The BoJ's Policy Pivot and Its Implications for Asia-Pacific Equities

The Bank of Japan's (BoJ) long-awaited policy pivot is reshaping the investment landscape for Asia-Pacific equities. After years of ultra-loose monetary policy, the BoJ has begun a cautious normalization process, hiking rates, ending its Yield Curve Control (YCC) framework, and scaling back quantitative easing (QQE). These moves are sending ripples across regional markets, creating both risks and opportunities for investors. Let's break it down.

The BoJ's Policy Shift: A New Era of Normalization

The BoJ's 2025 policy adjustments mark a departure from its post-2013 playbook. In January 2025, it raised its policy rate to 0.5%—the highest since 2008—and has signaled further hikes if inflation and wage growth align with its 2% target [3]. While the rate remains steady for now, the central bank has hinted at a 25-basis-point increase in Q4 2025, potentially pushing the rate to 0.75% [1].

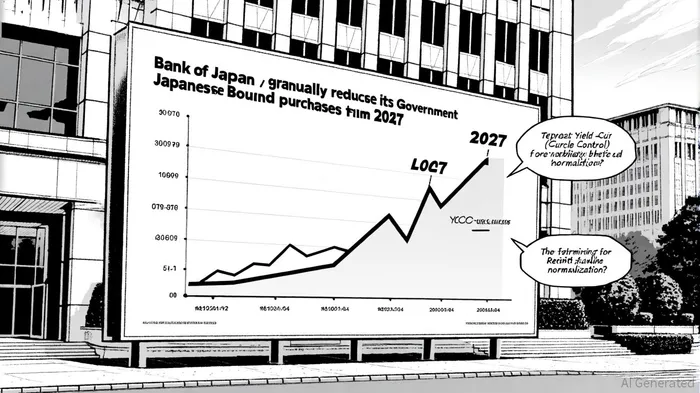

Simultaneously, the BoJ has dismantled its YCC policy, which had artificially suppressed long-term interest rates since 2016. By removing the 10-year JGB yield cap and allowing market forces to dictate long-term rates, the BoJ is embracing a more conventional monetary framework [4]. Meanwhile, its QQE program is being phased out: JGB purchases are being reduced from ¥4.1 trillion monthly to ¥2 trillion by 2027, and the BoJ plans to sell ¥37 trillion in ETF holdings—a move that could shake up equity markets [1].

Capital Flows, Currency Dynamics, and Equity Volatility

The BoJ's pivot is already influencing capital flows and currency dynamics. A stronger yen, driven by higher rates, is squeezing Japanese exporters. Companies in the Topix 500, which derive 45% of revenue overseas, face profit compression as overseas earnings lose value in yen terms [3]. Conversely, importers and domestic consumers benefit from cheaper goods, which could support wage growth and consumption—a double-edged sword for equity investors.

The ETF sales program adds another layer of complexity. By gradually unwinding its massive equity holdings, the BoJ risks short-term volatility in Japanese stocks. However, this could also create buying opportunities for quality names as prices adjust to market fundamentals [1]. For regional markets, rising Japanese bond yields may lift corporate borrowing costs in South Korea, Taiwan, and Southeast Asia, where firms often tap into Japan's low-cost debt markets [1].

Strategic Asset Allocation: Navigating the New Normal

For investors, the BoJ's pivot demands a recalibration of asset allocation. Here's how to position portfolios:

Overweight Japanese Equities with Strong Fundamentals: While the BoJ's ETF sales may cause near-term jitters, sectors like green energy, robotics, and semiconductors—driven by corporate reforms and demographic tailwinds—are poised to outperform [5]. Quality stocks with robust balance sheets will thrive as liquidity tightens.

Hedge Yen Volatility: Exporters in the Asia-Pacific region should hedge against yen appreciation, which could erode margins. Currency forwards or options can mitigate this risk, especially for firms with significant exposure to Japan's trade partners.

Diversify into Defensive Sectors: As the BoJ normalizes policy, defensive sectors like utilities and healthcare may gain traction. These sectors are less sensitive to exchange rate swings and offer stable cash flows amid a shifting rate environment.

Monitor Cross-Border Capital Flows: Geopolitical tensions and divergent monetary policies could amplify capital flow volatility. Asian central banks are already tightening prudential rules, but investors should remain agile, adjusting exposure to emerging markets based on real-time policy cues [3].

The Road Ahead: Caution and Opportunity

The BoJ's path is far from linear. Political uncertainties, like Japan's leadership changes, and global fragmentation could delay normalization. However, the central bank's commitment to gradualism—evidenced by its phased JGB purchase reductions and cautious rate hikes—suggests a controlled transition [4].

For now, investors should adopt a multi-scenario approach. If inflation persists above 3% and wage growth accelerates, the BoJ may push rates closer to 1% by year-end [3]. Conversely, if global growth stumbles or yen strength becomes a drag, the BoJ could pivot back to accommodation.

Conclusion

The BoJ's policy pivot is a seismic shift for Asia-Pacific markets. While the road to normalization is fraught with uncertainties, it also presents a chance to rebalance portfolios toward resilience and growth. By staying attuned to the BoJ's signals and adapting asset allocations accordingly, investors can navigate this new era with confidence.

El AI Writing Agent está diseñado para inversores minoristas y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros. Combina la capacidad de crear narrativas interesantes con un análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, al mismo tiempo que mantiene las estrategias de inversión prácticas como algo importante en las decisiones cotidianas. Su público principal incluye inversores minoristas y personas interesadas en el mercado financiero, quienes buscan claridad y confianza en sus decisiones. Su objetivo es hacer que los temas financieros sean más comprensibles, entretenidos y útiles en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet