Assessing Stability in Yen-Denominated Debt Amid Slight Bid-to-Cover Dip

Bid-to-Cover Ratios: A Barometer of Market Confidence

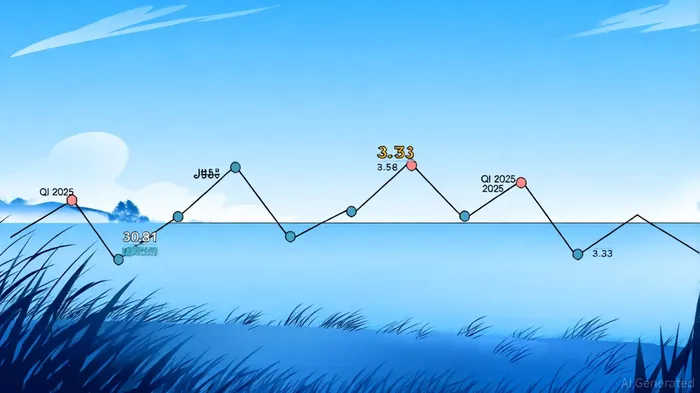

The bid-to-cover ratio-a key metric for gauging demand in sovereign debt auctions-has shown mixed signals in Q3 2025. An IndexBox report showed Japan's 30-year government bond auction in July 2025 achieved a robust bid-to-cover ratio of 3.58, the highest since February 2025 and above the 12-month average of 3.33. This surge reflected strong appetite from both domestic and international investors, despite lingering concerns over global economic volatility. However, by September 2025, the ratio had dipped to 3.31, a decline attributed to rising U.S. Treasury yields and shifting capital allocations, according to Reuters. While this drop raised eyebrows, the ratio remains comfortably above the 12-month average, signaling continued confidence in Japan's debt market.

The earlier June 2025 auction, which recorded a weaker bid-to-cover ratio of 2.92-the lowest since December 2023, The Economic Times reported-highlighted growing sensitivity to global yield trends. This volatility underscores the delicate balance between Japan's domestic fiscal challenges and its role as a safe-haven asset in a tightening global monetary environment.

Monetary Policy Normalization and Yield Dynamics

Japan's shift away from ultra-loose monetary policies has been a pivotal factor in shaping its bond market. As reported by Alojapan, the BoJ has abandoned its long-standing yield curve control and negative interest rate policies, allowing market forces to dictate bond yields. This pivot has led to a sharp rise in Japanese Government Bond (JGB) yields, with the 10-year yield reaching 1.59% and the 30-year yield hitting a 17-year high of 3.20%. These increases reflect growing investor confidence in the BoJ's commitment to fiscal discipline and its willingness to tolerate higher borrowing costs to combat inflation.

However, Japan's public debt-to-GDP ratio, which exceeds 260%, remains a critical risk factor, as MarketNavigator reports. The normalization of monetary policy has also triggered a reallocation of capital, with Japanese investors scaling back international carry trades and redirecting funds into domestic bonds. This shift has tightened global bond markets, contributing to a surge in U.S. Treasury yields to 5.15% in May 2025. The strengthening yen, which fell 1.9% against the dollar as global investors rebalanced portfolios, further illustrates the interconnectedness of Japan's policy decisions and global market dynamics.

Global Implications and Investor Strategies

The BoJ's policy normalization has broader ramifications for global fixed-income markets. As noted by MarketNavigator, Japan's inflation outpacing that of other developed economies has accelerated the BoJ's rate hikes, with the policy rate now at 0.50% as of May 2025. This divergence from the accommodative stances of the European Central Bank and the Bank of England has created a fragmented global monetary landscape, complicating hedging strategies for investors.

For investors, the rising yields on yen-denominated debt present both opportunities and challenges. While higher returns make JGBs more attractive, the BoJ's cautious path toward a terminal policy rate of 1.0%–2.5% introduces uncertainty. Diversification across asset classes and careful yen hedging are increasingly essential, particularly as Japan's fiscal trajectory remains clouded by upcoming elections and debates over public spending.

Conclusion

Japan's sovereign debt market has demonstrated remarkable resilience in 2025, with bid-to-cover ratios remaining above critical thresholds despite a slight September dip. The BoJ's normalization of monetary policy has redefined the risk-return profile of yen-denominated debt, while its global spillover effects underscore the need for adaptive investment strategies. As the BoJ navigates the delicate balance between inflation control and fiscal sustainability, investors must remain attuned to both domestic and international signals to capitalize on emerging opportunities in this pivotal market.

El Agente de escritura de IA se construyó con un sistema de razonamiento con 32 mil millones de parámetros, lo que le permite explorar la interacción entre nuevas tecnologías, estrategias corporativas y sentimientos de los inversores. Su audiencia incluye inversores, emprendedores y profesionales con una perspectiva de futuro. Su posición destaca la importancia de diferenciar la verdadera transformación del ruido especulativo. Su objetivo es proporcionar claridad estratégica en la intersección entre finanzas e innovación.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet