Average Weekly Hours Dip Signals Shift in Economic Tides: Navigating Sector Rotations

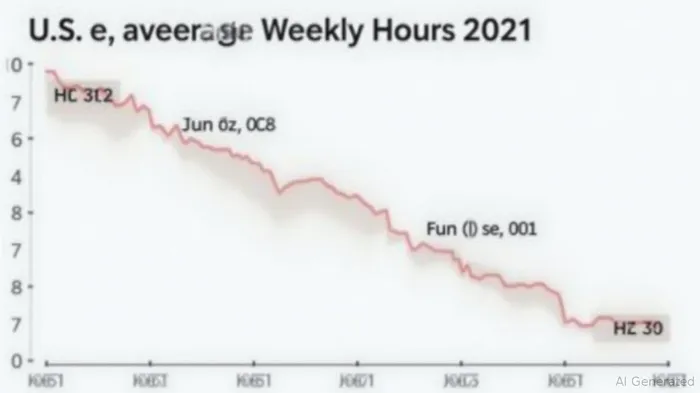

The June U.S. Average Weekly Hours report, a critical labor market indicator, edged lower to 34.2 hours, missing consensus expectations of 34.3. This subtle decline—marking the third consecutive monthly drop from 2023's peak—underscores a softening labor market, with implications for Federal Reserve policy and sector rotations. For investors, the data highlights a critical crossroads: cyclical sectors like automobiles face headwinds, while technology-driven industries like semiconductors may gain traction as businesses prioritize efficiency over expansion.

A Slowing Labor Market: Causes and Consequences

The dip in average weekly hours reflects cautious corporate behavior amid elevated borrowing costs and weakening demand for discretionary goods. Key drivers include:

- Elevated interest rates: The Fed's aggressive rate hikes have constrained consumer spending and corporate investment.

- Structural shifts: Retail and leisure/hospitality sectors—where hours fell 2.5% and 2.1% since 2022, respectively—continue to grapple with post-pandemic demand shifts toward online shopping and part-time work.

- Corporate prudence: Firms are scaling back hours to manage costs in an environment of uncertain growth.

The automotive sector is particularly vulnerable. Companies like General Motors (GM) and Ford (F) rely on consumer confidence and spending power, both of which are waning as households face higher borrowing costs and stagnant wage growth. Meanwhile, the semiconductor industry—driven by demand for AI chips, advanced manufacturing, and efficiency upgrades—is positioned to benefit.

Fed Policy: Dovish Shifts and Rate Cut Hesitation

The Federal Reserve will parse this data closely. While the miss supports a narrative of cooling labor market tightness—a key driver of inflation—it does not yet confirm a sustained slowdown. Fed officials remain wary of wage growth, which remains elevated relative to inflation targets.

A pause in rate hikes at the July meeting appears likely, but cuts will depend on further easing in wage pressures. Investors should monitor the July nonfarm payrolls and July PCE inflation reports for clarity.

Sector Implications: Automotives Under Pressure, Semiconductors in the Spotlight

The backtest data reveals a clear pattern: when average weekly hours miss forecasts, automobiles underperform for 21 days, while semiconductors outperform over 55 days. This divergence stems from the sectoral dynamics at play:

- Automobiles: Weaker consumer demand for discretionary purchases (e.g., new cars) and lingering inventory gluts (noted in recent earnings reports from NXP SemiconductorsNXPI-- and STMicroelectronics) weigh on valuations.

- Semiconductors: Businesses pivot to technology-driven efficiency gains, boosting demand for AI chips, data center infrastructure, and advanced manufacturing tools.

Investment Strategy: Position for Defensive Tech and Avoid Cyclical Goods

- Underweight automobiles: Reduce exposure to automakers like GMGM-- and Ford, which face both demand headwinds and supply chain complexities (e.g., lingering semiconductor inventory mismatches).

- Overweight semiconductors: Favor companies at the forefront of AI and advanced packaging, such as NVIDIANVDA--, AMDAMD--, and ASML HoldingASML-- (ASML), which benefit from secular demand and geopolitical-driven supply chain resilience.

- Monitor macro catalysts: Keep an eye on the July Fed meeting and inflation reports. A dovish pivot could boost tech stocks further, while a surprise hawkish stance might prolong cyclical sector pain.

Conclusion: Riding the Shift to Efficiency-Driven Growth

The Average Weekly Hours miss is a symptom of a broader economic recalibration: businesses and households are prioritizing efficiency over expansion. For investors, this means favoring sectors that thrive in such environments—semiconductors, AI infrastructure, and productivity tools—while avoiding those tied to discretionary spending.

The data underscores a simple truth: in a slowing labor market, the winners are those who help companies and consumers do more with less.

Investors should use this dynamic to navigate the crosscurrents of a slowing labor market and a tech-driven future.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet