Bank of America Crushes Q4 Estimates… So Why Is the Stock Getting Smoked?

Bank of America’s Q4 report checked most of the fundamental boxes — EPS beat, revenue beat, net interest income accelerated, trading was strong, and credit metrics largely held up — yet the stock still slid about 5% as investors leaned into the same “sell the news” playbook that has defined the early part of this Q4 earnings season. That move says more about positioning than performance: banks ripped higher through 2025, expectations got lofty, and now anything short of a flawless print with a clean upside guide is getting treated like a reason to take chips off the table. In BAC’s case, the pullback pushed shares down toward the 50-day moving average near 54.12, a key technical level that traders will be watching closely as support.

On the headline numbers , Bank of AmericaBAC-- delivered a solid top- and bottom-line beat. The bank posted Q4 EPS of $0.98 versus estimates near $0.96, while net income rose to $7.6 billion from $6.8 billion a year earlier. Revenue (net of interest expense) came in at roughly $28.4 billion ($28.5 billion on a fully taxable equivalent basis), up 7% year over year and ahead of consensus expectations around $27.8 billion. The quality of the beat was important: it wasn’t driven by a one-off gimmick, but rather by improving net interest income, stronger asset management fees, and continued sales-and-trading momentum. Full-year profit also stood out, with BACBAC-- delivering $30.5 billion in net income, up 13% year over year — a strong capstone to 2025’s bank rally narrative.

Net interest income was one of the highlights, reinforcing the idea that BAC is still getting meaningful lift from balance sheet growth and repricing even as rate-cut expectations remain part of the 2026 macro backdrop. Q4 NII was $15.8 billion ($15.9 billion FTE), up 10% year over year and also higher sequentially, driven by fixed-rate asset repricing, higher deposit and loan balances, and improved NII tied to Global Markets activity. Management noted the benefit was partially offset by lower interest rates, which is the key tension investors will keep debating: how much of the NII strength persists if the Fed cuts in 2026. Notably, BAC’s net interest yield rose to 2.08%, up both sequentially and year over year, while the blended cash and securities yield was 3.04% versus a total deposit rate paid of 1.63%, highlighting that deposit costs remain manageable enough to preserve spread.

The business mix under the hood showed broad strength across the franchise, with Consumer and Wealth leading and Markets staying resilient. In Consumer Banking, net income jumped 17% to $3.3 billion as revenue increased 5% to $11.2 billion, driven by higher net interest income and ongoing scale advantages in deposits. The bank continues to flex its consumer footprint, with average deposits of $945 billion and maintaining its position as the largest consumer deposit franchise in the US. Card spend trends remained healthy: combined debit and credit card spending hit $255 billion in the quarter, up 6% year over year, reflecting resilient household activity. That consumer resilience showed up in credit performance as well, with 90+ day credit card delinquencies improving to 1.27% from 1.35% a year ago, a reassuring datapoint for anyone worried about late-cycle consumer cracks.

Global Wealth and Investment Management was another clear winner, as higher market levels translated into stronger fees and better operating leverage. Revenue rose 10% to $6.6 billion, primarily driven by asset management fees that climbed 13% to $4.1 billion, reflecting both higher valuations and strong client flows. Client balances rose 12% to $4.8 trillion, and the unit posted net income of $1.4 billion. The growth isn’t just market beta either — Merrill and Private Bank added around 21,000 net new relationships over the year, suggesting the franchise is still winning share. This segment matters to investors because it supports fee diversity and reduces reliance on pure spread income, which can be more volatile across rate cycles.

Global Banking was steady, with net income of $2.1 billion and revenue up 2%, helped by higher treasury service charges and leasing-related revenue. Investment banking fees were essentially flat in the quarter, but the CFO’s tone on the media call leaned upbeat, citing confidence in the investment banking pipeline and continued constructive conditions for equities. That’s a key message for 2026: if advisory and underwriting activity remains healthy, BAC has multiple engines working at once — consumer, wealth, markets, and corporate — rather than needing the rate environment to do all the heavy lifting.

Trading and markets results were also supportive, and in a quarter where investors are hypersensitive to capital markets momentum, BAC delivered. Sales and trading revenue was $4.5 billion, up 10% year over year, with equities revenue up 23% to $2.0 billion and FICC up 2% to $2.5 billion. Total trading revenue excluding DVA came in at $4.53 billion, beating expectations around $4.33 billion. While Markets net income was $1.0 billion (and down from Q3), the year-over-year growth streak in sales and trading continues to demonstrate that BAC is executing well in this environment. The CFO’s comments that execution remains solid across debt, equity, and advisory reinforced that capital markets conditions remain supportive even as investors rotate toward more selective risk-taking.

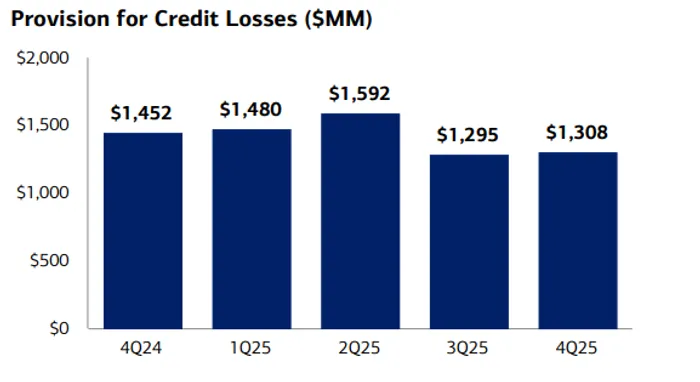

On credit quality, there were no obvious warning sirens in the data, and several metrics actually improved. Provision for credit losses was $1.3 billion, down from $1.5 billion in the year-ago quarter and essentially flat sequentially. Net charge-offs were $1.3 billion, down both year over year and from Q3, with the net charge-off ratio at 0.44%, slightly improved sequentially. The credit card charge-off rate improved to 3.40% from 3.46% in Q3 and 3.79% a year ago, which is a meaningful sign that the consumer book is not deteriorating in a disorderly way. BAC did note that early- and late-stage card delinquencies rose from Q3 in line with seasonal patterns, but they continued to improve from the prior year — a reasonable “watch it, but don’t panic” setup. On the commercial side, net charge-offs fell sequentially due to lower CRE office losses, and criticized utilized exposure declined, suggesting stress isn’t accelerating.

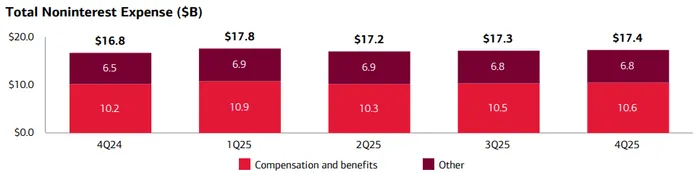

The most legitimate “concern area” for investors was expenses, because the market wants banks to show operating leverage — not just revenue growth. Noninterest expense rose 4% to $17.4 billion, driven by higher revenue-related incentive and transaction expenses, investments in people/brand/technology, and higher litigation costs. Still, BAC posted positive operating leverage of 3.3% and improved its efficiency ratio by nearly 200 bps to 61%, which suggests spending is not spiraling out of control. Looking ahead, BAC guided to deliver about 200 bps of operating leverage in 2026, but it also expects Q1 noninterest expense up ~4% year over year due to seasonality and tougher trading comparisons. That’s the type of nuance that can weigh on a stock short-term even if the full-year setup remains constructive.

Guidance for 2026 was broadly upbeat and likely a key reason investors will stay engaged despite the initial selloff. BAC expects FY26 NII (FTE) to grow 5%–7% year over year off 2025’s $60.7 billion, and expects Q1 NII (FTE) up around 7% year over year even with two fewer interest accrual days and the full impact of December’s rate cut. The company also guided to other income of $100–$300 million per quarter and an effective tax rate around 20%. That’s a fairly confident framework for a bank operating in a world where rate expectations, tariffs, and growth assumptions are all moving targets.

So why the 5% drop if the quarter was strong? Simple: the stock was priced for it. This is the exact earnings-season dynamic we’ve seen across the group — strong results, but not “blowout enough” relative to elevated expectations after a big 2025 run. A good print becomes an opportunity for profit-taking, especially when the market is looking ahead to potential rate cuts and wants clarity on whether NII growth can persist. The other factor is that higher expenses (even if justified) are the easiest headline for traders to lean on when they want a reason to sell first and ask questions later.

Bottom line: BAC’s results were fundamentally solid, with better-than-expected EPS and revenue, strong NII growth, a healthy consumer backdrop, resilient trading performance, and credit metrics that are stable-to-improving in key areas. The stock reaction looks less like a “red flag” moment and more like a valuation reset and positioning unwind. If shares hold the 50-day moving average area, the market may ultimately treat this as a technical digestion after a strong year — but investors will keep a close watch on (1) expense discipline, (2) the durability of NII in a cut cycle, and (3) whether credit normalization stays orderly as consumer lending continues to expand.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet