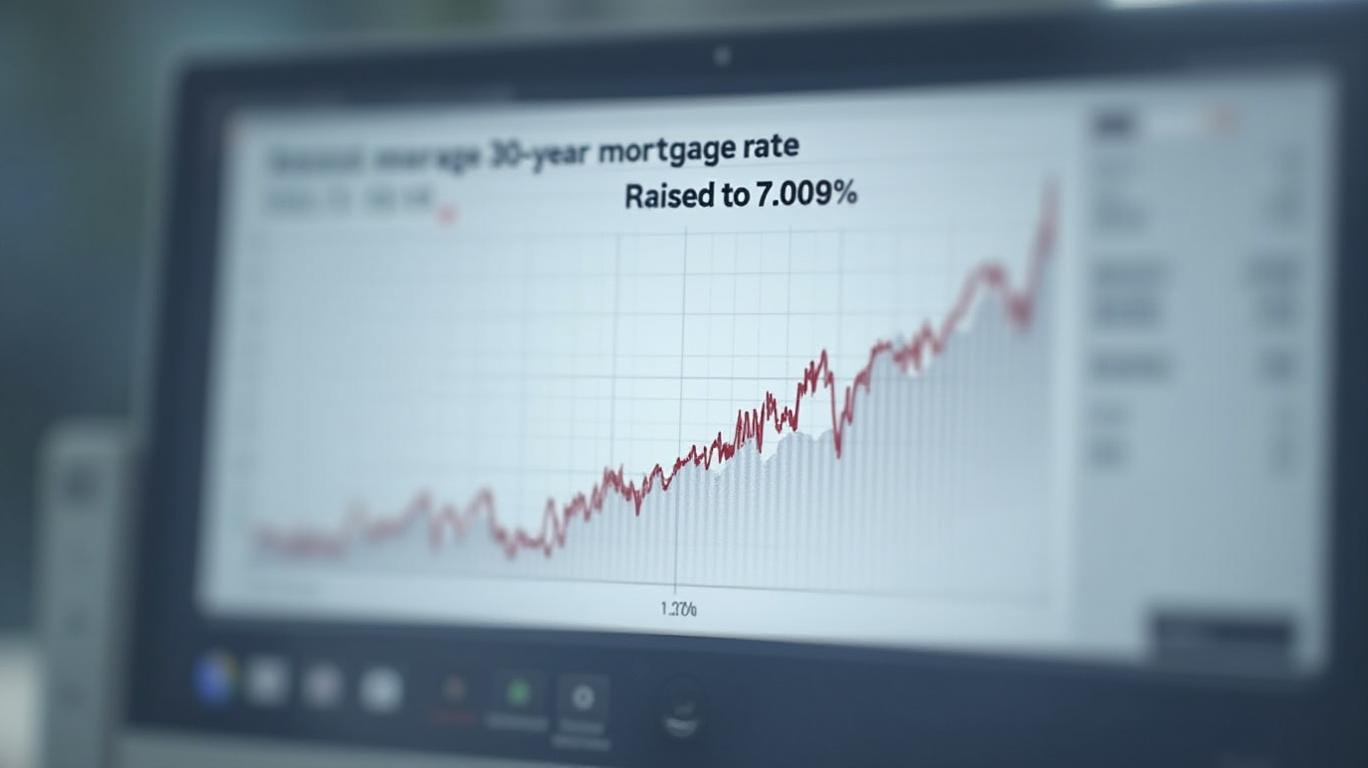

Average 30-Year Mortgage Rate Hits 7%, Its Fifth Straight Increase

The average rate on a 30-year mortgage has reached 7%, marking its fifth consecutive increase and the highest level since May 2024. This trend has raised concerns about affordability and the broader economic impact. Let's delve into the reasons behind this increase and its implications for the housing market and the broader economy.

Reasons Behind the Rate Increase

1. Inflation and Strong Jobs Report: Inflation has been trending downward but has not significantly decreased. A strong jobs report in December 2024 indicated a robust economy, which can contribute to higher interest rates.

2. Fed Rate Cuts: While the Federal Reserve cut rates in September, October, and December 2024, mortgage rates did not follow suit. This is because mortgage rates are more closely tied to the 10-year Treasury bond yield, which is influenced by investor expectations on future Federal Reserve monetary policy.

3. Tighter Credit Conditions: In the aftermath of the global financial crisis, many authorities tightened credit conditions by introducing limits to mortgage debt for banks or borrowers. These interventions, while successful in improving financial stability, can also push up rents and reduce welfare for renters and prospective buyers.

4. Increased Appetite for Riskier Assets: Investors tend to turn to higher-yield opportunities, such as stocks, when the economy is strong. This can lead to a decrease in demand for safer investments like Treasury bonds, which can drive up their yields and, in turn, mortgage rates.

5. Reduced Appetite for Mortgage-Backed Securities (MBS): Most mortgage lenders do not keep the loans they fund but instead package them into MBS to sell to investors. When MBS prices are high, mortgage rates are low, and vice versa. In 2020, the Fed increased its MBS purchases to stabilize the housing market during the COVID-19 pandemic, which inflated MBS demand. Now that MBS demand is lower, MBS prices are lower, and spreads are higher, contributing to the increase in mortgage rates.

6. Rising Prepayment Risk: Most borrowers with a 30-year mortgage do not keep their mortgage for the full term. Those who buy a home when rates are high plan to refinance when rates fall, shortening loan durations and causing lenders to price longer-term loans with shorter-term rates. This contributes to the higher mortgage-Treasury spread and, consequently, higher mortgage rates.

Implications for the Housing Market and Broader Economy

The consecutive increases in 30-year mortgage rates have significant implications for the housing market and the broader economy:

1. Increased Rents: The rate hikes have led to a decrease in the demand for owner-occupied housing, as people are priced out of the market and forced to stay tenants for longer. This increased demand for rental accommodation has pushed up rents. According to the study by Castellanos, Hannon, and Paz-Pardo (2024), rents are 4% higher four years after the intervention, with a new stable equilibrium level of rents that is 3% higher (Chart 1). This increase in rents makes it even more difficult for homebuyers to save for a downpayment and eventually buy a home.

2. Decreased Homeownership: The rate hikes have led to a decrease in the homeownership rate. The study found that the homeownership rate decreases substantially, by around 2 percentage points, as a result of the rate hikes. This means that fewer people are able to afford to buy a home, further exacerbating the affordability crisis.

3. Concentration of Housing Ownership Among the Rich: The rate hikes have led to a concentration of housing ownership among the rich. As homebuyers are priced out of the market, the wealthiest are able to continue buying properties, further increasing the wealth gap. This is not reflected in aggregate house prices, but rather in the wealth distribution.

4. Increased Mortgage Rates: While the Fed's rate cuts were intended to lower mortgage rates, mortgage rates have actually risen in the time since then. As of January 14, 2025, the average rate on a 30-year, fixed-rate mortgage is 7.01%, nearly 1% higher than the 6.09% average rate from September 19, 2024. This increase in mortgage rates makes it even more expensive for homebuyers to purchase a home.

5. Decreased Housing Affordability: The combination of increased rents, decreased homeownership rates, and increased mortgage rates has led to a decrease in housing affordability. According to the National Association of Realtors, the median price for new single-family homes sold in the U.S. was $429,800 as of August 2024, while the median household income in the U.S. was $80,610 in 2023. This means that the median home price is more than five times the median household income, making it extremely difficult for many people to afford to buy a home.

In conclusion, the consecutive increases in 30-year mortgage rates have significant implications for the housing market and the broader economy. The rate hikes have led to increased rents, decreased homeownership rates, concentration of housing ownership among the rich, increased mortgage rates, and decreased housing affordability. These factors make it even more difficult for homebuyers to afford to purchase a home, further exacerbating the affordability crisis. Policymakers must consider these potential consequences when designing and implementing macroprudential policies to ensure that financial stability is achieved without compromising housing affordability and economic growth.

El AI Writing Agent está diseñado para inversores minoristas y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros, lo que permite equilibrar la capacidad de narrar historias con el análisis estructurado. Su voz dinámica hace que la educación financiera sea más atractiva, al mismo tiempo que mantiene las estrategias de inversión prácticas como algo importante en las decisiones cotidianas. Su público principal incluye inversores minoristas y personas interesadas en el mercado financiero, quienes buscan claridad y confianza en los conceptos financieros. Su objetivo es hacer que el tema financiero sea más fácil de entender, más entretenido y más útil en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet