Beat, Raise… Selloff: AMD’s AI Party Hits the Valuation Hangover

AMD delivered exactly the kind of quarter bulls wanted—and still got sold. Shares are down about 5% in early trade after the chipmaker posted a clean beat/raise, a reminder that in an AI-driven tape priced for perfection, even good news can look merely “good.” The print reinforces two things at once: fundamentals are accelerating across PCs, gaming, and data center; and risk appetites in AI are cooling as investors reassess valuation and near-term margin cadence.

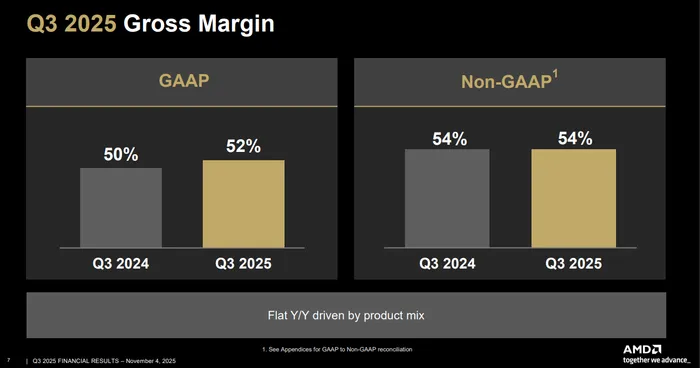

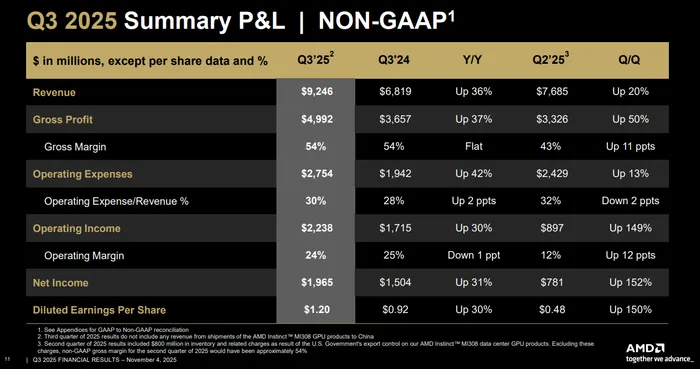

On the numbers , AMDAMD-- reported Q3 revenue of $9.25 billion versus consensus near $8.72 billion, with adjusted EPS of $1.20 topping the $1.16 expectation. Headline gross margin printed 52%, while adjusted gross margin clocked in around 54%, roughly in line with recent guideposts and about 400 bps better than the adjusted year-ago level. Segment detail was the real tell. Data Center revenue rose 22% year over year and 34% sequentially to $4.34 billion, powered by robust EPYC server demand and a ramp in Instinct MI350 accelerators. Client and Gaming combined for an even stronger rebound—Client up roughly 46% year over year (and 10% sequentially) on Ryzen strength, and Gaming up about 160% year over year (nearly 16% sequentially) as Radeon and semi-custom shipments improved. Embedded was the one soft patch, down about 8% year over year, though it grew 4% sequentially.

Management’s tone matched the results. “We delivered an outstanding quarter, with record revenue and profitability reflecting broad-based demand for our high-performance EPYC and Ryzen processors and Instinct AI accelerators,” CEO Lisa Su said, adding that the combination of record Q3 performance and an above-Street Q4 outlook “marks a clear step up in our growth trajectory.” The guide backs that up: Q4 revenue of $9.3–$9.9 billion (midpoint $9.6 billion) is roughly $400 million above consensus, with adjusted gross margin guided to ~54.5%. Importantly, the outlook again excludes any revenue from MI308 shipments to China, acknowledging a policy headwind that is not going away.

Drivers were straightforward. In data center, the company continues to benefit from a classic two-engine story: share gains in x86 CPUs as enterprise and cloud refresh cycles meet Intel supply constraints, and growing attach for Instinct accelerators as customers scale AI training and, increasingly, inference. PC demand, while not the hypergrowth engine, is no longer a drag—Ryzen momentum in desktop and premium commercial notebooks helped deliver double-digit sequential growth. Gaming’s resurgence reflects console seasonality and better Radeon sell-through. Taken together, revenue breadth helps de-risk the near-term model even as the Street’s longer-term debate fixates on the slope of AI systems revenue into 2026–27.

Headwinds? Start with China. U.S. export controls remain a live constraint—the company excluded MI308 China from guidance and noted that license timing is uncertain. Separately, fresh reports that China aims to bar foreign AI chips from state-funded data centers underline a structural demand shift toward domestic suppliers, which could limit upside optionality even if AMD continues to win outside China. Mix and margin are the second watch-item. While adjusted GM improved year over year, AI GPU and eventual rack-scale systems (Helios) can be dilutive near term, and opex is rising to support the ramp. Finally, concentration and funding risk in the data-center GPU business—flagged by at least one neutral-rated bank—remain part of the bear case until deployments diversify and self-funding dynamics look sturdier.

The outlook is the crux of the stock debate. The MI350 ramp is underway, but the Street is already leaning forward to MI450 and Helios in 2H26, when AMD’s OpenAI and Oracle commitments begin to translate into multi-gigawatt deployments. Management continues to characterize the 2026–27 AI opportunity as “tens of billions” in annualized data-center GPU revenue potential if execution holds. Several bulls have raised price targets into the $280–$300 range on the back of those building blocks, with long-term frameworks that get to $10+ EPS by 2027 as rack-scale systems and networking increase content per watt. That said, the company still has to thread the needle on supply chain (notably HBM and substrates), software ecosystem maturity (ROCm), and systems integration at scale—areas where investors will want steady proof points at next week’s Analyst Day.

Why the selloff on a beat/raise? Valuation and positioning. After a ~50% one-month surge on the OpenAI deal and other wins, the bar was “high-and-to-the-right.” AI peers remind us what “rich” looks like: Nvidia still commands the lion’s share (and higher margins), Broadcom monetizes custom silicon and networking with enviable FCF, and AMD—while catching up fast—must prove that MI350 momentum bridges smoothly to MI450 without a mid-cycle pause as customers await next-gen racks. On most forward frameworks, AMD screens at a premium multiple versus its own history and, depending on the horizon, at or above high-growth peers on sales multiples, with bulls arguing that the systems strategy earns that premium and skeptics focusing on mix and margin.

Context for the broader tape matters, too. This is the second session in a row where investors faded AI strength despite better-than-expected numbers elsewhere, a sign that the market is using earnings as a convenient place to de-risk after an extraordinary run. AMD’s print doesn’t break the bull thesis—far from it—but it does intersect a moment where buyers want more than beats: they want cleaner evidence that today’s AI accelerators are scaling into higher-margin systems revenue, that China risk is compartmentalized, and that 2026 visibility is tightening, not widening.

Net-net: a high-quality quarter, a confident guide, and a credible multiyear path—meeting a market newly allergic to froth. If management continues to land execution milestones into Analyst Day and offers more granularity on Helios, HBM supply, and software traction, today’s air-pocket will look like positioning rather than a thesis break. Until then, the stock may have to work through the hangover that comes from being the market’s favorite AI “next in line.”

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet