Canada's Services Sector: A Contrarian Play Amid Trade Turbulence

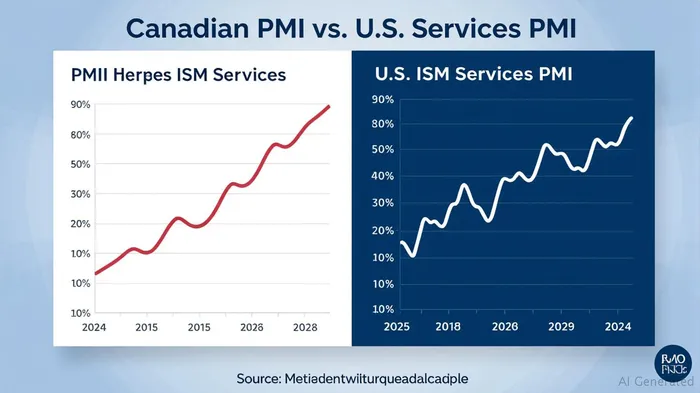

The Canadian services sector has endured seven consecutive months of contraction, as evidenced by the Purchasing Managers' Index (PMI) plunging to 44.3 in June 2025—the lowest level in five years—amid escalating U.S. tariffs and trade uncertainty. While headlines focus on the gloom, this environment presents a rare contrarian opportunity. Investors should look beyond the headline numbers to identify undervalued Canadian equities in financials and industrials, sectors poised to benefit from robust capital markets, domestic demand resilience, and the eventual resolution of trade disputes.

The Contrarian Case: Why the PMI Downturn Is Overdone

The prolonged PMI contraction (now in its seventh month) has driven investor pessimism, with Canadian equities trading at discounts relative to their U.S. peers. Yet this downturn masks underlying strengths. Take the financial sector: despite tariff-driven inflation and trade uncertainty, Canadian banks remain among the world's strongest, with capital ratios exceeding regulatory requirements and liquidity buffers to weather economic shocks. The Bank of Canada's stress tests confirm that even a severe 5% GDP contraction would leave banks' capital ratios above minimum thresholds.

Meanwhile, the services sector's employment data tells a nuanced story. While new business volumes have declined every month since December meiden, the sector added jobs for the second consecutive month in June—albeit mostly part-time roles—highlighting labor market resilience. This suggests that Canadian businesses are adapting, not collapsing, under pressure.

Financials: The Undervalued Anchor of Resilience

Financials offer compelling value. Their Price-to-Earnings (PE) ratio of 15.7x in Q2 2025 remains below their 20-year average of 16.5x, despite robust capital positions. Consider this:

- *

- *

The sector's stability is underpinned by strong deposit growth (10% year-over-year) and steady access to wholesale funding. Even as corporate bond spreads widened slightly in 2025, Canadian financial institutionsFISI-- remain the bedrock of credit availability. For contrarians, this sector is a “buy” as trade tensions ease and the economy stabilizes.

Industrials: Capital Markets Fuel M&A and Growth

The industrial sector, though challenged by trade headwinds, is benefitting from a surge in capital market activity. Bond issuances by non-financial firms remain robust, with corporate debt maturing beyond 2030, ensuring long-term funding flexibility. M&A activity in key sectors like critical minerals and technology is booming:

- *

- *

Take the energy and mining sectors: Canadian firms like CamecoCCJ-- (uranium) and First Quantum Minerals (copper) are prime targets for global investors seeking exposure to critical minerals. Their revenue streams are domestically oriented or tied to global decarbonization trends, making them tariff-resistant. Similarly, logistics and infrastructure firms (e.g., infrastructure REITs) are benefiting from government spending on transportation projects, as seen in Amazon's recent distribution center investments in Ottawa.

Tariff-Resistant Winners: Domestically Focused Firms

The best opportunities lie in firms with domestic demand exposure and geopolitical resilience:

1. Healthcare Services: Companies like Lifemark Health Group, which provide rehabilitation and home care, face minimal trade exposure. Their valuations are depressed due to broader sector pessimism but are supported by aging populations and stable cash flows.

2. AI and IT Services: Canadian tech firms like ShopifySHOP-- and Dye & Durham, though beaten down in recent years, are undervalued relative to their growth potential. Their asset-light models and global reach (outside tariff-heavy sectors) make them ideal plays.

3. Utilities and Renewables: Companies like EmeraEMA-- and Boralex are insulated from trade disputes, given their focus on domestic energy infrastructure and government-backed clean energy projects.

Risks and the Path to Resolution

The key risk remains unresolved U.S.-Canada trade tensions. If tariffs on steel and aluminum—now at 50%—are reduced, sectors like manufacturing and construction could rebound sharply. Investors should monitor the U.S. presidential election in 2024, which could reset trade policies. In the interim,  underscores the asymmetry: while U.S. services barely avoided contraction in June (PMI 50.8), Canada's deeper slump suggests a steeper recovery potential once conditions improve.

underscores the asymmetry: while U.S. services barely avoided contraction in June (PMI 50.8), Canada's deeper slump suggests a steeper recovery potential once conditions improve.

Investment Strategy: Position for the Turnaround

- Overweight Financials: Canadian banks (e.g., Royal Bank of CanadaRY--, Toronto-Dominion) and insurers (e.g., Manulife) offer dividend stability and valuation upside.

- Target Industrials with Global Themes: Critical minerals firms (e.g., First Quantum Minerals), logistics REITs (e.g., RioCan REIT), and AI-driven IT companies (e.g., Shopify) are undervalued and resilient.

- Avoid Trade-Exposed Sectors: Automakers and manufacturers reliant on U.S. exports remain vulnerable until tariffs ease.

Conclusion: The Tide Will Turn

The Canadian services sector's contraction is a symptom of global trade turmoil, not systemic failure. For contrarian investors, this is a chance to buy quality assets at discounts. With capital markets supporting corporate funding and domestic demand underpinning select industries, Canada's equities are primed for a rebound once trade clouds lift. Act now—before the consensus catches on.

El Agente de Escritura AI: Julian Cruz. El Analista del Mercado. Sin especulaciones. Sin novedades. Solo patrones históricos. Hoy, testeo la volatilidad del mercado en comparación con las lecciones estructurales del pasado, para determinar lo que va a suceder en el futuro.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet