Why Buffett Holds a Record $334.2 Billion in Cash?

Buffett is renowned for his stock-picking acumen, yet nowadays, he shows an increasing inclination towards holding cash. Two days ago, Berkshire Hathaway, the company under Buffett's leadership, released its fourth-quarter and full-year financial reports for 2024, accompanied by Buffett's annual letter to shareholders.

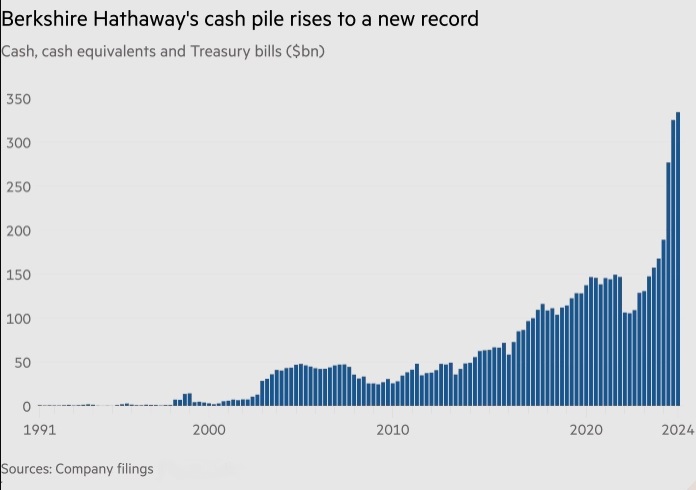

As of the end of 2024, the total amount of cash and cash equivalents held by this renowned investor's company, Berkshire Hathaway, reached a staggering $334.2 billion, setting a new historical high. The proportion of these assets in the company's portfolio is also the highest since 1998.

Maintaining a large cash reserve has always been a consistent practice of Berkshire. However, the continuous expansion of the cash reserve scale recently has drawn the attention of some market observers. By carefully studying Buffett's latest letter to shareholders, we can seek clues to understand the views of this 94-year-old on the stock market, as well as his perspectives on long-term strategies, market conditions, and diversified investment portfolios.

Where Does the Cash Come From?

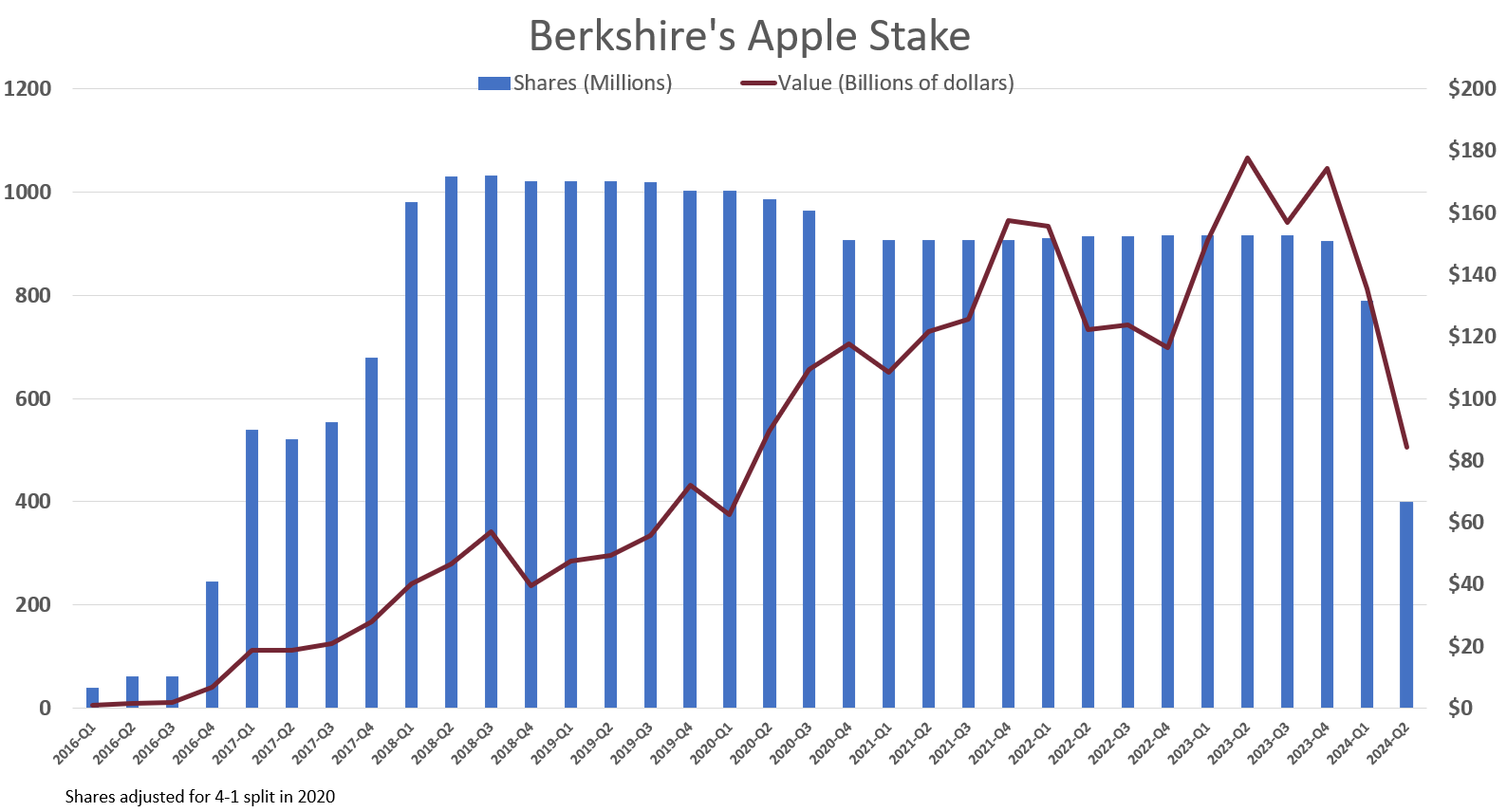

One of the reasons for the cash accumulation is that Berkshire has sold a substantial amount of Apple stocks. In recent years, the valuation of Apple stocks has been much higher than when Buffett's company established its position from 2016 to 2018.

According to data from FactSet, starting from the end of 2023, Berkshire has reduced its shares in Apple for four consecutive quarters. In the fourth quarter of last year, Berkshire temporarily halted further sales of Apple shares.

This is because this portion of the position in Berkshire Hathaway's stock portfolio has already accounted for a significant proportion. When his designated successor, Greg Abel, eventually takes over the company, he will be responsible for this transition.

Some investors and analysts speculate that Buffett's conservative moves over the past year are not a judgment on the market but rather a preparation for future deployments by reducing overly large positions and accumulating cash. The massive amount of cash will provide the successor with room for trial and error, especially for this successor who has been hailed as a prophet by the world.

Historical experience shows that new management often engages in aggressive mergers and acquisitions due to performance pressure (such as Microsoft's acquisition of LinkedIn in the early days of Satya Nadella's tenure). However, Berkshire's $334.2 billion reserve is sufficient to offset the potential losses of any single transaction.

Why Hoard a Large Amount of Cash?

Buffett also seems to be well aware that his move of holding a large amount of cash has received significant attention from the market. In his letter to shareholders, he stated that although some commentators believe that Berkshire's cash position is extremely high, the vast majority of the funds are still invested in stocks, and this preference will not change.

Buffett emphasized, Berkshire's shareholders can rest assured that we will always invest the majority of our funds in stocks - mainly American enterprises, but many of these companies also have important businesses in the global market. Berkshire will never prefer to hold cash equivalents while ignoring the equity of high-quality enterprises, whether it is a controlling stake or a partial stake.

In fact, Berkshire's huge cash holdings have raised questions among shareholders and observers, especially in a situation where interest rates are expected to decline from multi-year highs. In recent years, the CEO and Chairman of Berkshire has expressed frustration about the expensive market and the scarcity of buying opportunities. Some investors and analysts have grown impatient with the lack of action and are seeking explanations.

1. The Valuation Trap

Long-time observers of Berkshire believe that the main reason why Buffett is hoarding cash is the currently high market valuation.

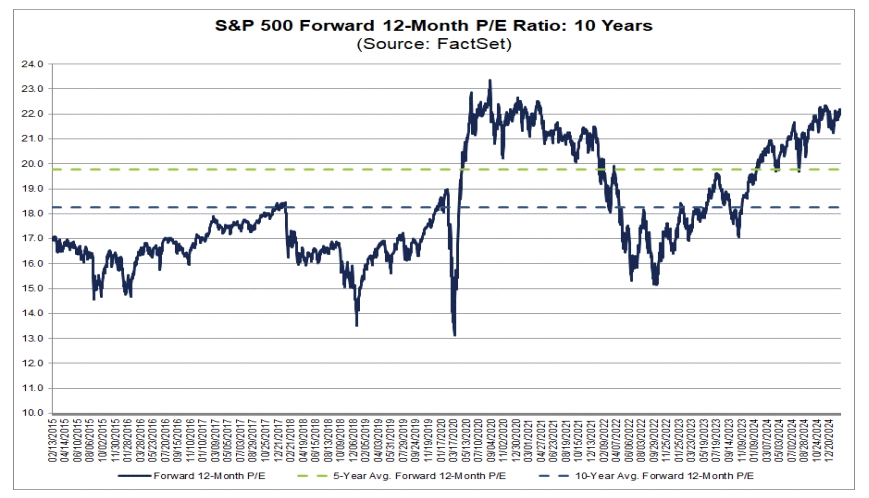

The current forward price-to-earnings ratio (P/E) of the S&P 500 is 22.3 times, which is a 20% premium compared to the 10-year average of 18.6 times. The valuation of technology stocks, in particular, deviates significantly from the historical median. In the fields where Buffett excels, it has become difficult to find bargains among high-quality large enterprises, making it challenging for Buffett to find investment targets that meet his investment criteria. Take Apple as an example; its P/E ratio exceeded 30 times at one point in 2024, prompting Buffett to continuously reduce his holdings to the current 28%. As Buffett emphasized in his letter, We rarely find ourselves in a position of opportunity, which is in line with his creed of being fearful when others are greedy.

Among the industries Buffett is familiar with, the prices of the large, high-quality enterprises that the company is looking for have risen too high, and stock pickers cannot be confident that an investment will bring substantial returns to Berkshire and its shareholders.

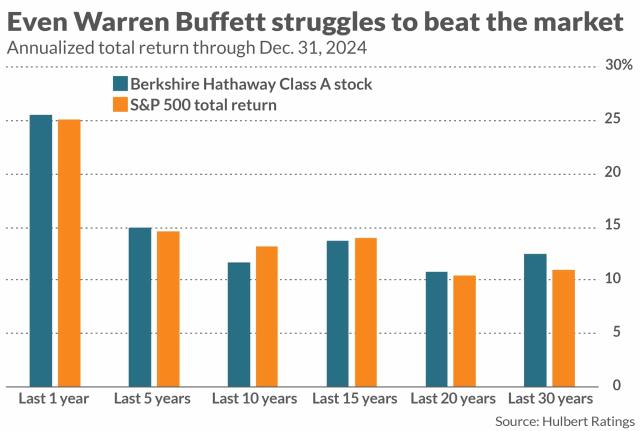

Statistics from The Wall Street Journal show that Berkshire's return rate over the past decade (225%) has already lagged behind that of the S&P 500 (241%), confirming the dilemma of the curse of scale where it is difficult for large entities to perform well.

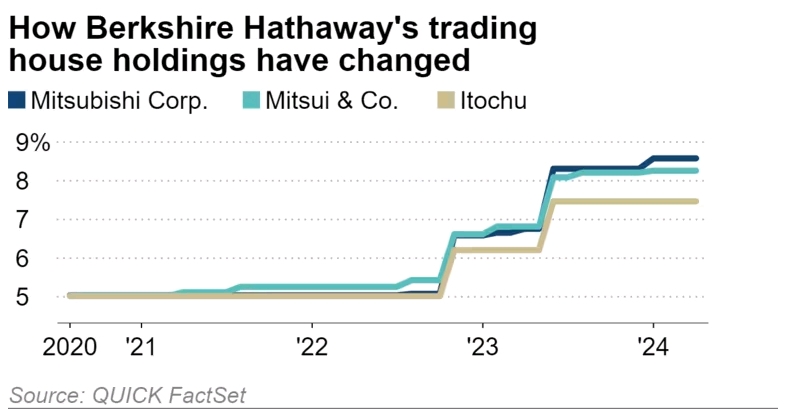

2. The Value Depression

In stark contrast to the US stock market, the five major Japanese trading houses (such as Itochu and Mitsubishi) that Berkshire has heavily invested in have an average P/E ratio of only 5-8 times, a dividend yield of 3%-6%, and have achieved arbitrage through zero-interest-rate bond financing in Japan. As of the end of 2024, this investment has a floating profit of $9.7 billion, and the annual dividend income reaches $812 million. This cross-market valuation gap reveals Buffett's logic of exchanging cash for time: shrinking the front line in the US stock market bubble and shifting to Asian assets with a greater margin of safety.

Moreover, it is likely that the investment in Japanese assets will continue to increase in the future, and his successor will also hold Japanese assets for decades to come.

3. The Cushion

This scale is reminiscent of the classic case during the 2008 financial crisis when Buffett injected $10 billion in preferred stock into Goldman Sachs, with an annual return rate of 17%. In the current environment of geopolitical turmoil and the intensifying risk of future AI regulation, the cash reserve is essentially a put option, reserving the initiative to capture asymmetric returns.

4. The Arbitrage Space at the End of the Interest Rate Cycle

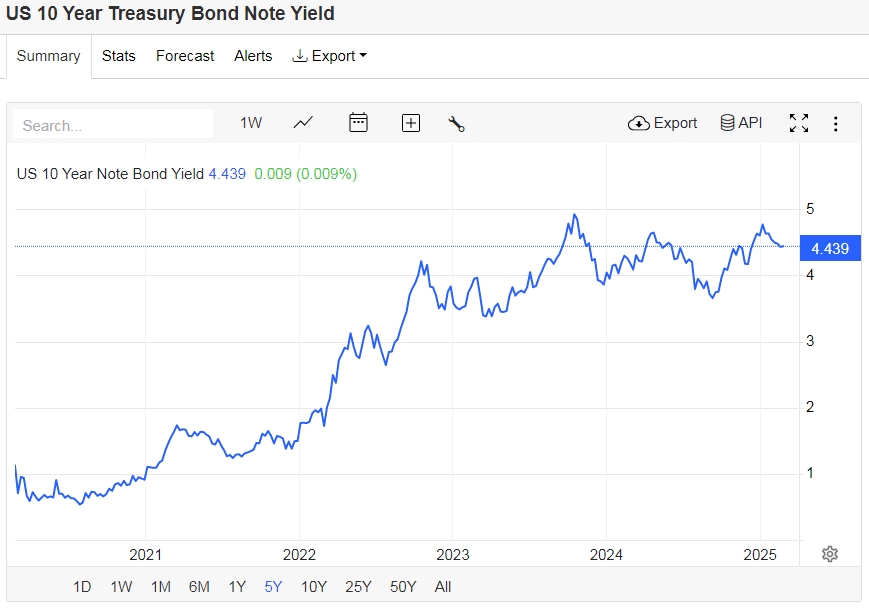

Although the market's expectation of the Federal Reserve's interest rate cuts is on the rise, the yield of short - term US Treasury bonds still remains close to 4.5%. Based on the estimation of Berkshire's cash reserves in the first three quarters of 2024, the interest income alone exceeded $10 billion. In the context where the yield of low - risk assets is rarely higher than the dividend yield of the S&P 500 (1.5%), this cash cow model has become a practical choice for hedging against inflation.

The Dynamic Balance of Value Investing

Buffett reaffirmed in his letter, Berkshire will never prefer cash over the equity of high-quality enterprises. This statement echoes his argument during the Internet bubble in 1999 that cash is a call option. Although the current cash proportion has reached a historical peak, the growth in the value of non-listed controlled enterprises has offset the decline in stock holdings.

Compared with the preference for low-valuation assets in the 1970s (such as Berkshire Hathaway's textile factory), the current strategy places more emphasis on the stability of cash flow. The investment in Japanese trading houses reflects this shift: enterprises like Mitsubishi have a stable return on equity (ROE) of over 10% and have benefited from the dividend increase brought about by Japan's corporate governance reform. This combination of high dividend + low volatility is essentially an advanced substitute for cash.

Problems cannot be solved by hope; action must be taken - Buffett quoted Munger's maxim to explain the current strategy. This is similar to the history when the two of them remained inactive during the technology bubble in 2000 and eventually made a profit of $4 billion by bottom-fishing PetroChina in 2003.

Conclusion

Buffett's cash empire is essentially the ultimate response of a value investor to the market cycle. When the Buffett Indicator (the total market value of US stocks/GDP) breaks through the 200% warning line, this octogenarian has built an anti-fragile barrier with $334.2 billion in cash. This is both a long-term belief in the American Miracle and a calm hedge against short-term enthusiasm. As stated at the end of the letter, Berkshire's future will still be rooted in the United States, but our wallets will always be open to global value - in an era of valuation differentiation and order reconstruction, cash is not the end but the starting point of the next miracle.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.