Broadcom's AI Bet Falls Short, Sending Shares Tumbling Despite Beat

Broadcom Inc. has ridden the artificial intelligence wave with gusto, positioning itself as a formidable challenger to Nvidia Corp. in the lucrative chip market.

But on Thursday, the company's latest earnings report revealed the perils of sky-high investor expectations. Shares tumbled about 4% in after-hours trading, erasing earlier gains, as CEO Hock Tan's commentary on the AI backlog failed to ignite the enthusiasm Wall Street craved. Tan, the architect of Broadcom's aggressive pivot toward AI, described a $73 billion order backlog for AI products over the next six quarters—a figure he labeled a "minimum" amid lengthening lead times of six months to a year. Yet, for a stock that has surged 75% this year, closing at $406.37 before the report, the details felt like a letdown in an industry where billions are table stakes.

The Palo Alto-based chipmaker, with its sprawling portfolio from communications silicon to networking gear and software, has thrived on the data center boom. AI models' escalating complexity demands faster interconnections between chips, servers, and entire facilities—areas where BroadcomAVGO-- excels. Still, the post-earnings slide underscores a broader tension: as AI spending explodes, companies like Broadcom must deliver not just growth, but outsized leaps to justify their valuations.

Earnings Highlights: A Solid Beat Tempered by Margin Pressures

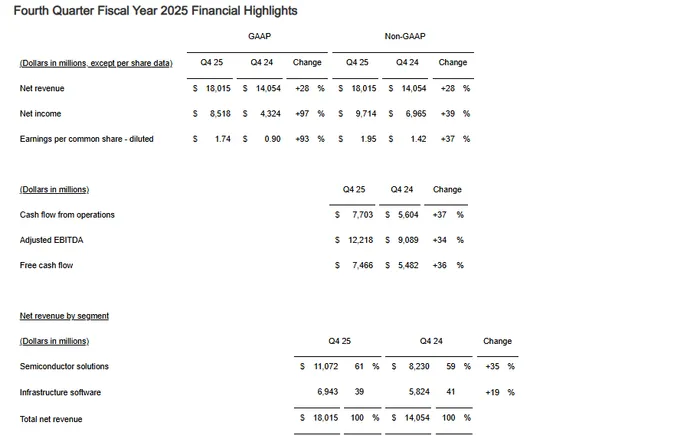

Broadcom's fiscal fourth quarter, ending November 2, delivered results that would envy most tech peers. Revenue climbed 28% year-over-year to $18.02 billion, surpassing the $17.49 billion analysts had anticipated, per LSEG data. Adjusted earnings per share hit $1.95, beating estimates of $1.86. Net income nearly doubled, soaring 97% to $8.51 billion, or $1.74 per share, from $4.32 billion a year earlier.

The semiconductor solutions segment, home to Broadcom's AI chips, grew 22% to $11.07 billion, topping StreetAccount's $10.77 billion forecast. AI chip sales within this unit jumped 74%, equating to $8.2 billion for the quarter—a testament to the company's custom accelerators and networking prowess. Meanwhile, the infrastructure software arm, bolstered by VMware acquisitions, expanded 26% to $6.94 billion, exceeding expectations.

Looking ahead, Broadcom projected first-quarter revenue of about $19.1 billion, implying 28% growth and outpacing the $18.3 billion consensus. The company also sweetened its appeal to shareholders with a 10% dividend hike to 65 cents per share, payable later this month. These figures paint a picture of robust health, yet Tan's warnings about narrowing profit margins—driven by the high costs of AI product ramps—cast a shadow. "It's a moving target," Tan said of the AI landscape, declining to offer a 2026 revenue forecast despite analyst prodding.

AI Outlook: Doubling Down Amid Investor Scrutiny

At the heart of Broadcom's narrative is its AI trajectory, where revenue is set to double to $8.2 billion in the current quarter from a year ago. This surge stems from custom AI chips—dubbed XPUs—and semiconductors tailored for AI networking. Tan emphasized the company's role in the massive data center expansion, where its designs underpin hyperscalers' ambitions.

Yet, the $73 billion backlog, spanning custom chips, switches, and other AI data center components over the next 18 months, drew mixed reactions. Tan positioned it as a floor, noting that additional orders could swell the pipeline as lead times extend. "We do expect much more," he assured analysts, highlighting the fluidity of demand in this nascent market.

Broadcom's reluctance to pinpoint future AI sales reflects the sector's volatility. AI models are evolving rapidly, requiring ever-faster data movement—a boon for Broadcom's updated networking equipment. But with profit margins compressing under the weight of these investments, investors are left pondering the sustainability of the growth spurt.

Customer Wins: From Anthropic to OpenAI, Partnerships Fuel Momentum

Broadcom's AI credentials shine through its marquee deals. In the fourth quarter, the company secured an $11 billion order from AI startup Anthropic PBC, following a $10 billion commitment in the third quarter. Anthropic, leveraging Google's latest Ironwood TPUs—which incorporate Broadcom designs—represents a deepening entanglement with cloud giants like Alphabet Inc.

Tan also disclosed a fifth custom chip customer, unnamed but with a $1 billion order slated for delivery in late 2026. This builds on a June tally of three customers and four prospects, evolving to include a fourth mystery buyer by September. The October pact with OpenAI, the force behind ChatGPT, stands out: Broadcom will supply custom chips and networking components to power OpenAI's AI services, granting deeper market penetration.

These alliances position Broadcom as a key enabler in the AI arms race. Google's TPUs, increasingly adopted as Nvidia alternatives, rely on Broadcom's innovations, while OpenAI's shift toward proprietary silicon underscores a trend among AI leaders to "control their own destiny," as Tan put it. With Anthropic now identified as the prior $10 billion TPU buyer, investors gain clarity on Broadcom's expanding roster, even as some crave more specifics on deployment timelines.

Challenges Ahead: Balancing Growth and Expectations

Despite the triumphs, Broadcom operates in Nvidia's long shadow, where the latter dominates AI processors. Broadcom's custom chip unit has seen revenue climb, but the company must navigate intensifying competition and supply chain strains. Tan's performance-linked incentives—a potential 610,521 shares if AI revenue reaches $90 billion by fiscal 2030, scaling to 300% at $120 billion—align his fortunes with shareholders, yet they amplify the pressure to deliver.

The margin squeeze from AI sales highlights a trade-off: explosive top-line growth at the expense of profitability. As data centers scale, Broadcom's ability to innovate in connectivity will be crucial, but any hiccup in order fulfillment could exacerbate volatility.

In a year where Broadcom shares have outperformed amid AI fervor—doubling last year and up 75% in 2025—the earnings reaction serves as a reality check. Investors, primed for disappointment after a 170% rally in recent memory, are demanding proof that Broadcom's AI payoff will match the hype.

Looking Forward: Can Broadcom Soldier through the Tough Time?

As Hock Tan steers Broadcom through this transformative era, the company stands at a crossroads. With a fortified dividend, beating forecasts, and a swelling AI backlog, the fundamentals remain strong. Yet, the stock's dip signals that in the high-stakes AI arena, even solid progress can feel insufficient.

Broadcom's partnerships with OpenAI, Anthropic, and Google position it as an indispensable player, but sustaining momentum will require navigating margin pressures and delivering on those multibillion-dollar promises. For now, Tan's cautious optimism—"I'd rather not give you guys any guidance"—leaves room for upside, but also for skepticism. In an industry where fortunes pivot on the next breakthrough, Broadcom's journey from AI contender to leader hangs in the balance.

Rodder Shi is a market analyst covering U.S. stocks and prediction markets. He holds a Master’s degree in Financial Engineering from UCLA and dual degrees from UC San Diego, with research experience at CICC and Rayliant. An IAQF quantitative research award winner, he has over six years of equity and options investing experience focused on data-driven and risk-aware market analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet