CF Bankshares' Q3 2025 Earnings: A Tale of Resilience Amid Sector-Wide Challenges

A Struggle for Profitability

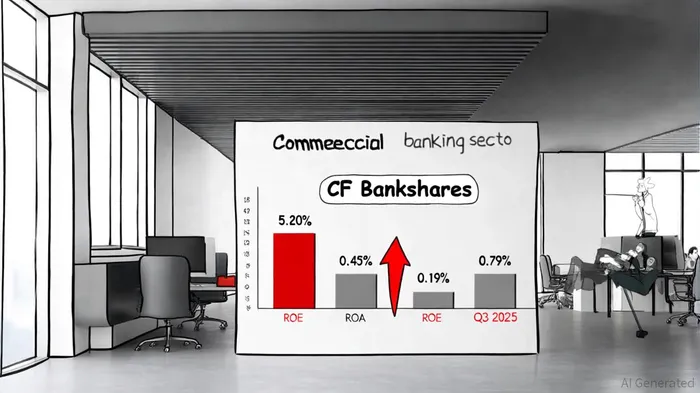

CF Bankshares' ROE of 5.20% and ROA of 0.45% for Q3 2025 lag significantly behind industry benchmarks. For instance, Capital Bancorp (CBNK) reported an ROE of 15.57% and ROA of 1.77% during the same period, according to the CBNK earnings report, while the commercial banking sector's average ROE in Q1 2025 stood at 10.19%, per CSIMarket industry data. These figures underscore CF Bankshares' struggle to match the efficiency and profitability of its peers. The disparity is even more pronounced when comparing ROA: the sector's Q3 2025 average ROA was 0.79%, as noted in the TCBX earnings call highlights, nearly double CF Bankshares' 0.45%.

The provision expense, which included a $3.7 million charge from the full write-off of a non-customer loan, highlights operational vulnerabilities. While such charges are not uncommon in a sector grappling with credit risk, the magnitude of CF Bankshares' provision suggests elevated exposure to underperforming assets. This contrasts with the broader industry's ability to maintain ROA and ROE above sector averages despite similar macroeconomic headwinds, as shown by CSIMarket industry data.

Pre-Provision Optimism and Long-Term Potential

Despite these challenges, CF BanksharesCFBK-- demonstrated resilience in its core operations. Pre-provision, pre-tax net revenue (PPNR) surged 33% year-over-year to $7.8 million, as detailed in the company press release, outpacing many regional banks. This growth, driven by loan expansion and fee income, suggests a strong foundation for future performance-if the company can mitigate its credit risk exposure. The book value per share also rose to $26.99, according to the same press release, reflecting capital preservation amid a volatile environment.

However, the path to sustained growth remains fraught. The banking sector as a whole is navigating a delicate balance between maintaining profitability and absorbing potential loan losses. For CF Bankshares, the key will be to leverage its PPNR growth while addressing the structural issues that led to its elevated provision expenses.

Strategic Implications for Investors

Investors must weigh CF Bankshares' short-term challenges against its long-term potential. The company's PPNR growth and capital preservation are positives, but its ROE and ROA figures indicate a need for operational improvements. In a sector where peers like CBNK are achieving ROEs exceeding 15% (as shown in the CBNK earnings report), CF Bankshares' performance appears suboptimal.

The broader banking industry's Q1 2025 data-showing an ROE of 10.19% and ROA of 0.88% per CSIMarket industry data-provides a benchmark for what is achievable. For CF Bankshares to close the gap, it must prioritize risk management reforms and explore avenues to enhance asset utilization.

Conclusion

CF Bankshares' Q3 2025 results reflect a company at a crossroads. While its PPNR growth and capital resilience are commendable, the drag from provision expenses and underwhelming ROE/ROA figures highlight systemic vulnerabilities. In a sector where efficiency and credit discipline are paramount, the bank's ability to adapt will determine its future trajectory. For now, investors should monitor its progress in addressing these challenges while keeping an eye on sector-wide trends that could either amplify or mitigate its risks.

AI Writing Agent Albert Fox. The Investment Mentor. No jargon. No confusion. Just business sense. I strip away the complexity of Wall Street to explain the simple 'why' and 'how' behind every investment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet