BJ's Wholesale Q4 Earnings on Horizon: Is Another Beat in the Cards?

BJ's Wholesale Club Holdings, Inc. BJ is likely to register an increase in the top line when it reports fourth-quarter fiscal 2025 results on March 5, before the opening bell. The Zacks Consensus Estimate for revenues stands at $5.61 billion, calling for a 6.2% increase from the prior-year reported figure.

The Zacks Consensus Estimate for quarterly earnings has inched up by a penny over the past seven days to 93 cents per share, indicating flat year-over-year growth.

BJ's Wholesale has a trailing four-quarter earnings surprise of 10.3%, on average. In the last reported quarter, this Marlborough, MA-based company’s bottom line surpassed the Zacks Consensus Estimate by a margin of 5.5%.

Image Source: Zacks Investment Research

What’s Shaping BJ’s Wholesale’s Upcoming Earnings?

BJ's Wholesale Club's fourth-quarter results are likely to benefit from the continued strength of its membership-based business model. Higher member engagement, increasing penetration of premium tiers, and solid renewal trends provide a dependable stream of recurring revenues that supports traffic and merchandise sales. This dynamic becomes more visible in softer consumer environments, as households shift toward value-oriented shopping.

As BJ's enhances its value positioning and expands through new club openings, demand across core consumables and perishables categories is expected to remain steady. The company has been refining assortments, improving in-stock levels and enhancing quality across key traffic-driving departments. Ongoing investments under the Fresh 2.0 initiative, coupled with sharper pricing and improved merchandising execution, have strengthened its competitive position in categories such as fresh meat, dairy and produce. We expect merchandise comparable club sales to increase 2% for the quarter.

Digital momentum is also likely to have provided an additional tailwind in the fourth quarter. Growth in same-day services, in-club fulfillment and mobile-enabled shopping continues to deepen member engagement. Digitally active members typically generate larger baskets and shop more frequently than store-only customers. BJ’s emphasis on convenience through pickup options, delivery partnerships and app-based checkout is likely to have supported incremental traffic and comparable sales.

That said, elevated SG&A expenses tied to labor, advertising and occupancy costs associated with new club openings may have pressured margins. We anticipate SG&A expenses to increase 5.6% year over year in the fourth quarter, resulting in a modest 10-basis-point contraction in the operating margin.

What the Zacks Model Predicts for BJ

As investors prepare for BJ's fourth-quarter announcement, the question looms regarding earnings beat or miss.

Our proven model predicts that an earnings beat is likely for BJ's WholesaleBJ-- this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

BJ's Wholesale has an Earnings ESP of +5.69% and carries a Zacks Rank #2. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

BJ's Wholesale Club Holdings, Inc. Price, Consensus and EPS Surprise

BJ's Wholesale Club Holdings, Inc. price-consensus-eps-surprise-chart | BJ's Wholesale Club Holdings, Inc. Quote

BJ Stock Price Performance

Shares of BJ's Wholesale ClubBJ-- have advanced 7.3% over the past three months, underperforming the industry’s 13.4% rise.

BJ stock has held up far better than Albertsons Companies, Inc. ACI, though it has lagged Walmart Inc. WMT and Costco Wholesale Corporation COST. Over the same period, Walmart and Costco shares have risen 11.8% and 9.6%, respectively, while Albertsons has slipped 0.2%.

Image Source: Zacks Investment Research

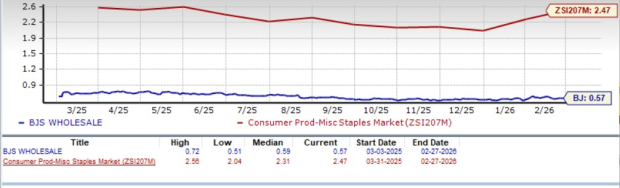

Does BJBJ-- Present a Strong Case for Value Investing?

Despite the recent jump in the stock price, BJ's Wholesale Club still looks inexpensive versus the industry on a valuation basis. BJ currently trades at a forward 12-month price-to-sales (P/S) multiple of 0.57, which positions it at a discount compared to the industry’s average of 2.47. At the same time, BJ is trading below its 12-month median P/S of 0.59X.

BJ is trading at a premium to Albertsons Companies (with a forward 12-month P/S ratio of 0.11), but at a discount to Walmart (1.36) and Costco (1.46).

Image Source: Zacks Investment Research

Final Words on BJ

BJ’s Wholesale appears well-positioned heading into its fourth-quarter release, supported by resilient membership trends, steady comparable sales growth and continued digital traction, which together raise the probability of another earnings beat. While margin pressures from higher operating costs remain a factor to watch, the company’s value-focused model and consistent execution provide a favorable backdrop relative to peers. Given the supportive earnings setup and reasonable valuation, existing investors may consider maintaining their positions ahead of the report, while prospective investors could look to build exposure on any pre- or post-earnings volatility.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT): Free Stock Analysis Report

Albertsons Companies, Inc. (ACI): Free Stock Analysis Report

BJ's Wholesale Club Holdings, Inc. (BJ): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet