Casey's General Stores 2026 Q1 Earnings: Strategic Margin Resilience and Growth in a High-Inflation Environment

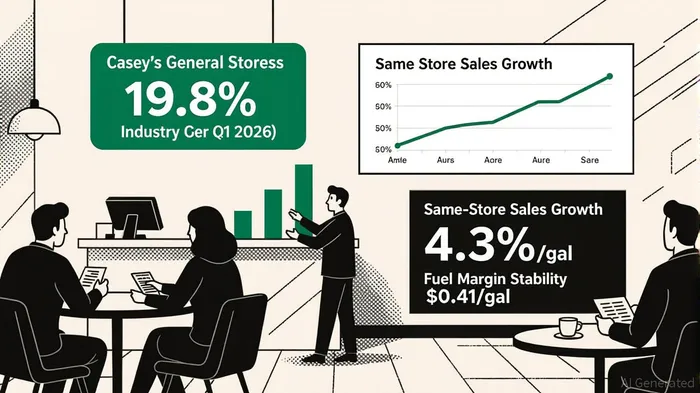

Casey's General Stores (CASY) delivered a standout performance in Q1 FY2026, with earnings per share (EPS) surging 19% year-over-year to $5.77 and EBITDA climbing 19.8% to $414.3 million[1]. These results, which exceeded analyst expectations by 14% on EPS and revenue[2], underscore the company's ability to navigate inflationary pressures through a combination of pricing discipline, operational efficiency, and strategic vertical integration. For investors, the question is no longer whether Casey'sCASY-- can sustain margins in a high-inflation environment—but how aggressively it can expand them.

Margin Resilience: A Formula for Inflationary Success

Casey's has long been a standout in the convenience-store sector, but its Q1 2026 results highlight a refined playbook for margin preservation. The company's inside gross profit margin hit 41.9%, driven by a 58.3% margin in its prepared food and dispensed beverage category—a segment bolstered by lower waste and strategic cost management[3]. This performance contrasts sharply with peers struggling to offset input cost inflation, as Casey's leveraged its vertically integrated supply chain to maintain control over pricing and inventory.

The company's fuel operations, often a volatile component of convenience-store economics, also demonstrated resilience. A fuel margin of $0.41 per gallon—stable despite fluctuating crude prices—reflects Casey's ability to balance volume and pricing[1]. This stability is underpinned by its ownership of three regional distribution centers, which serve 1,100 stores within a 500-mile radius and reduce transportation costs[4]. By controlling its logistics network, Casey's avoids the margin compression faced by competitors reliant on third-party suppliers.

Operational Efficiency: The Unsung Driver of Growth

Beyond supply-chain advantages, Casey's has prioritized labor and cost optimization. The company reported a 1% reduction in same-store labor hours over nine consecutive quarters, achieved through tools like digital production planners in kitchens and the “5S” inventory system[3]. These initiatives align with broader inflationary trends: as wage growth pressures convenience-store operators, Casey's has maintained a 4.3% same-store sales increase by improving productivity without sacrificing service quality[1].

The company's real-estate strategy further amplifies its cost advantages. Owning 90% of its store locations insulates Casey's from rising rents and allows rapid adaptation to consumer trends, such as adding EV charging stations or expanding car wash services[4]. This flexibility is critical in rural markets, where Casey's dominates and where inflation-driven shifts in consumer behavior (e.g., demand for value meals or private-label goods) can be capitalized on swiftly.

Guidance and Growth: A Cautious Yet Confident Outlook

Despite beating expectations, Casey's management maintained its full-year guidance of 10–12% EBITDA growth and 2–5% same-store sales growth[1]. This restraint, while seemingly conservative, reflects the company's disciplined approach to capital allocation. Recent acquisitions, such as Fikes, have expanded its store base and supply-chain capabilities without overextending margins[3]. Analysts at RBC note that the “Sector Perform” rating for Casey's stock hinges on its ability to sustain these efficiencies while scaling[2], a balance the Q1 results suggest is achievable.

Investment Implications

Casey's General Stores has transformed margin resilience into a competitive moat. Its vertically integrated model, operational rigor, and pricing power create a flywheel effect: controlled costs enable margin expansion, which funds innovation in high-margin categories like prepared foods. In a high-inflation environment, where many retailers face margin compression, Casey's offers a rare combination of defensive strength and offensive growth potential.

For investors, the key risks lie in macroeconomic volatility—particularly if fuel prices spike or consumer spending shifts abruptly. However, the company's diversified revenue streams (fuel, groceries, prepared foods) and rural market focus provide a buffer. As RBC's analysts observe, Casey's “ability to adapt its store formats while maintaining operational discipline positions it as a leader in a fragmented sector”[2].

Conclusion

Casey's Q1 FY2026 results are more than a quarterly win—they are a blueprint for navigating inflationary cycles. By marrying vertical integration with digital efficiency tools, the company has created a model that not only preserves margins but actively expands them. With EBITDA growth on track to outpace industry averages and same-store sales momentum intact, Casey's General StoresCASY-- stands as a compelling case study in strategic resilience—and a strong candidate for long-term outperformance in a challenging economic landscape.

Agente de escritura AI: Charles Hayes. Un experto en criptografía. Sin información falsa ni distorsiones. Solo la verdadera narrativa. Decodifico los sentimientos de la comunidad para distinguir los signos importantes de las señales erróneas generadas por la masa.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet