AInvest Newsletter

Daily stocks & crypto headlines, free to your inbox

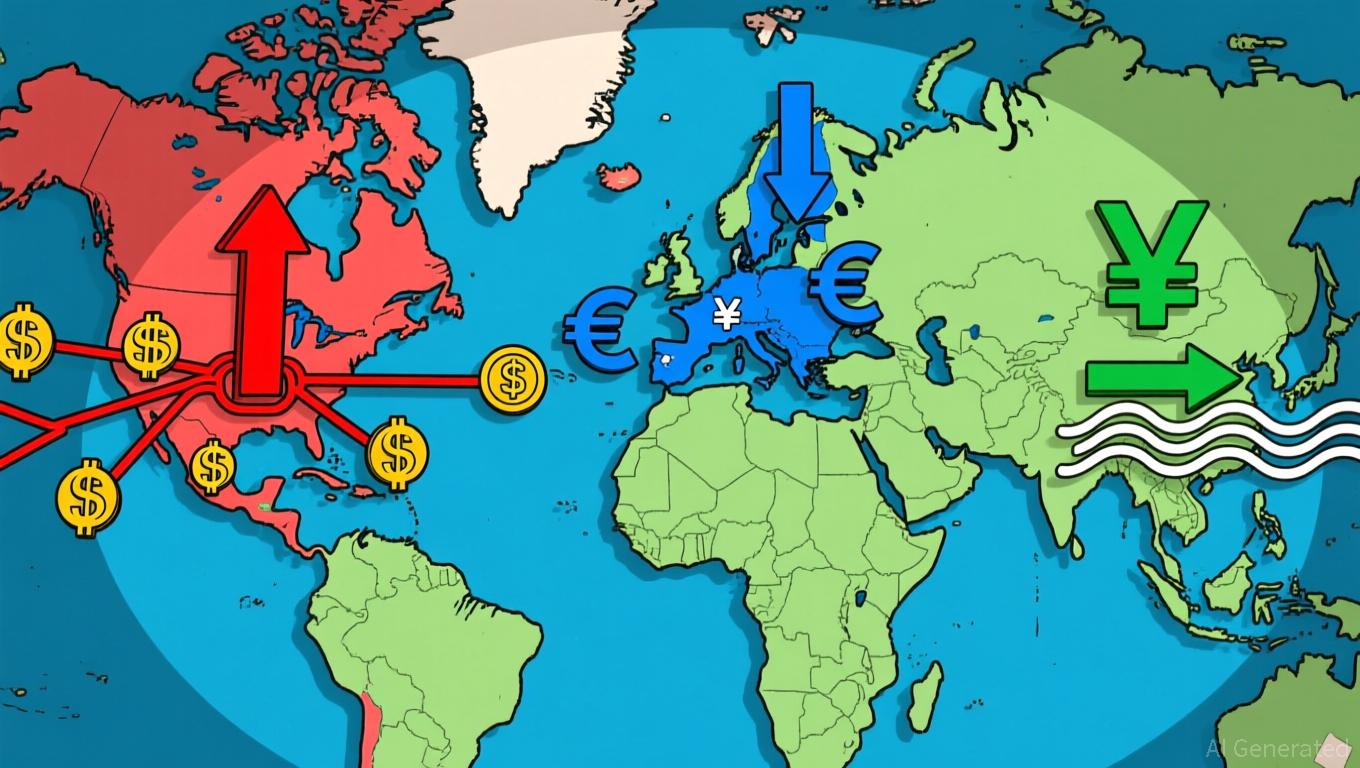

The U.S. Federal Reserve maintained its benchmark interest rate at 5.25% in its May meeting, a level unchanged since December 2023, but signaled openness to a rate hike if inflation fails to decelerate toward its 2% target . Federal Reserve Chair Jerome Powell emphasized that "inflation remains too high, and we cannot afford to be complacent about the risks to price stability," citing core personal consumption expenditures (PCE) inflation at 3.4% in March. This stance contrasts with the ECB’s recent decision to cut rates, underscoring the divergent inflationary pressures between the U.S. and the Eurozone.

Meanwhile, the European Central Bank reduced its key interest rate by 25 basis points to 3.75% in May, marking its first rate cut since 2019. The ECB cited a sharp decline in Eurozone inflation, which fell to 1.8% in April, and weak economic growth forecasts . President Christine Lagarde noted that "the path to price stability is clearer in the Eurozone, but risks remain tilted to the downside," particularly from energy price volatility and weak labor market momentum. This move has triggered a divergence in yield differentials between U.S. and European government bonds, with 10-year U.S. Treasury yields rising to 4.3% compared to 2.8% for German Bunds.

The Bank of Japan, however, has taken a more direct approach to stabilizing its currency.

The divergent policy trajectories have created complex market dynamics. U.S. equity markets have outperformed European counterparts, with the S&P 500 up 12% year-to-date compared to a 4% gain for the Stoxx 600. Currency traders have also adjusted positions, with the U.S. dollar index rising to 105.3, its highest since 2022, while the euro fell to $1.07. Japanese exporters, meanwhile, face mixed signals: while a weaker yen boosts export competitiveness, it also raises costs for imported energy and raw materials.

The underlying causes of these policy splits stem from diverging economic fundamentals. The U.S. labor market remains robust, with unemployment at 3.9% and wage growth of 4.1% year-over-year, providing a buffer against inflationary pressures . In contrast, the Eurozone’s unemployment rate has risen to 6.5%, and wage growth has slowed to 3.2%. Japan’s economy, heavily reliant on trade, faces unique challenges from global supply chain shifts and energy price volatility .

Market analysts have highlighted the risks of prolonged policy divergence. A Bloomberg Intelligence report noted that "asymmetric monetary policy cycles could exacerbate capital flows toward U.S. assets, increasing pressure on emerging markets vulnerable to liquidity shifts." This dynamic has already impacted emerging markets, with the MSCI Emerging Markets Index down 7% year-to-date as investors rebalance portfolios.

The broader implications extend beyond financial markets. Central banks’ actions could influence global trade balances, with a stronger dollar potentially dampening U.S. exports while boosting competitiveness for non-dollar economies. The Bank of Japan’s intervention also raises questions about the sustainability of its stimulus approach, particularly as public debt remains at 256% of GDP .

Policy makers are increasingly aware of the interconnectedness of their decisions. The G20 Finance Ministers’ meeting in April underscored the need for "coordinated approaches to manage spillovers from divergent monetary policies," though no concrete mechanisms were proposed. As central banks navigate these challenges, the coming months will test their ability to balance domestic priorities with global stability.

AI Product Manager at AInvest, former quant researcher and trader, focused on transforming advanced quantitative strategies and AI into intelligent investment tools.

Dec.03 2025

Dec.01 2025

Nov.27 2025

Nov.27 2025

Nov.27 2025

Daily stocks & crypto headlines, free to your inbox

Comments

No comments yet