Should You Buy, Hold, Or Sell IONQ Stock Ahead of Q4 Earnings?

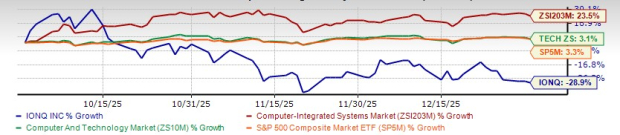

IonQ IONQ is scheduled to release its fourth-quarter and full-year 2025 results on Feb. 25, amid rapid strategic execution and expansion efforts. However, a complex geopolitical backdrop and broad-based tech selloffs have weighed on overall growth momentum. The company’s stock declined 28.9% during the October-December quarter of 2025, despite bold moves in quantum networking, space-based communications and key acquisitions.

IonQ reported earnings beat in just one of the trailing four quarters and missed on the other three occasions, the average negative surprise being 343.53%.

How are things shaping up ahead of the fourth-quarter earnings release? Let’s take a closer look.

October-December Share Performance of IONQ

Image Source: Zacks Investment Research

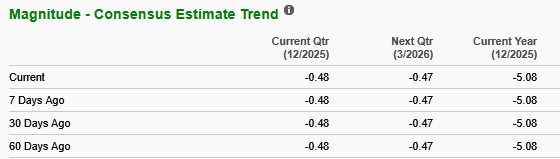

How Are Estimates Poised for IonQ?

The Zacks Consensus Estimate for fourth-quarter EPS has remained unchanged at a loss of 48 cents per share over the past 60 days. The estimated figure indicates 48.4% improvement from the year-ago loss per share.

The consensus mark for fourth-quarter revenues is pegged at $40.3 million, indicating 244.2% year-over-year growth.

For 2025, IONQIONQ-- is expected to register a 151.8% increase from a year ago in revenues. Its bottom line is expected to witness a decline to a loss of $5.08 per share from a loss of $1.56 a year ago.

Image Source: Zacks Investment Research

What to Expect From IonQ’s Q4 Performance

IonQ’s third-quarter revenues of $39.9 million were up 222% year over year and 37% above the high end of its guidance. The company stated that fourth-quarter 2025 revenues are expected to exceed the Q3 levels, breaking the seasonality seen in prior years. The company also raised its full-year 2025 revenue outlook to $106-$110 million.

During the third quarter of 2025, IonQ strengthened its position as a full-stack quantum platform provider. The company closed its acquisition of Oxford Ionics, expanding its quantum computing capabilities. During the quarter, IonQ also delivered #AQ 64 on its Tempo system ahead of schedule and achieved a record 99.99% two-qubit gate fidelity milestone. After the quarter ended, IonQ closed its acquisition of Vector Atomic and raised $2 billion in October, bringing pro forma liquidity to approximately $3.5 billion and significantly strengthening its financial flexibility. All these are expected to have contributed positively to IONQ’s fourth-quarter performance.

At the same time, investment remains heavy. IonQ’s third-quarter operating expenses were $208.7 million, with R&D at $66.3 million and an adjusted EBITDA loss of $48.9 million. Full-year EBITDA guidance remains at a loss of $206–$216 million, signaling continued aggressive spending.

However, despite strong operational progress and raised revenue guidance, IonQ’s stock declined during the October–December quarter. The pullback occurred amid broader market volatility in high-growth technology stocks. While IonQ continues to expand its exposure to government and sovereign contracts, near-term equity performance may remain sensitive to broader market conditions.

Competitive Positioning

Rigetti Computing RGTI: In the fourth quarter of 2025, Rigetti Computing is expected to have witnessed continued execution on its system roadmap rather than a sharp revenue inflection. With $5.7 million in purchase orders for two Novera quantum systems scheduled for delivery in the first half of 2026, fourth-quarter revenues are likely to remain modest, with greater contribution expected next year. Investors will focus on progress toward the planned 100+ qubit chiplet-based system, fidelity improvements and updates on additional system orders. The stock carries a Zacks Rank #3 (Hold).

D-Wave Quantum QBTS: In the fourth quarter of 2025, D-Wave’s performance is expected to have built on its recent booking momentum rather than show an immediate step-change in recognized revenue. The company announced a 10 million euro booking tied to partial capacity of its Advantage2 system under a multiyear agreement, which is likely to have supported backlog growth more than near-term revenues. Continued enterprise and research partnerships may have strengthened demand visibility. The stock carries a Zacks Rank #3.

What the Zacks Model Unveils for IONQ Stock

Our proven model does not conclusively predict an earnings beat for IonQ this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here.

Earnings ESP: IonQ has an Earnings ESP of 0.00%. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank of 3. You can see the complete list of today’s Zacks #1 Rank stocks here.

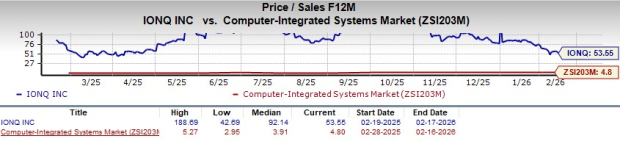

IONQ's Valuation

The stock is currently trading at a lofty forward 12-month price-to-sales (P/S) ratio of 53.55, which is significantly higher than the industry average of 4.8. This exceptionally high forward P/S ratio raises the risk of a sharp pullback if fourth-quarter results or the guidance for 2026 disappoint.

Image Source: Zacks Investment Research

Our Take

IonQ’s strong third-quarter performance, raised full-year revenue outlook and expectation for stronger fourth-quarter revenues signal solid commercial execution. The company also boosted liquidity following its October capital raise. However, the adjusted EBITDA losses projection of $206–$216 million for 2025 reflects continued heavy investment. With tech-sector volatility pressuring the stock, investors may prefer to stay cautious ahead of the fourth-quarter earnings release, consistent with its Zacks Rank.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

IonQ, Inc. (IONQ): Free Stock Analysis Report

Rigetti Computing, Inc. (RGTI): Free Stock Analysis Report

D-Wave Quantum Inc. (QBTS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet