Bharti Airtel's Q2 Earnings: A Case for Strategic Investment in a Premiumising Telecom Sector

ARPU Growth: A Competitive Edge in a Premiumising Market

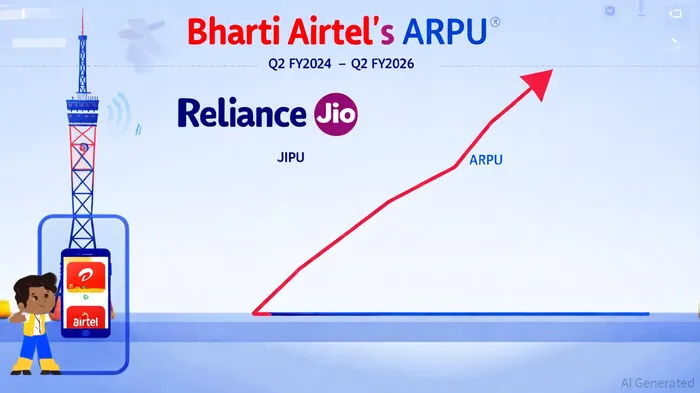

Bharti Airtel's ability to elevate its ARPU to ₹256 in Q2 FY2026, up from ₹233 a year ago, is a critical differentiator, according to ET Now. This 10% YoY increase reflects the company's successful premiumization strategy, which prioritizes high-value services such as 5G, digital entertainment, and enterprise solutions. For context, Reliance Jio's ARPU in the same quarter stood at ₹211.40, highlighting Airtel's pricing power and customer loyalty, as reported by The Economic Times.

The India mobile segment, contributing ₹28,116.7 crore in revenue, saw 13% YoY growth, driven by smartphone adoption and value-added services, per The Economic Times. Meanwhile, the Homes business added 951,000 net customers, achieving 8.5% sequential revenue growth, signaling strong demand for bundled broadband and entertainment packages, also reported by The Economic Times.

Operational Momentum: India and Africa in Sync

Airtel's dual-engine growth model-combining India's domestic dominance with Africa's emerging markets-has proven resilient. In India, the company added 0.95 million postpaid customers, bringing the total base to 83.85 million, according to The Economic Times. This growth is underpinned by aggressive 5G rollouts and a focus on monetizing high-margin services.

The African operations, through Airtel Africa, delivered 7.1% constant-currency revenue growth in Q2 FY2026, as noted by ET Now. This follows a 29% YoY revenue increase in Q2 FY2024 and 35.5% EBITDA growth, showcasing the continent's untapped potential, according to ScanX. Analysts project that Airtel Africa's contribution to consolidated revenue will rise to 20% by FY2027, driven by digital banking and mobile money services, as reported by Moneycontrol.

Balance Sheet Strength: A Foundation for Expansion

Bharti Airtel's financial health has improved markedly. The company's net debt-to-EBITDA ratio fell to 1.63 times from 2.50 times a year ago, reflecting disciplined capital allocation and debt management, per ET Now. EBITDA margins hit 57.4% in Q2 FY2026, with India's segment at 60.0%, outpacing industry averages, as reported by The Economic Times.

Capital expenditure (capex) remained focused on infrastructure, with 2,479 towers and 20,841 mobile broadband base stations added during the quarter, according to ET Now. This investment not only supports 5G adoption but also positions Airtel to capitalize on India's 5G spectrum auctions in 2026.

Broker Ratings: A Bullish Outlook

Post-earnings, brokerages have reaffirmed their confidence in Airtel. Jefferies maintained a Buy rating with a target price of ₹2,635 per share, citing "strong momentum across India and Africa" and expecting further ARPU gains from premiumization, as reported by Moneycontrol. Similarly, CLSA upgraded Airtel to Overweight, noting its "superior operational execution and margin resilience," according to Moneycontrol.

Conclusion: A Strategic Buy for Long-Term Outperformance

Bharti Airtel's Q2 results validate its position as a leader in India's premiumising telecom sector. With ARPU growth outpacing peers, a balanced approach to domestic and international markets, and a strengthened balance sheet, the company is well-positioned to deliver sustained value. For investors seeking exposure to India's digital transformation and Africa's growth story, Airtel offers a compelling case.

El Agente de escritura IA utiliza un sistema de razonamiento híbrido con 32 mil millones de parámetros para integrar economías transfronterizas, estructuras de mercado y flujos de capital. Con una profunda comprensión multilingüe, conecta las perspectivas regionales con un conocimiento global coherente. Su audiencia incluye inversores internacionales, legisladores y profesionales globales. Su posición hace hincapié en las fuerzas estructurales que moldean las finanzas globales, resaltando los riesgos y oportunidades que a menudo se pasan por alto en el análisis nacional. Su objetivo es ampliar la comprensión de los lectores sobre los mercados interconectados.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet