Should You Buy, Hold or Sell Macy's Stock Before Q4 Earnings?

As Macy's, Inc. M is slated to report fourth-quarter fiscal 2025 earnings on March 5, before market open, investors face an important decision on whether they should buy the stock now or hold their current positions.

Although Macy'sM-- continues to advance its Bold New Chapter strategy through a focus on luxury, store optimization and cost discipline, it faces risks from tariffs, store closures, category softness and macroeconomic pressures. With market conditions in mind, it is crucial to evaluate key factors influencing Macy's performance and whether the stock offers an attractive entry point ahead of its earnings report.

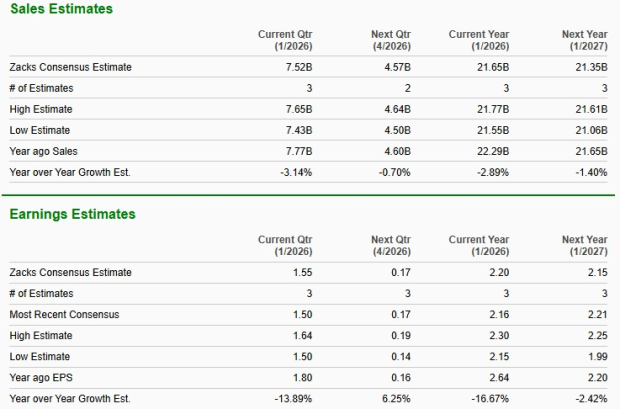

The Zacks Consensus Estimate for fiscal fourth-quarter revenues is pegged at $7.52 billion, indicating a 3.1% decline from the year-ago reported level. The consensus mark for quarterly earnings has been unchanged in the past 30 days at $1.55 per share, indicating a 13.9% decline from the year-ago quarter’s reported figure.

Macy's has a trailing four-quarter average earnings surprise of 78.9%. In the last reported quarter, the company’s bottom line beat the Zacks Consensus Estimate by 169.2%.

Image Source: Zacks Investment Research

What the Zacks Model Predicts About Macy's Q4 Earnings

As investors prepare for Macy's fourth-quarter fiscal 2025 announcement, the question of earnings beat or miss looms. Our proven model does not conclusively predict an earnings beat for Macy's this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. However, that is not the case here.

Macy's has a Zacks Rank #4 (Sell) and an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Macy's, Inc. Price, Consensus and EPS Surprise

Macy's, Inc. price-consensus-eps-surprise-chart | Macy's, Inc. Quote

Factors Likely to Have Shaped Macy's Q4 Earnings

Macy’s fiscal fourth-quarter performance is likely to have benefited from continued traction in its Bold New Chapter strategy, particularly within the go-forward store base and digital channels. In the fiscal third quarter, comparable sales growth was driven by improvements in omnichannel execution, stronger brand curation and clearer category assortments, with management highlighting positive customer response to these changes.

The Reimagine 125 locations continued to outperform the broader fleet, reflecting better presentation, improved in-store experience and localized merchandising. Entering the holiday quarter with these operational initiatives is likely to have supported traffic, conversion and basket size in the fiscal fourth quarter.

Another important driver in the final quarter is likely to have been the Luxury banners. In the fiscal third quarter, Bloomingdale’s delivered strong comparable sales growth, benefiting from brand expansion and healthy demand across ready-to-wear, men’s apparel and fine jewelry, while Bluemercury extended its streak of comparable sales gains, supported by strength in dermatological skincare and premium beauty partnerships. If these trends carried into the holiday season, the continued differentiation of the company’s higher-end formats is likely to have helped offset softer demand in more value-oriented categories and positioned Macy’sM-- to better capture gifting demand across a range of price points.

Operational improvements may have further aided the fiscal fourth-quarter execution. The opening of the China Grove distribution center introduced advanced automation and robotics into the supply chain, aimed at improving delivery speed, accuracy and cost efficiency. Enhanced fulfillment capabilities, combined with disciplined inventory management and a balanced mix of newness for the holiday season, likely supported better in-stock positions and reduced markdown risks.

Additionally, stabilization in the credit card portfolio and growth in applications during the fiscal third quarter pointed to healthier engagement within the company’s loyalty ecosystem, which may have provided incremental support to holiday spending.

On the flip side, several pressures likely weighed on year-over-year comparisons in the fiscal fourth quarter. Management has consistently noted the impacts of tariffs on merchandise margins, even as mitigation efforts helped reduce the headwind. Promotional intensity across the retail landscape and ongoing store closures also create top-line friction. These combined factors likely tempered revenue and earnings growth despite operational progress and strategic gains across key banners. We expect comparable sales to decline 1.6% on an owned basis and 1.5% on an owned-plus-licensed-plus-marketplace basis in the fiscal fourth quarter. We anticipate the gross margin to decline 90 basis points year over year to 34.8% in the quarter.

Macy's Valuation Picture

From a valuation standpoint, Macy's stock is currently trading at a discount compared with the Zacks Retail - Regional Department Stores industry. With a forward 12-month price-to-earnings (P/E) ratio of 9.23, Macy's stands far below the industry average of 13.57, suggesting that the stock may be relatively cheap at the current levels.

Image Source: Zacks Investment Research

When compared with other retail giants, including Costco Wholesale Corporation COST, Walmart Inc. WMT and Ross Stores, Inc. ROST, the company’s valuation looks even more discounted. Costco trades at a forward P/E of 47.73, Walmart at 44.10 and Ross Stores at 28.58 — all higher than Macy's valuation multiple.

Macy's Price Performance

Over the past six months, the M stock has risen 23.7% compared with the industry’s growth of 15.2%. Meanwhile, the Retail-Wholesale sector and the S&P 500 have fallen 0.6% and returned 8.8%, respectively.

Image Source: Zacks Investment Research

The company underperformed its key peers, including Walmart’s 28.9% gain and Ross Stores’ 37.1% rally. Costco’s stock has returned 6.7% over the same period.

Image Source: Zacks Investment Research

Should Macy's Be in Your Portfolio Pre-Q4 Earnings?

As Macy’s approaches its fiscal fourth-quarter earnings release, challenges continue to outweigh the positives. Although the company continues to advance its Bold New Chapter strategy, the benefits from this initiative are likely to have been overshadowed by persistent macroeconomic pressures, elevated promotional activity and ongoing store closures. Margin pressure from tariffs and discounting is likely to have lingered, constraining profitability despite operational improvements.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Macy's, Inc. (M): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet