Not a Bubble! Semiconductors and Energy Power Enter Long-Term Uptrend Supercycle

Is the AI boom another tech bubble—or the start of a decades-long transformation? While skeptics warn of hype, trillions of dollars in real investments and tangible demand tell a very different story.

OpenAI recently signed compute contracts worth up to $1 trillion with major tech giants including NVIDIANVDA--, BroadcomAVGO--, Oracle, and AMDAMD--. The promised investments far exceed OpenAI’s current revenue, tightly linking these companies’ future profits to OpenAI’s success. Stock markets have responded enthusiastically—AI stocks are once again hitting record highs.

However, these massive AI investments have yet to show matching monetization results, fueling persistent doubts about whether the AI frenzy is another bubble. A recent MIT study found that only 5% of companies have seen measurable profit-and-loss impacts from AI adoption.

Yet, Citigroup believes this AI boom is fundamentally different from the dot-com bubble. The key distinction lies in the “clear off-ramp”—a growing, externally validated demand from enterprises adopting AI.

In 2000, many internet firms poured billions into advertising for customers who ultimately didn’t exist. Today, AI companies face visible, reliable demand from enterprise applications in knowledge retrieval, customer service, and healthcare—providing tangible proof of real economic value.

Semiconductors: The Biggest Winners of the AI Wave

Under the AI boom, semiconductors have emerged as the biggest beneficiaries.

Whether it’s OpenAI, Google, or Meta, large language models require massive GPU computation, reshaping the chip industry from cyclical to structurally growing.

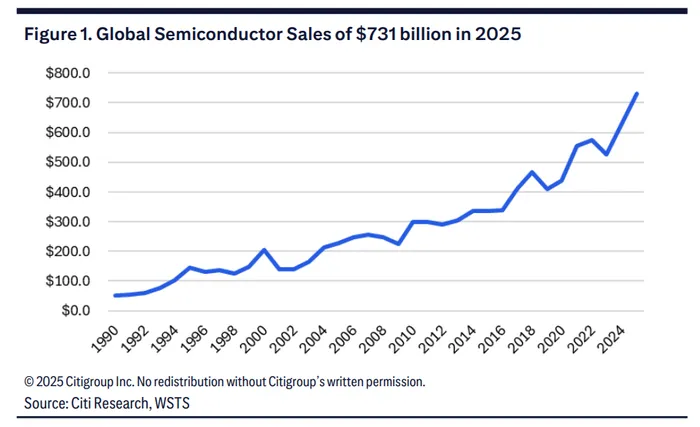

Citigroup analyst Christopher Danely projects global semiconductor sales to rise 16% in 2025 to a record $731 billion, entirely driven by price increases rather than shipment growth.

Inventory levels remain low, suggesting further upside.

The average semiconductor price has risen 75%, from about $0.72 in 2019 to $1.26 in 2025, with a 45% jump since 2022—the sharpest increase in 30 years. This marks the first four-year consecutive price upcycle since 1992–1995.

Citi expects AI data center chips to account for 27% of industry revenue by 2025, up from less than 5% in 2022, and to reach 40% by 2028. AI-driven demand could lift the industry’s long-term revenue growth rate from 7% to 10%.

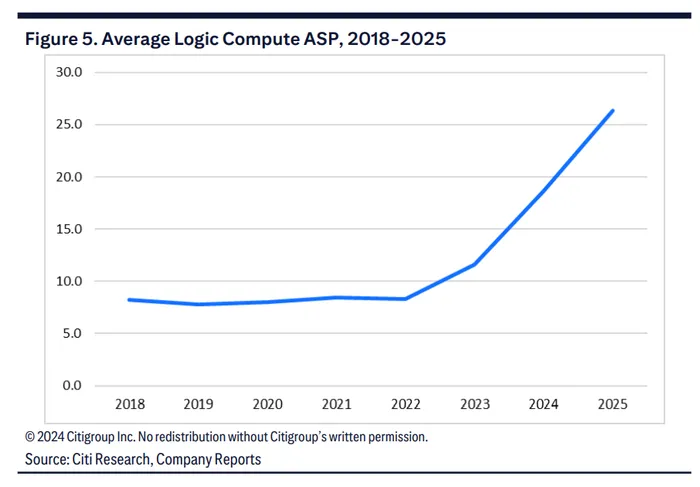

Most of this growth is powered by higher prices for logic chips (including AI accelerators).

Average selling prices have surged 24% in three years, far above the prior decade’s 2% pace, while logic chips’ share of total semiconductor sales will climb from 27% in 2020 to 39% in 2025.

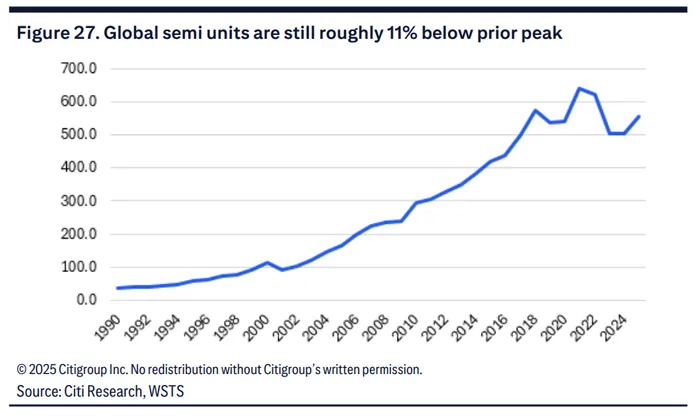

Despite the rally, total semiconductor shipments remain 11% below the previous peak, indicating ample room for expansion.

Citi notes that in an industry where unit growth typically reaches 50% peak-to-peak, the current 11% gap “gives us confidence this cycle still has room to run.”

Strong Margins Justify High Valuations

High margins at NVIDIA and Broadcom are exceptional, but the industry’s average gross margin is still only 52%, well below historical highs—leaving upside potential as Intel and AMD improve.

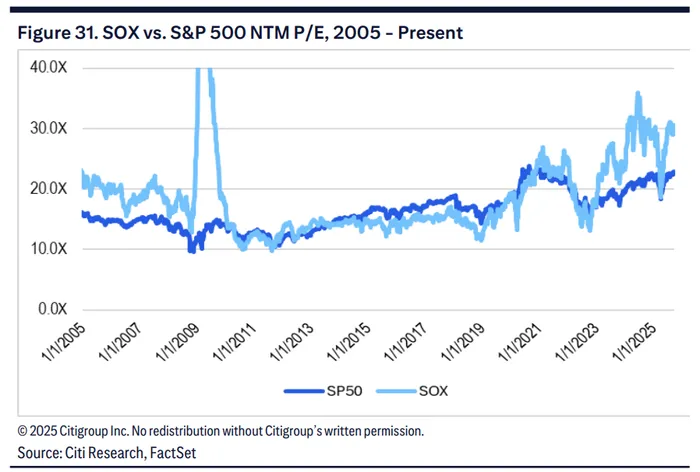

The Philadelphia Semiconductor Index (SOX) trades at 31× forward earnings, a 34% premium to the S&P 500, which Citi views as reasonable.

Since ChatGPT’s release in November 2022, SOX’s relative premium has averaged 31%.

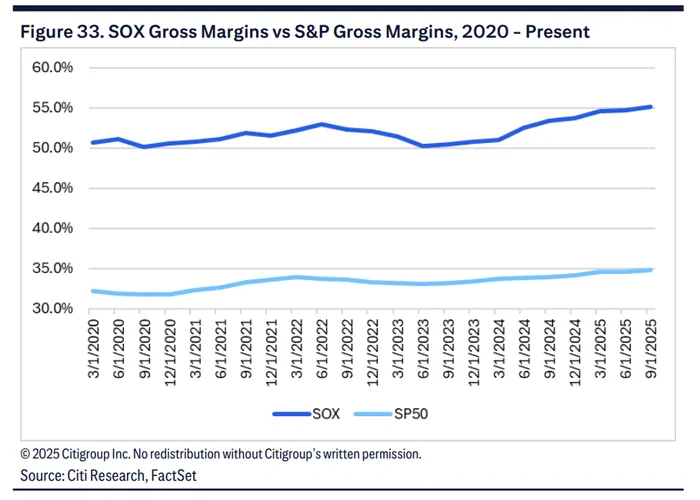

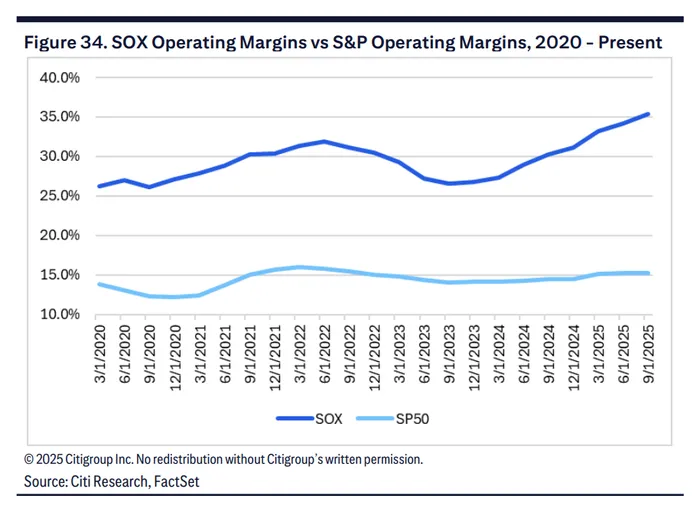

Citi highlights that the semiconductor sector’s gross margin (>50%) and operating margin (>25%) far exceed those of the S&P 500 (30–35% and 10–15%, respectively).

Growth rates across 3-year, 5-year, and 10-year horizons also outpace the broader market.

According to Goldman Sachs, the Nasdaq 100’s P/E remains 46% below its dot-com peak, and IPO activity is far lower, suggesting no imminent correction risk.

Beyond Chips: The Next Opportunity — Power

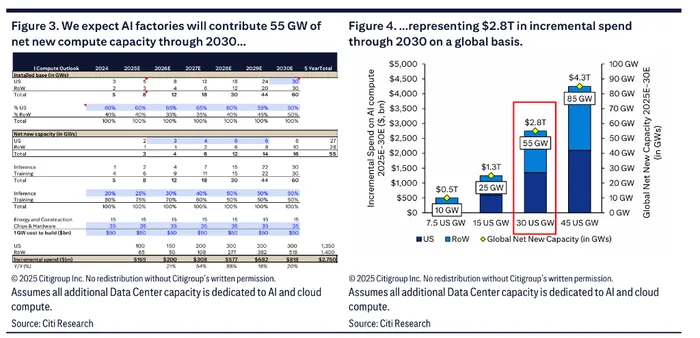

Citi analysts have sharply raised their forecasts for AI capital spending by tech giants, projecting $490 billion by 2026, up from $420 billion previously.

Cumulative AI-related CapEx through 2029 is now estimated at $2.8 trillion, up from $2.3 trillion.

Driven by AI infrastructure and data centers, global power capacity is expected to expand by 55 GW by 2030, translating into $2.8 trillion in additional AI compute investment—$1.4 trillion in the U.S. alone.

Goldman Sachs expects data center power demand to surge 165% by 2030 compared to 2023. In the U.S., 60% of future demand will require new generation facilities, adding roughly 72 GW in capacity—mainly from natural gas (60%), solar (25–30%), and wind (10–15%) sources.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.