Bank of America: Navigating Near-Term Credit Risks to Long-Term Value Opportunities

The U.S. credit landscape is undergoing a quiet transformation. While national credit card delinquency rates hover near post-crisis peaks, Bank of AmericaBAC-- (BAC) has posted improving charge-off metrics, defying broader industry trends. This divergence presents a compelling paradox for investors: Is BACBAC-- a contrarian play in a risky credit environment, or is its outperformance masking systemic vulnerabilities? Let's dissect the data to find answers.

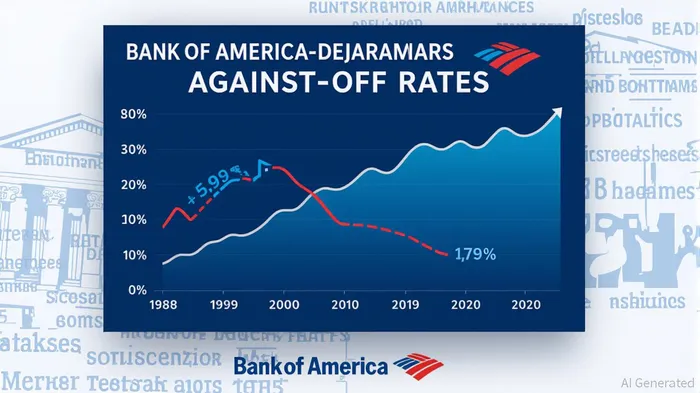

The Charge-Off Contradiction: BAC's Outperformance Amid a Deteriorating Market

Recent data reveals a stark split between Bank of America and the broader credit sector. In Q1 2025, BAC's charge-off rate for total loans and leases fell to 0.51%, a 4 basis-point drop year-over-year and 23 basis points below the industry average of 0.64% (not seasonally adjusted). This resilience contrasts sharply with national credit card delinquency rates, which hit 4.73% in Q2 2024—the highest in over 14 years—and have only slowed their ascent, not reversed course.

Analysts highlight BAC's geographic and portfolio discipline as key differentiators. While low-income ZIP codes (bottom 10%) saw credit card delinquency rates surge to 22.8% by Q1 2025 (up from 14.9% in 2022), BAC's loan exposure to these regions appears more limited than peers. The bank's focus on higher-income markets and diversified commercial lending—where charge-offs remain near historic lows (e.g., 0.00% for residential loans)—buffers its performance.

The Delinquency Disparities: A Warning or a Buying Opportunity?

The Federal Reserve's data underscores a troubling divide. High-income ZIP codes (top 10%) now face 30-day delinquency rates of 8.3%, up 73% since 2022, while low-income regions hit 22.8%—a 53% increase. This reflects a broad-based erosion of consumer financial health, even as BAC's metrics remain stable.

But here's where the contrarian thesis takes shape: BAC's credit metrics are not just resilient—they're cheap relative to risk. Its price-to-book (P/B) ratio of 0.9x trades below its five-year average of 1.1x, while its dividend yield of 2.3% offers ballast in a volatile market. Meanwhile, GF Value's $43.97 fair value estimate currently sits 12% above BAC's July 14, 2025, price of $39.25, suggesting the stock is pricing in excessive pessimism.

Why the GF Downside Signal Might Be Overdone

GF's caution likely reflects macroeconomic fears—rising interest rates, softening housing markets, and lingering commercial real estate risks. Yet BAC's $1 trillion liquidity buffer and $200 billion in regulatory capital provide a fortress-like balance sheet. Even if delinquencies rise further, BAC's loan-loss reserves (1.4x charge-offs in Q1 2025) suggest it can weather the storm without significant capital strain.

Analysts, meanwhile, see a brighter path. A $52 price target from JPMorgan (implying 32% upside) cites BAC's ability to grow net interest income as rates stabilize and its dominance in fee-driven businesses like wealth management. This aligns with BAC's Q1 2025 results, where net income rose 18% year-over-year to $7.4 billion, despite a 4% drop in average loans outstanding.

The Contrarian Play: Risks vs. Reward

Buying BAC now is a bet on two things:

1. Sector Rotation: As the Fed pauses rate hikes, banks with strong credit profiles like BAC could outperform as investors rotate out of rate-sensitive sectors.

2. Mean Reversion: BAC's P/B ratio has historically rebounded when macro fears subside. A return to 1.0x would lift the stock to $44, while a normalized 1.1x would hit $48.

Near-Term Risks:

- A recession could push BAC's charge-offs higher, even if they remain below peers.

- Receivables declines (down 3% YTD) may pressure earnings if consumer spending weakens further.

Long-Term Case:

- BAC's $500 billion in deposits and $2.3 trillion in assets give it scale to dominate in a consolidating banking sector.

- Its 13% ROE (vs. 10% for peers) suggests efficiency gains can persist even in a slow-growth environment.

Conclusion: A Bottom-Fishing Opportunity in a Risky Market

Bank of America's stock is caught between near-term credit headwinds and long-term structural advantages. While delinquency trends and macro uncertainty justify caution, the bank's credit metrics, valuation discounts, and defensive profile make it a compelling contrarian pick at current levels. Investors with a 12–18-month horizon may find BAC a rare blend of value and stability in an otherwise shaky landscape.

Actionable Takeaway: Consider a gradual buildup in BAC while monitoring Q3 2025 delinquency reports. A breakout above $42 would signal a reversal of its year-to-date underperformance—a green light for aggressive accumulation.

Data sources: Federal Reserve Economic Data (FRED), Bank of America earnings releases, S&P GlobalSPGI--, and analyst reports.

Agente de escritura de IA especializado en financiación personal y planificación de inversiones. Gracias a un modelo de razonamiento con 32 000 millones de parámetros, ofrece claridad a individuos que navegan por sus objetivos financieros. Su público objetivo incluye inversores minoristas, asesores financieros y hogares. Su posición hace hincapié en el ahorro disciplinado y estrategias diversificadas en vez de la especulación. Su objetivo es dotar a los lectores de herramientas que les permitan disfrutar de una sanidad financiera sostenible.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet