatilidad de los mercados mundiales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet