BRO Stock Trading at a Discount to Industry at 13.6X: Time to Hold?

Brown & Brown, Inc. BRO shares are trading at a discount compared with the Zacks Brokerage Insurance industry. Its forward price-to-earnings multiple of 13.6X is lower than the industry average of 14.54X, the Finance sector’s 14.8X and the Zacks S&P 500 Composite’s 19.99X.

The insurer has a market capitalization of $21.59 billion. The average volume of shares traded in the last three months was 3.2 million.

Shares of other insurers like Aon plc. AON and Arthur J. Gallagher & Co. AJG are trading at a multiple higher than the industry average, while Willis Towers Watson Public Limited Company WTW is trading at a discount.

Image Source: Zacks Investment Research

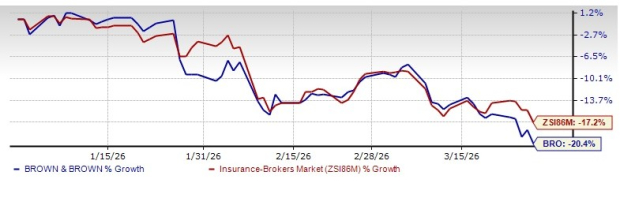

Shares of Brown & BrownBRO-- have lost 20.4% year to date compared with the industry’s decline of 17.2%.

Image Source: Zacks Investment Research

BRO’s Encouraging Growth Projection

The Zacks Consensus Estimate for Brown & Brown’s 2026 earnings per share (EPS) indicates a year-over-year increase of 7%. The consensus estimate for revenues is pegged at $7.28 billion, implying a year-over-year improvement of 23.3%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 9.3% and 5.9%, respectively, from the corresponding 2026 estimates.

Earnings have grown 19.2% in the past five years, better than the industry average of 13.9%. Brown & Brown's bottom line outpaced estimates in three of the trailing four quarters and missed in one, the average surprise being 5.54%.

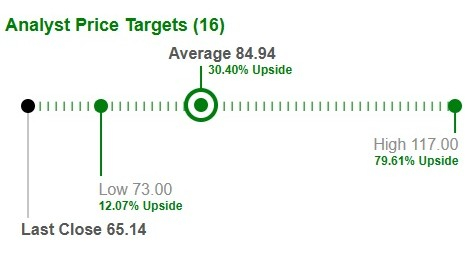

Average Target Price for BROBRO-- Suggests Upside

Based on short-term price targets offered by 16 analysts, the Zacks average price target is $84.94 per share. The average suggests a potential 30.4% upside from the last closing price.

Image Source: Zacks Investment Research

Factors Impacting BRO

Commissions and fees, the main component of the top line, benefit from increasing new business, strong retention and continued rate increases for most lines of coverage. The company met its intermediate annual revenue goal of $4 billion, doubling in the last five years.

The insurance broker continually makes investments in boosting organic growth and margin expansion. It has an industry-leading adjusted EBITDAC margin.

Brown & Brown’s strategic buyouts help it capitalize on growing market opportunities, strengthen its compelling products and service portfolio, expand global reach and accelerate its growth rate. From 1993 through the fourth quarter of 2025, Brown & Brown acquired 717 insurance intermediary operations. The Quintes buyout was the largest transaction in 2024.

Banking on operational expertise, BRO boasts a strong liquidity position with an improving leverage ratio. The strength of its operating model and diversity of businesses ensures strong cash conversion. The company effectively deploys cash into acquisitions, capital expenditure and wealth distribution for shareholders via dividend increases.

BRO has an impressive dividend history. The strong capital position enables Brown & Brown to distribute wealth to shareholders via dividend increases. For dividend payments, the company has increased dividends for the last 30 years at a five-year (2019-2024) CAGR of 8.7%.

Headwinds

However, the company’s international expansion to the United Kingdom, Bermuda and the Cayman Islands introduces additional complexities. Exposure to regulatory changes, currency fluctuations and varying economic conditions, coupled with heightened competition for quality business, could pressure margins and operational efficiency.

Profitability metrics also lag industry levels. Brown & Brown’s return on equity is 12.9%, well below the industry average of 19.1%. Return on invested capital was 6.5% versus the industry’s 7.5%, pointing to inefficiencies in utilizing shareholder funds.

Conclusion

New business, strong retention, rate increases, strategic buyouts and impressive dividend history position the company well for growth. Favorable growth estimates and positive analyst sentiment are other positives. A robust capital position over the years reflects its financial flexibility.

However, international expansion risks, regulatory headwinds and profitability pressures may temper its near-term performance.

Given the balanced mix of strengths and headwinds, it is, therefore, wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aon plc (AON): Free Stock Analysis Report

Arthur J. Gallagher & Co. (AJG): Free Stock Analysis Report

Brown & Brown, Inc. (BRO): Free Stock Analysis Report

Willis Towers Watson Public Limited Company (WTW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet