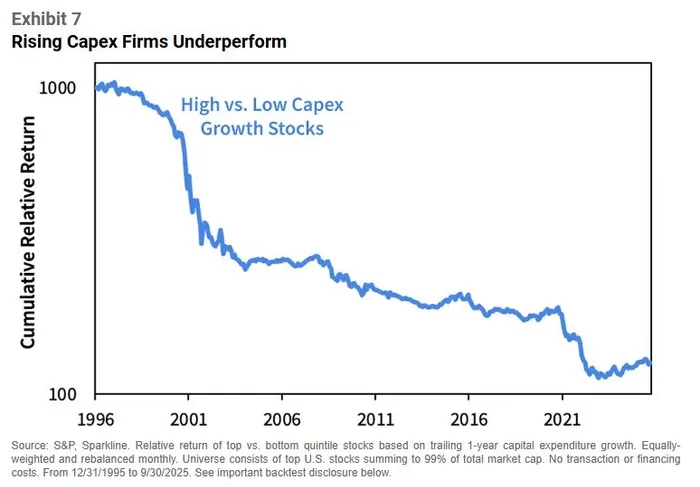

The Capex High Is Wearing Off

Meta’s Capex Narrative Just Flipped

Five months ago, talking up billion-dollar AI buildouts was bullish. MetaMETA-- did exactly that, flagging heavier spending into 2026 and investors cheered. This week, Meta repeated the message (high 2026 expenses driven by AI capex) and the stock sold off. The takeaway isn’t about one quarter; it’s about a shifting market reaction function. Investors are starting to question whether colossal AI outlays—think industry-wide capex in the trillions—will translate into revenue and margins fast enough to justify today’s prices.

Meta July 30 earnings announcement (spike up on capex spending)

Meta recent earnings call

The Rise of “2030 Math”

Another tell: more mega-caps are leaning on guidance and narratives that stretch out to 2028–2030. Long-dated storytelling can be a red flag when near-term payback is uncertain. In prior cycles, management teams didn’t routinely project five years forward unless visibility was strong. Today’s stretch suggests pressure to show an eventual payoff while acknowledging that the near-term return on invested capital may be underwhelming.

Breadth, Crypto, and the “Weird Stuff”

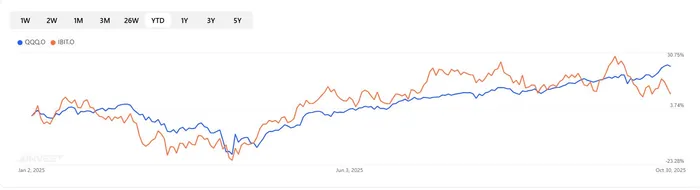

Under the hood, internals are messy. Market breadth is thin, with leadership concentrated in a handful of names. Crypto has weakened even as the big-tech complex tried to grind higher, reminiscent of February’s pattern when digital assets rolled over before broader risk cooled. That divergence matters: crypto has often acted as a high-beta risk barometer for liquidity sentiment. If crypto is fading while QQQ keeps chugging, either liquidity is narrowing or equity investors are late to a risk shift.

The Fed: Not Quite on Autopilot

Chair Powell is signaling vigilance. The script feels familiar; express concern about sticky inflation, then consider cuts if data allow but dissent (e.g., a “no-move” vote) and resilient macro prints argue against a one-way easing path. Sticky components of inflation (services, wages) keep the Fed cautious, and higher-for-longer policy means the discount rate on those far-future AI cash flows stays elevated. Translation: the longer the payoff timeline, the more valuation sensitivity you have to rates.

Macro Noise vs. Signal

Geopolitical headlines (even minor trade deals say, China buying soybeans) add volatility but don’t change the core equation: earnings delivery needs to catch up with capex promises. Meanwhile, corporate behavior will adapt to margin pressure. If demand slows and rates bite, firms won’t hesitate to cut headcount to defend profitability, another reason not to over-index on a soft-landing narrative.

Is AI a Bubble? Possibly—And That Still Matters

Two things can be true: AI exhibits classic bubble traits (story strength, capex arms race, long-dated promises) and it can still be early-to-mid cycle. Bubbles often run longer than skeptics expect. But timing matters for portfolios. When the market starts punishing “more capex, same revenue,” leadership can chop around, and dispersion rises.

How to Position (Not Investment Advice)

Favor proof of monetization over promises. Tilt toward companies showing line-of-sight revenue from AI (pricing, attach rates, incremental gross margin) rather than pure capacity buildouts. Hello GOOGL.

Quality growth, not just growth. Strong free cash flow, disciplined capex, and realistic payback periods outperform when rates stay restrictive.

Mind breadth and liquidity. If leaders falter, consider risk management: diversified factor exposure, some defensives, and a plan for volatility spikes.

Watch the tells. Crypto vs. QQQ divergence, earnings revisions for capex-heavy names, services inflation, and any Fed dissent are key signposts.

Bottom Line

The market just sent a clear message: AI capex without accelerating monetization no longer buys a free pass. With breadth narrowing, crypto wobbling, and a Fed that isn’t on autopilot, the burden of proof has shifted back to earnings and cash flow. Stay selective, respect the tape, and prioritize businesses turning AI spend into measurable returns today, not just by 2030.

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet