AVO Falls Nearly 12% in a Month: Time to Buy or Stay on the Sidelines?

Mission Produce, Inc. AVO has come under notable pressure in the past month, with its shares dropping as much as 11.9%. Despite delivering solid operational execution in the first quarter of fiscal 2026, including volume growth and margin expansion, investor sentiment has remained cautious amid ongoing pricing pressures in the avocado market.

The normalization of pricing, following a period of elevated levels, has weighed on the company’s top-line performance in the first quarter of fiscal 2026, creating a disconnect between revenue trends and underlying fundamentals. In addition, concerns around near-term margin compression, lower asset utilization and uncertainty tied to its pending acquisition continue to act as overhangs, limiting near-term upside for the stock.

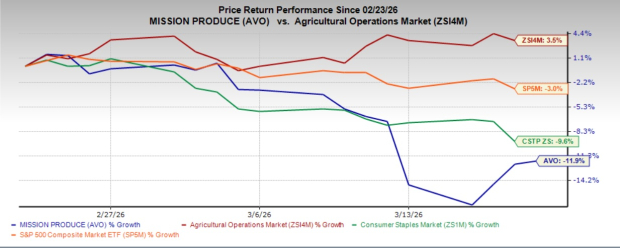

AVO’s sharp share decline has resulted in underperformance as the Zacks Agriculture – Operations industry advanced 3.5% in the same period. Meanwhile, the Consumer Staples sector and the S&P 500 index slipped 9.6% and 3%, respectively, highlighting Mission Produce’s relatively weaker performance.

Mission Produce’s One-Month Price Performance

Image Source: Zacks Investment Research

AVO’s performance has also lagged its key peers, such as Adecoagro AGRO, Archer Daniels Midland Company ADM and Dole Plc DOLE. The stock has notably trailed AdecoagroAGRO-- and Archer DanielsADM--, which delivered gains of 63.8% and 1.4%, respectively, in the past month. Meanwhile, AVOAVO-- has slightly underperformed DoleDOLE--, whose shares declined 9.9% during the same period.

Currently at $12.54, AVO’s stock price reflects a 30.6% premium to the company’s 52-week low of $9.60. The stock is trading at a 16.5% discount from its 52-week high of $15.02, reflecting upside potential.

Let’s take a closer look at the factors driving the stock’s recent weakness and evaluate whether it still offers meaningful upside potential.

Factors Hindering AVO’s Performance

Mission Produce’s recent stock momentum is largely tied to its heavy exposure to volatile avocado pricing, which continues to distort top-line performance. Despite strong volume growth of 14% in first-quarter fiscal 2026, revenues declined 16.6% due to a sharp 30% drop in pricing. This highlights a structural challenge in the business model, where external supply conditions — particularly from Mexico — can significantly impact realized prices. As pricing normalizes from elevated levels, investors worry that revenue growth may remain inconsistent, even if underlying demand trends stay healthy.

Another fundamental concern lies in margin sustainability and near-term earnings visibility. While the company managed to expand gross margins and grow adjusted EBITDA modestly, management has guided a margin compression in the fiscal second quarter due to continued pricing pressure and lower asset utilization. A delayed California harvest and reliance on a single sourcing region are expected to further weigh on profitability. Additionally, the Blueberries segment is facing yield-related inefficiencies, leading to higher production costs and weaker segment EBITDA, raising questions about execution consistency across newer growth areas.

Lastly, the pending Calavo acquisition introduces both opportunity and risk, shaping investor sentiment. While the deal is expected to generate at least $25 million in cost synergies and expand capabilities into prepared foods, it also brings integration challenges and near-term leverage concerns. Investors are cautious about execution risks, the timeline of synergy realization and the impact on the balance sheet before deleveraging is achieved. Until clearer visibility emerges on post-acquisition performance and capital allocation priorities, these uncertainties are likely to remain a key overhang on the stock.

Mission Produce’s Estimate Revision Trend

The Zacks Consensus Estimate for AVO’s fiscal 2026 and 2027 earnings remained unchanged in the last 30 days. For fiscal 2026, the Zacks Consensus Estimate for AVO’s sales and EPS implies year-over-year declines of 10.2% and 10.1%, respectively. For fiscal 2027, the Zacks Consensus Estimate for AVO’s sales and EPS implies year-over-year growth of 1.7% and 4.2%, respectively.

Image Source: Zacks Investment Research

Are AVO’s Long-Term Fundamentals Intact?

Mission Produce benefits from its vertically integrated business model, which remains a key competitive advantage in a highly fragmented produce industry. The company’s control across sourcing, farming, packing, distribution and marketing enables better supply chain coordination, improved cost efficiencies and more consistent product quality. This integrated structure allows Mission ProduceAVO-- to respond quickly to changing market conditions, optimize per-unit margins and maintain strong customer relationships, even in volatile pricing environments.

A key area of strength is the Marketing and Distribution segment, which continues to deliver robust growth and profitability. Despite lower pricing, the segment posted strong volume gains and a notable increase in adjusted EBITDA, driven by improved per-unit margins and effective execution. This performance highlights the company’s ability to leverage its scale, logistics network and category management expertise to drive earnings growth, reinforcing confidence in its core operating engine.

The company’s International Farming segment is showing encouraging momentum, supported by improved asset utilization and efforts to maximize returns from its global footprint. Initiatives such as increasing packhouse utilization and diversifying crop handling are helping smooth seasonality and enhance operating leverage. These improvements indicate better efficiency and stronger contribution from owned assets, which is a positive fundamental driver over the long term.

Overall, Mission Produce’s integrated platform, coupled with strong performance in its key segments, positions it well to capitalize on favorable industry trends. The combination of volume-led growth, improving operational efficiencies and expanding global capabilities continues to support its long-term earnings potential, providing a solid foundation for sustained value creation.

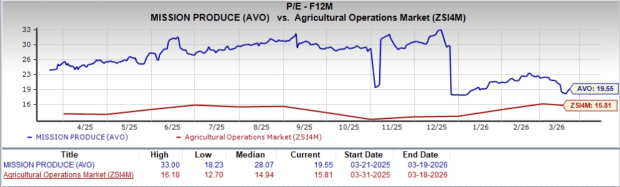

Is AVO’s Premium Valuation Justified?

Mission Produce is currently trading at a forward 12-month P/E multiple of 19.55X, exceeding the industry average of 15.81X and the S&P 500’s average of 16.57X.

While this valuation may appear stretched at first glance, it remains well below the company’s five-year peak multiple of 58.58X, suggesting room for potential upside. Despite the recent pullback in the stock, the premium valuation signals that investors continue to factor in solid growth prospects and expect strong future performance from AVO.

At its current valuation, Mission Produce trades at a notable premium to several close competitors, including Dole, Adecoagro and Archer Daniels, all of which are delivering lower earnings multiples. Dole, Adecoagro and Archer Daniels have forward 12-month P/E ratios of 9.82X, 12.07X and 16.86X — all significantly lower than that of AVO.

Image Source: Zacks Investment Research

Mission Produce Faces Pressure: Should Investors Hold?

Mission Produce has seen recent weakness in its stock, largely due to near-term pricing pressures and market volatility. While these factors have weighed on sentiment, the company’s vertically integrated business model and global sourcing network provide a strong competitive advantage, enabling efficient operations and consistent product quality. Its core segments continue to perform well, demonstrating resilience even in a challenging market environment.

With a premium valuation relative to peers, near-term stock performance may continue to be uneven. For existing investors, holding the position appears prudent, given the company’s solid fundamentals and long-term growth potential.

Mission Produce currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Archer Daniels Midland Company (ADM): Free Stock Analysis Report

Dole PLC (DOLE): Free Stock Analysis Report

Adecoagro S.A. (AGRO): Free Stock Analysis Report

Mission Produce, Inc. (AVO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet