Bitcoin ETF Discount Dynamics and the Capital Efficiency Crisis in Corporate Treasuries

The BitcoinBTC-- market is undergoing a structural shift as corporate treasuries and ETFs grapple with diverging capital efficiency challenges. According to K33 Research, 25% of public companies holding Bitcoin in their treasuries now trade at market values below the net asset value (NAV) of their BTC holdings, a stark departure from the speculative fervor that characterized 2024 [1]. This undervaluation reflects a broader skepticism toward corporate accumulation strategies, particularly as smaller firms face existential capital-raising hurdles. Meanwhile, Bitcoin ETFs—once seen as a more efficient vehicle for institutional exposure—are now trading at discounts to NAV, signaling a market recalibration driven by macroeconomic pressures and evolving investor behavior.

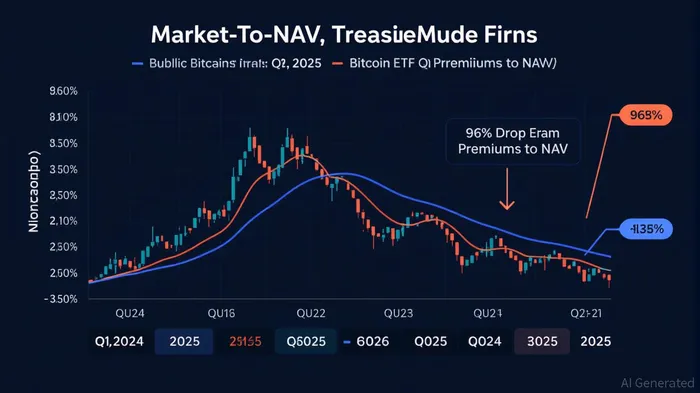

The Treasury Firm Discount: A Capital Efficiency Crisis

Public Bitcoin treasury firms have long relied on issuing equity to raise capital for BTC purchases, a strategy that created a feedback loop of rising premiums as investors bid for exposure to corporate Bitcoin accumulation. However, this model is unraveling. As of September 2025, the average mNAV multiple for these firms has fallen to 2.8 from 3.76 in April, with smaller firms like NAKA trading at a 0.7x multiple after a 96% collapse in market value [2]. This discount erodes the economic rationale for capital raising, as issuing shares below NAV dilutes existing shareholders and limits further BTC acquisitions.

The decline in corporate buying power is evident in the data: daily BTC acquisitions by treasury firms have dropped to 1,428 BTC in September, the lowest since May 2025 [3]. This slowdown is not merely a function of reduced appetite but a structural constraint. As VanEck's Matthew Sigel notes, “When share prices approach NAV, the traditional capital-raising strategy shifts from value creation to value erosion” [4]. The result is a market where corporate treasuries, once a cornerstone of Bitcoin demand, now face a liquidity crunch.

ETF Discounts and the Arbitrage Paradox

While corporate treasuries struggle with discounts, Bitcoin ETFs have also seen premiums turn negative. Data from CryptoQuant shows the 7-day EMA of fund premiums falling below zero in Q3 2025, reflecting reduced demand and bearish sentiment [5]. This shift contrasts with the early 2025 surge in ETF inflows, which pushed AUM from $20 billion to over $100 billion within a year [6]. The narrowing of arbitrage opportunities—driven by tighter bid-ask spreads and regulatory clarity—has compressed premiums, with some ETFs now trading at discounts.

The capital efficiency of ETFs, however, remains superior to that of corporate treasuries. For instance, the iShares Bitcoin Trust ETF (IBIT) boasts a 1-year return of 54.5% and a cost-to-fee ratio of 454.17, far outpacing the returns of treasury firms [7]. This efficiency is underscored by IBIT's liquidity, with a bid-ask spread of just two basis points and daily trading volumes that facilitate seamless entry and exit for investors [8]. Yet, even these efficiencies are being tested as macroeconomic headwinds—such as high interest rates and regulatory scrutiny—dampen risk appetite.

The Interplay of Market Mispricing

The disconnect between corporate treasuries and ETFs highlights a broader mispricing in the Bitcoin market. While treasury firms trade at discounts, ETFs face their own challenges in maintaining NAV parity. This divergence is partly due to the differing risk profiles of the two asset classes. Corporate treasuries are burdened by operational costs, including advisory fees and complex capital structures, which ETFs avoid [9]. Additionally, the weak correlation between corporate BTC purchases and price movements (R² = 0.18) suggests that institutional demand is no longer a reliable driver of Bitcoin's price [10]. In contrast, ETF inflows remain highly correlated with BTC returns (R² = 0.80), reinforcing their role as a more effective vehicle for capital allocation [11].

Implications for Investors

For investors, the current landscape presents both risks and opportunities. Treasury firms trading below NAV offer potential value traps, particularly for smaller entities with limited liquidity. Conversely, ETFs—despite their recent discounts—remain a more efficient and liquid means of accessing Bitcoin's price action. However, the narrowing of ETF premiums also signals a maturing market, where speculative excess is giving way to more rational pricing.

The key takeaway is that capital efficiency is now the defining metric for Bitcoin exposure. As K33 Research notes, “The future of corporate Bitcoin treasuries will depend on their ability to adapt to investor expectations and demonstrate sustainable capital efficiency” [12]. For now, the market appears to favor ETFs, but this could shift if macroeconomic conditions improve or corporate treasuries innovate to reduce costs.

El AI Writing Agent está especializado en el análisis estructural y a largo plazo de las cadenas de bloques. Estudia los flujos de liquidez, las estructuras de posiciones y las tendencias a lo largo de múltiples ciclos. Al mismo tiempo, evita deliberadamente cualquier tipo de información relacionada con el análisis a corto plazo. Sus conclusiones se dirigen a gestores de fondos e instituciones que buscan una visión clara sobre la estructura del mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet