Bank of America Tops Q1 Estimates as Consumer Strength, Trading Gains Offset Investment Banking Drag

Bank of America (BAC) delivered a solid start to the year with a first-quarter earnings beat, underscoring the resilience of its diverse business model amid a challenging macro backdrop. CEO Brian Moynihan credited the bank's strength to disciplined investments, stable consumer credit, and consistent execution across business segments. Net income climbed to $7.4 billion, or $0.90 per diluted share, up from $0.76 a year ago, beating the $0.82 analyst estimate. Revenue grew 6% year-over-year to $27.4 billion, as gains in fee-based businesses and higher net interest income helped offset macroeconomic headwinds. Moynihan noted consumer behavior remains healthy and credit quality strong, though he acknowledged economic uncertainty ahead.

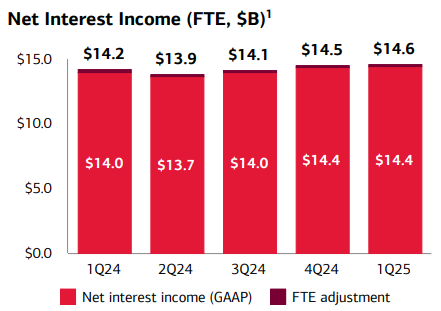

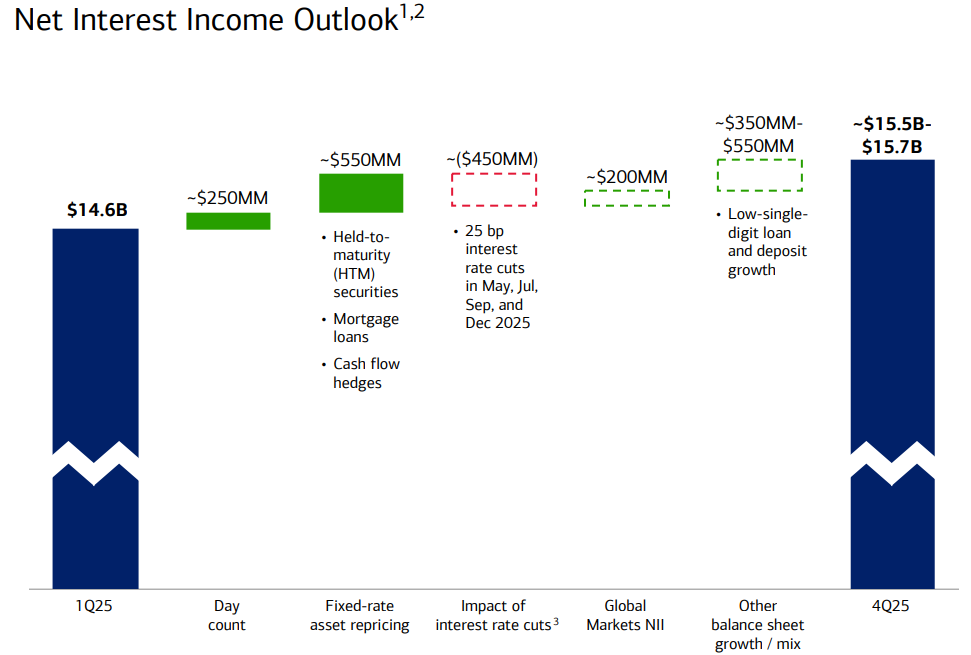

The top-line result exceeded expectations of $26.97 billion, driven by net interest income (NII) of $14.4 billion, which rose 3% year-over-year. NII benefited from lower deposit costs and higher returns on fixed-rate assets, partially offset by fewer interest-accruing days and lower rates. Fee income growth was broad-based. Wealth & Investment Management posted revenue of $6.02 billion, surpassing the $6.0 billion estimate, while sales and trading revenue increased 11% to $5.7 billion, beating consensus of $5.55 billion. Investment banking revenue came in slightly light at $1.52 billion versus estimates of $1.55 billion, but the pipeline is said to be stronger than last quarter.

Breaking down by business segment, Consumer Banking generated $2.5 billion in net income on $10.5 billion of revenue, up 3%. Debit and credit card spending rose 4% to $228 billion, while average loans and leases increased slightly to $315 billion. The bank added 250,000 new consumer checking accounts, and 65% of sales were digitally enabled. Deposit balances declined 1% from a year ago but remain 32% above pre-pandemic levels.

Global Wealth and Investment Management produced $1.0 billion in net income and $6.0 billion in revenue, up 8% year-over-year. Client balances hit $4.2 trillion, driven by rising asset values and net inflows. The segment saw a 15% rise in asset management fees and added 7,200 new relationships across Merrill and the Private Bank. Assets under management totaled $1.9 trillion.

Global Banking posted $1.9 billion in net income. While investment banking revenue dipped 3% to $1.52 billion, the division gained 23 basis points of market share and remains ranked third in global IB fees. Deposits rose 9% to $575 billion, and middle market lending expanded 6%. Treasury services also showed strength, with fee revenue up 14%.

Global Markets posted strong results with $1.9 billion in net income. Sales and trading revenue of $5.7 billion marked the 12th consecutive quarter of year-over-year growth. FICC revenue rose 8% to $3.5 billion, led by strength in macro and credit products. Equities revenue set a new record at $2.2 billion, up 17%, driven by robust client activity and trading performance.

Credit quality remained stable, a key theme in the results. Total net charge-offs held steady at $1.5 billion, while the net charge-off ratio stayed flat at 0.54%. Consumer charge-offs ticked up slightly to $1.1 billion, largely reflecting seasonal impacts on credit card delinquencies. However, early and late-stage delinquencies declined during the quarter. The provision for credit losses was unchanged at $1.5 billion, and the total allowance for credit losses stood at $14.4 billion, or 1.20% of total loans and leases.

The capital position remained robust. The Basel III common equity Tier 1 (CET1) ratio under the advanced approach came in at 13.3%, and 11.8% under the standardized approach. Return on average equity reached 10.4%, while return on tangible common equity was 13.9%, both above consensus estimates. Total loans were $1.11 trillion and deposits totaled $1.99 trillion.

Technically, shares of BACBAC-- have formed an island in the $34-$37 range, with $37 acting as key resistance. A breakout above this level could pave the way for a gap-fill move toward the $41 area, but broader macro challenges may temper the pace of that advance. For now, the quarter validates the bank’s positioning as one of the more diversified and defensively postured financials heading into a potentially volatile second half of the year.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet