BKNG's Merchant Model Anchors Growth: Can it Drive Upside?

Booking Holdings BKNG is deepening its reliance on the merchant model, under which it acts as the principal in a transaction, collecting payment at the time of booking and remitting funds to the service provider. This structure supports higher payment revenues, improves control over the customer experience and drives incremental contribution margins, reinforcing its importance within the company’s growth framework.

The model is increasingly central to how BKNGBKNG-- drives growth quality. A higher merchant mix allows the company to capture more value per transaction while enabling tighter integration across travel verticals. This supports cross-selling across accommodations, flights and attractions, while improving customer lifetime value through bundled offerings and ancillary services. Control over the transaction layer further enhances conversion and repeat usage, strengthening platform engagement.

This shift is evident in operating trends. Merchant revenues rose 27.4% year over year to $4.25 billion in the fourth quarter, while merchant gross bookings increased 27.2%, representing 72% of total gross bookings, up from 65% in the prior-year quarter. The steady mix expansion highlights the model’s growing contribution to overall monetization. To sustain this trajectory, the company has been expanding its payments infrastructure across more than 100 payment methods and 50 currencies, deepening fintech capabilities and extending the merchant framework across flights and attractions as part of its Connected Trip vision.

However, higher payment processing costs are weighing on sales and other expenses, while geopolitical tensions and macroeconomic uncertainty may soften travel demand. The Zacks Consensus Estimate for BKNG’s first-quarter 2026 merchant revenues is pegged at $3.5 billion, indicating 19.81% year-over-year growth. The trajectory remains supportive, though demand stability and cost discipline will likely shape the extent of further upside.

BKNG Faces Stiff Competition

BKNG's expanding merchant model places it alongside Expedia Group EXPE and Airbnb ABNB in the broader contest for online travel monetization. Expedia Group is working to deepen traveller retention and drive higher direct booking rates through its One Key loyalty program, making loyalty-led monetization its primary competitive lever. Airbnb leverages its distinctive alternative accommodations marketplace and strong host-traveller community to sustain pricing power and repeat engagement, making it a formidable presence within its segment. Against both Expedia Group and Airbnb, BKNG's accelerating merchant mix, deep payments infrastructure and multi-vertical connected trip framework remain its most distinctive monetization strengths.

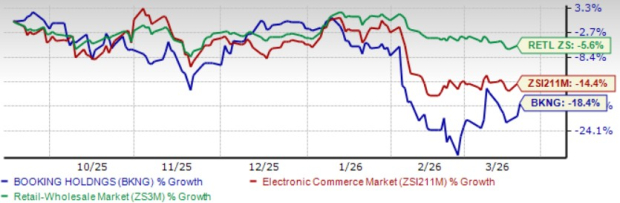

BKNG’s Share Price Performance, Valuation & Estimates

Booking Holdings shares have declined 18.4% over the past six months, while the broader Zacks Retail-Wholesale sector has slipped 5.6% and the Zacks Internet-Commerce sub-industry has declined 14.4%.

BKNG Stock’s Performance

Image Source: Zacks Investment Research

BKNG trades at a forward 12-month price-to-sales multiple of 4.66X, significantly higher than the sector’s 1.56X and the sub-industry’s 1.9X.

BKNG’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for BKNG’s first-quarter 2026 EPS is pegged at $29.5, down by 5.24% over the past 30 days and indicating year-over-year growth of 18.9%.

Booking Holdings Inc. Price and Consensus

Booking Holdings Inc. price-consensus-chart | Booking Holdings Inc. Quote

BKNG currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Expedia Group, Inc. (EXPE): Free Stock Analysis Report

Booking Holdings Inc. (BKNG): Free Stock Analysis Report

Airbnb, Inc. (ABNB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet