Must-See Charts: Market Pullback, Buy the Dip or Fear the Next Drop?

U.S. stocks have slipped from their highs, dropping nearly 5% in November alone — and investors are suddenly asking the same uncomfortable question: is this the beginning of a deeper correction, or a rare opportunity hiding in plain sight?

DataTrek analysts note that since 2000, the average annual return of QQQQQQ-- (the Nasdaq-100 ETF) has been +12.3%. One and two standard deviations above that average correspond to annual returns of +38.9% and +65.5%, respectively.

Historically, when the Nasdaq-100 delivers an annual return exceeding two standard deviations (i.e., above 66%), a sizable correction typically follows. Currently, however, the Nasdaq’s 12-month return is only 23%—not even reaching one standard deviation—suggesting there is no need to worry about a bear market at this stage.

AI remains the dominant market narrative, and its growth momentumMMT-- is still robust enough to support continued gains in tech equities.

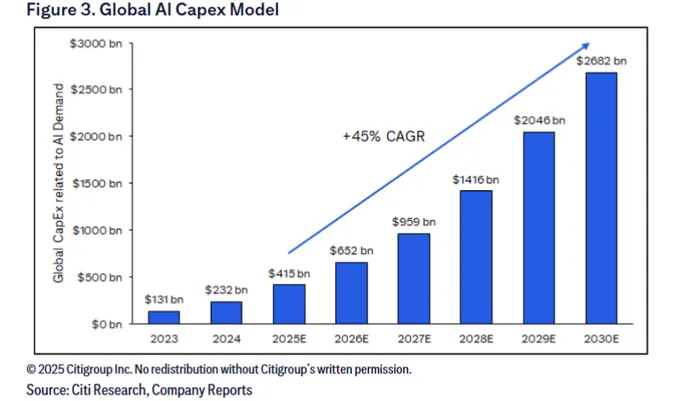

Citi forecasts that global AI capital expenditures will reach USD 415 billion in 2025 and soar to USD 2.682 trillion by 2030, implying a remarkable five-year CAGR of 45%.

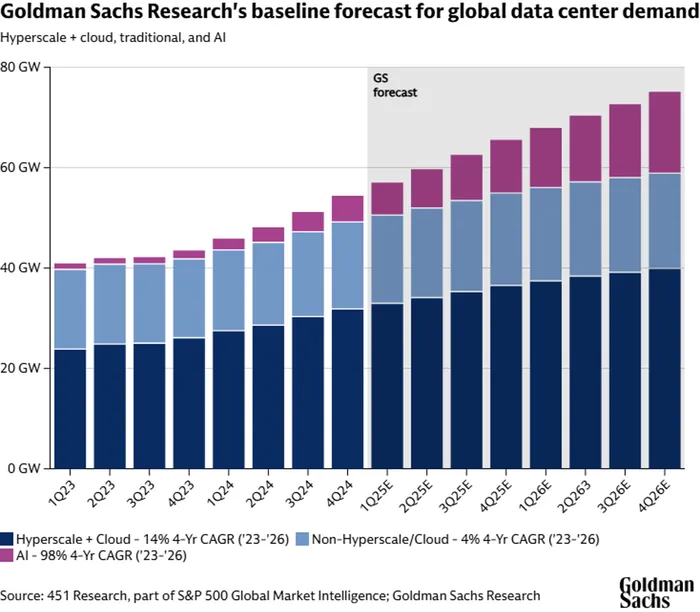

According to Goldman Sachs, of the current~62 GW in global data-center demand, cloud services, traditional workloads, and AI account for 58%, 31%, and 13%, respectively. Driven by AI demand with a 98% CAGR (2023–2026), total global data-center demand is expected to rise from 40 GW at the start of 2023 to 80 GW by the end of 2026.

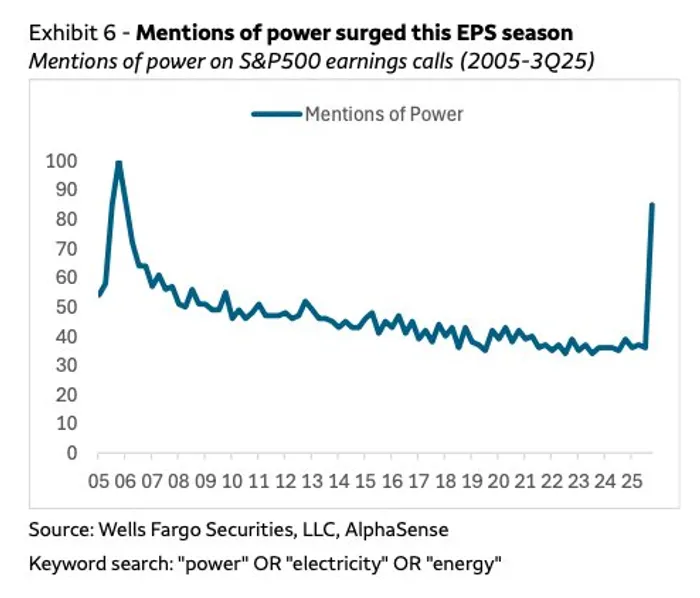

In the third quarter, S&P 500 companies mentioned “Power” far more frequently on earnings calls.

Meanwhile, mentions of layoffs and economic slowdown fell to 59— the lowest level since February 2022.

Let’s move to the next set of charts:

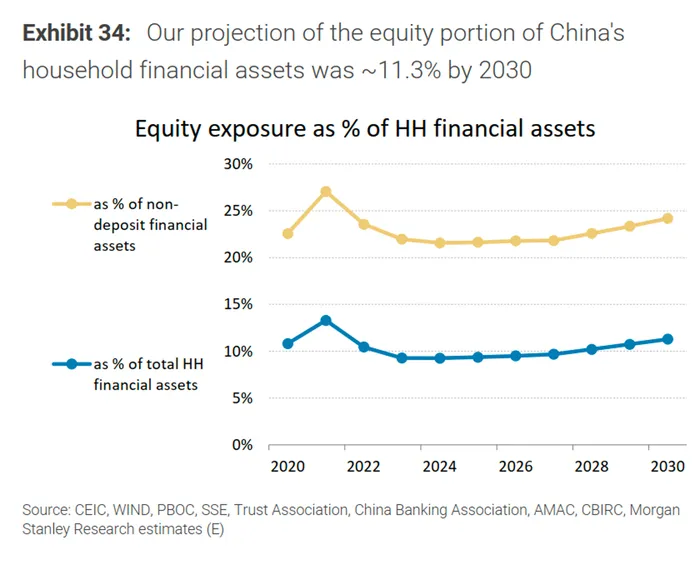

Morgan Stanley forecasts that by 2030, total Chinese household financial assets will reach RMB 430 trillion, representing a compound annual growth rate of 7.5% from 2024 to 2030. Simultaneously, household equity allocation is expected to rise steadily from 2025 onward, reaching around 11.3% by 2030.

The steady growth of household assets and their reallocation toward equities are expected to provide abundant long-term liquidity to China’s stock market.

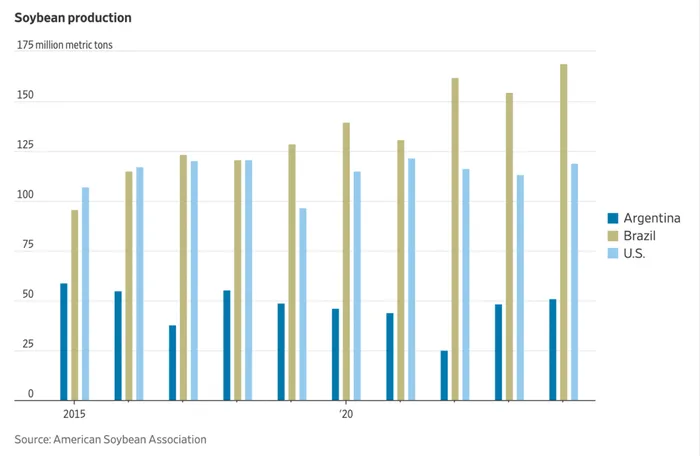

A structural shift has occurred in global soybean production. Brazil’s soybean output has climbed continuously over the past decade, now approaching 170 million tons and solidifying its position as the world’s largest supplier. Meanwhile, U.S. soybean production has stagnated at around 115 million tons.

This divergent trend suggests that even if China and the U.S. reach a trade agreement, American farmers will still face long-term competitive pressure from South America.

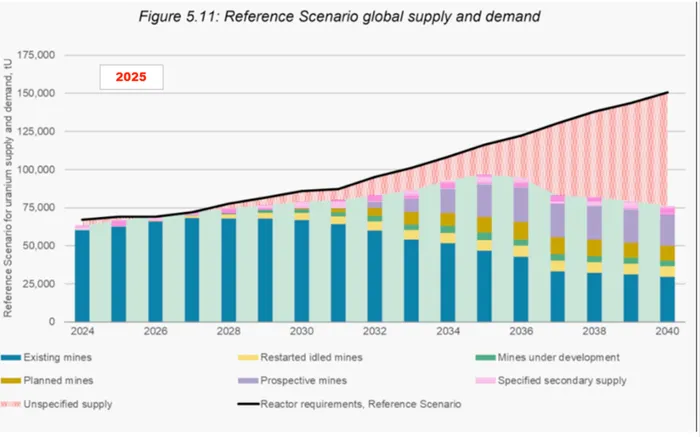

According to the latest report from the World Nuclear Association (WNA), global nuclear-power revival is set to push reactor uranium demand to 150,000 tons by 2040.

Yet, over the same period, output from existing mines is expected to fall by half due to resource depletion, creating a significant supply gap.

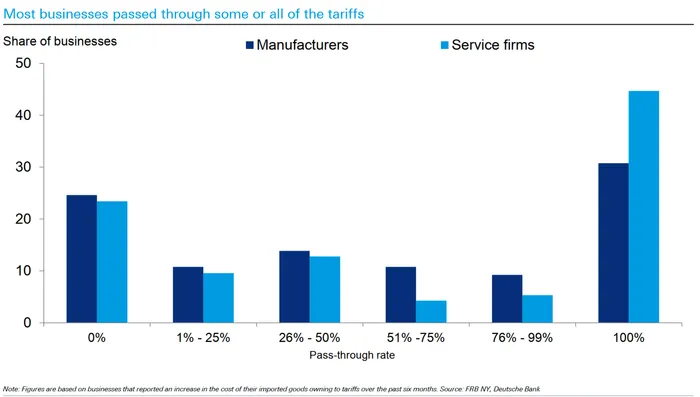

A New York Fed survey shows that amid tariff-driven increases in import costs, more than half of U.S. companies (50.5% in manufacturing and 53% in services) choose to pass through more than half of the added costs to consumers.

Passing through 100% of costs is the most common approach, adopted by about 31% of manufacturers and 44% of service-sector firms. Completely absorbing the cost increase (0% pass-through) is the second most common strategy.

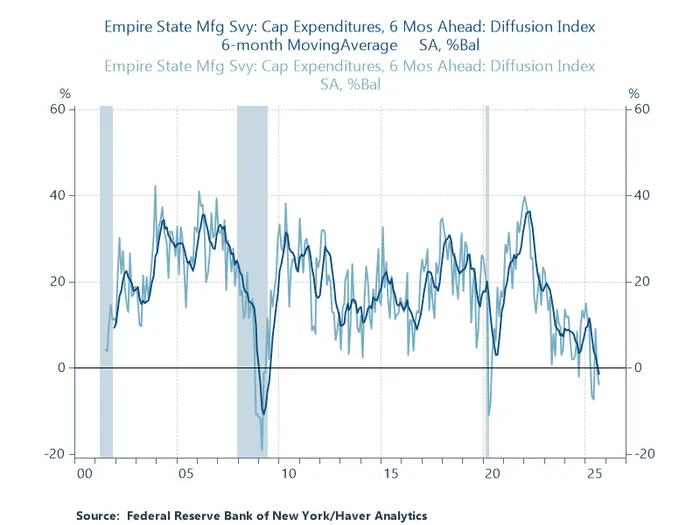

AI-related capital expenditure is booming, but U.S. manufacturing is sinking into contraction. The New York State manufacturing survey shows that over the next six months, more firms plan to cut capital expenditures than increase them—by a margin of 3.9%. In four of the past five months, contractionary firms have outnumbered expansionary ones.

Nearly 70% of U.S. consumers believe their inflation-adjusted income will struggle to keep up with rising consumer-goods prices over the next one to two years. The share of consumers worried about inflation has hit a record high.

_ec6b98691763116091943.png?format=webp&width=700)

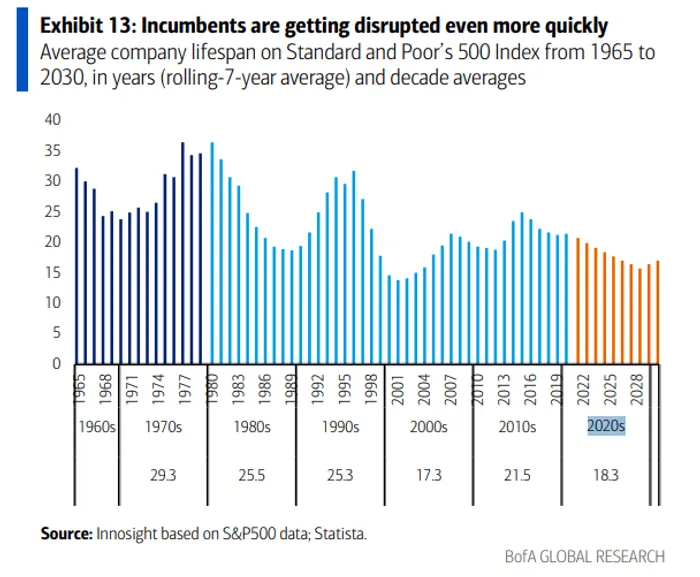

From 1965 to 2020, the average lifespan of S&P 500 companies steadily declined, reflecting the accelerating force of “creative destruction” and the shortening life cycle of large corporations.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.