Bear of the Day: Vulcan Materials (VMC)

Higher input costs and pricing pressure in construction materials are playing a part in why it may be best to avoid Vulcan MaterialsVMC-- VMC stock at the moment.

Correlating with such, EPS estimates for Vulcan have been trending downward as analysts expect weaker growth than in prior years and compressed margins.

As the largest supplier of construction aggregates in the United States, Vulcan could start to take the brunt of the pain in regard to what has also been slowing demand for aggregate production.

Keeping this in mind, it’s noteworthy that Vulcan’s Zacks Building Products-Concrete and Aggregates Industry is currently in the bottom 1% of over 240 Zacks industries.

Aggregate Production & Demand Issues

Six Straight Quarters of Declining Production

- U.S. Geological Survey (USGS) data shows aggregate production volumes fell for six consecutive quarters up until Q2 of 2025.

- Crushed stone production was down 5.5% at midyear 2025, and shipments were down 4.4% across April-June.

- Material producers cited inclement weather as a major factor reducing output and demand.

Broad Construction Slowdown

- U.S. construction growth dropped sharply from 6.6% in 2024 to just 1.4% in 2025.

- The slowdown spanned all major construction sectors, including residential, commercial, industrial, and infrastructure.

- Weak investor confidence is a key driver of reduced project starts, which directly lowers aggregate consumption. When investors (developers, lenders, private equity, REITs, industrial owners) lose confidence in the economic outlook, they pull back on committing capital to new construction. That hesitation cascades through the entire project pipeline.

Post-Boom Normalization

- After five years of strong growth spurred by post-pandemic demand (over 40% cumulative), construction spending is now rising roughly 2% year over year, which feels like stagnation when adjusted for inflation.

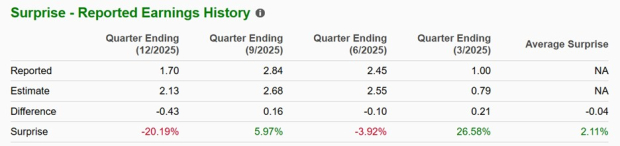

Vulcan’s Q4 Earnings Miss

Causing concern amid slowing demand for construction aggregates is that Vulcan missed Q4 EPS expectations by 20% last month, with quarterly earnings at $1.70 per share compared to estimates of $2.13. This was also a steep drop from EPS of $2.17 in Q4 2024.

Image Source: Zacks Investment Research

Declining EPS Revisions Spark P/E Premium Concerns

Following Vulcan's Q4 earnings miss, EPS estimates for FY26 and FY27 have continued to trend lower and are now down over 10% and 3% in the last 60 days, respectively.

Image Source: Zacks Investment Research

Magnifying the alarming drop in EPS revisions is that Vulcan’s 29X forward earnings multiple is 30% above its Zacks industry peers and reflects an even sharper premium to the benchmark S&P 500's 22X.

Image Source: Zacks Investment Research

Bottom Line

Although Vulcan Materials is still expected to post steady EPS growth, the noticeably weakening earnings outlook is concerning for a stock that investors are paying over $260 a share for. There could be downside risk ahead, as this price point still appears to reflect sentiment for what were much loftier EPS projections.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vulcan Materials Company (VMC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet