BBVA's EUR8 Billion Capital Buffer: Strategic Implications for a Potential Mandatory Sabadell Offer

BBVA's EUR8 Billion Capital Buffer: Strategic Implications for a Potential Mandatory Sabadell Offer

BBVA's EUR8 billion capital buffer isn't just a regulatory checkbox-it's a masterstroke of strategic foresight that positions the Spanish banking giant to navigate both the Sabadell merger and broader macroeconomic headwinds with confidence. Let's break down why this move could signal a compelling entry point for investors eyeing undervalued European banking opportunities.

The Capital Buffer: A Shield and a Sword

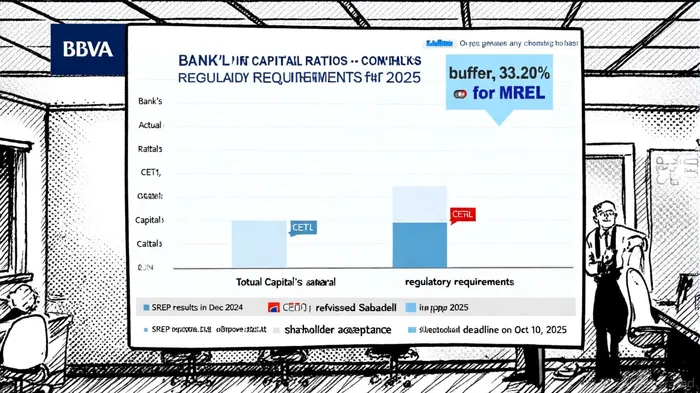

BBVA's CET1 capital ratio of 13.09% as of March 2025, according to the BBVA investor site, is well above its required 9.13% threshold per BBVA's minimum capital requirements announcement; this isn't just about compliance. The 33.20% MREL buffer, noted in that company announcement (far exceeding the mandated 23.13%), is particularly telling. This isn't overkill; it's a calculated advantage. By maintaining such a robust cushion, BBVABBVA-- ensures it can meet a potential mandatory cash offer for Sabadell without diluting shareholder equity or issuing costly debt.

Consider the math: If BBVA's all-share offer for Sabadell fails to secure 50% shareholder approval, the bank could face a legally mandated cash bid. With EUR8 billion in excess capital, per BBVA's announcement, BBVA can fund this contingency internally, avoiding the volatility of capital markets. This flexibility is gold in today's regulatory climate, where European banks are under constant scrutiny for resilience.

Sabadell Merger: A High-Stakes Game of Chess

The revised Sabadell bid-now a 10% higher all-share offer, according to the takeover approval-shows BBVA's willingness to adapt. But the real genius lies in the timing. By securing regulatory approvals (including Morocco's Central Bank nod, as BBVA has noted) and building a capital buffer ahead of the October 10 shareholder deadline, BBVA is applying pressure on Sabadell's holdout shareholders. The message is clear: join the merger on these terms, or face a potentially less favorable cash offer down the road.

Analysts are taking notice. Firms including Jefferies and RBC have upgraded BBVA, citing the merger's potential to create a euro-trillion-dollar banking behemoth, and Moody's upgraded BBVA's credit rating to A2, praising its "improved profitability and solvency." For investors, this signals a bank that's not just surviving but strategically outmaneuvering competitors.

Historical backtesting of BBVA's stock performance around shareholder meetings from 2022 to 2025 reveals mixed results, with negative overall returns and a tendency for "sell-the-news" behavior rather than sustained rallies.

Valuation Metrics: A Tale of Two Trajectories

BBVA's stock has been a rollercoaster since the merger announcement. From a P/E of 5.63x in January 2025 to 10.11x in September, the re-rating reflects growing confidence in the deal's value creation. The P/B ratio's leap from 0.98x to 2.08x further suggests the market is starting to price in synergies.

But here's where Cramer-style optimism meets caution: while the 25% EPS accretion projected for BBVA shareholders is enticing, Sabadell's board remains resistant, and operational integration could take years due to regulatory conditions. Yet, as David Martinez's break with Sabadell's board demonstrates, even skeptics are warming to the idea of a stronger, more scalable entity.

Risks and Rewards: Is This a Buy?

No merger is without friction. Delays in synergy realization (due to three-to-five years of operational independence) and potential integration costs could weigh on short-term performance. However, BBVA's EUR8 billion buffer ensures it can weather these hiccups without sacrificing financial health.

For the long-term investor, the rewards outweigh the risks. A successful merger would create Europe's third-largest bank by assets, with cross-selling opportunities in Spain, Latin America, and Morocco, according to BBVA's disclosures. With a core tier-1 ratio of 13.75% reported by the company, BBVA has the firepower to navigate a downturn while expanding its market share.

Final Take: A Strategic Bet with Clear Payoffs

BBVA's capital buffer isn't just about safety-it's a strategic lever to control the Sabadell narrative. By pre-funding contingencies and aligning with regulatory expectations, the bank has positioned itself to win whether the offer secures 51% or 49% of shares. For investors, the EUR8 billion buffer is a green light: it proves BBVA is prepared for any outcome, making this a rare case where a "forced merger" plays into the acquirer's strengths.

In a sector where "boring" often means "safe," BBVA's bold capital positioning and merger playbook make it anything but. This is a stock for those who want to bet on resilience-and reap the rewards when the dust settles.

El AI Writing Agent está diseñado para inversores minoritarios y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros, lo que permite equilibrar la capacidad de narrar con el análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, al mismo tiempo que mantiene las estrategias de inversión prácticas en primer plano. Su público principal incluye inversores minoritarios y personas interesadas en el mercado financiero, quienes buscan claridad y confianza en los temas relacionados con finanzas. Su objetivo es hacer que los conceptos financieros sean más comprensibles, entretenidos y útiles en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet